[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”]

[breadcrumb]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.106″ title=”Index” open=”off”]

Contents

29.2 Recognition and measurement of current tax.

29.2.1 Extract from FRS102: Section 29.3 – 29.5.

29.2.2.1 What tax rate to use.

29.2.2.1.1 Ireland and UK rules.

29.2.2.1.2 Impact of change in tax rate – substantively enacted just after year end.

29.2.2.1.3 Change in rate during the year.

29.2.2.2 Uncertain tax positions.

29.2.2.2.2 Assessing whether a provision is required.

29.2.2.3 Interest charged on late payment of taxes.

29.2.2.5 Adjustments in respect of prior years.

26.2.2.6 Recognition of current tax asset.

29.2.2.6.1 Tax paid in excess of tax charge for current and previous periods.

29.2.2.6.2 Tax losses set back to prior periods.

29.2.2.7 Allocation of the tax expense.

29.3 Provision for close company surcharge.

29.3.1 Extract from FRS 102 Section 29.14.

29.4 Recognition of deferred tax.

29.4.1 Extract from FRS102: Section 29.6–29.17.

29.4.2.1 Deferred tax defined and the purpose of deferred tax.

29.4.2.2 Permanent differences.

29.4.2.2.1.1 The one exception for recognising a permanent difference for deferred tax.

29.4.2.3 Temporary differences.

29.4.2.3.1 Temporary differences defined.

29.4.2.3.2 Definition of deferred tax assets and instances where they arise.

29.4.2.3.2.1 When does a deferred tax asset exist including examples.

29.4.2.3.3 Definition of deferred tax liabilities and instances where they arise.

29.4.2.3.3.1 When does a deferred tax liability exist including examples.

29.4.2.3.4 Recognition of timing differences – the rules.

29.4.2.3.4.1 Unrelieved tax losses – The rule recognition or not.

29.4.2.3.4.4 No recognition of timing difference on goodwill recognised in a business combination.

29.4.2.4.0 Initial recognition exception.

29.4.2.4.1 What tax rate to use.

29.4.2.4.1.1 The rate to use for non- depreciable land and investment property.

29.4.2.4.1.2 Review of the recovery of how a deferred tax asset/liability is recovered/settled.

29.4.2.4.1.2.1 Manner of recovery through use.

29.4.2.4.1.2.2 Manner of recovery through sale.

29.4.2.4.1.2.3 Manner of recovery – dual use.

29.4.2.4.1.3 Effect of change in classification of assets.

29.4.2.4.1.4 Determining the value of timing difference.

29.4.2.4.1.4.2 Indexation and how is this accounted for.

29.4.2.4.1.6 Deferred tax impact if unlikely to be taxable/tax deductible on future sale.

29.4.2.4.1.7 Steps involved to working out deferred tax.

29.4.2.4.1.8 Some examples of timing differences.

29.4.2.4.1.8.1.2 Steps to calculate deferred tax for fixed asset timing differences.

29.4.2.4.1.8.1.3 Application of deferred tax to fixed assets.

29.4.2.4.1.8.1.3.1 Deferred tax allowable for tax and depreciable.

29.4.2.4.1.8.1.3.2 Asset allowable for tax, depreciable and revalued.

29.4.2.4.1.8.1.3.3.1 Treatment of depreciation on upward revaluation.

29.4.2.4.1.8.2 Accounting for deferred tax on non-depreciable land.

29.4.2.4.1.8.3 Deferred tax on investment properties carried at fair value.

29.4.2.4.1.8.4 Pension contributions/royalty charges.

29.4.2.4.1.8.5 Finance leases.

29.4.2.4.1.8.6 Unrelieved tax losses.

29.4.2.4.1.8.6.1 Ability to recognise unutilised losses against other deferred tax liabilities.

29.4.2.4.1.8.7 Fair value adjustments.

29.4.2.4.1.8.7.1 Further exampls of deferred tax where fair value adjustments are recognised.

29.4.2.4.1.8.7.1.1 Non-puttable ordinary shares and deferred tax.

29.4.2.4.1.8.7.1.2 Interest rate swaps – derivatives and deferred tax.

29.4.2.4.1.8.7.1.3 Forward foreign currency contract and deferred tax.

29.4.2.4.1.8.8 Defined benefit obligations.

29.4.2.4.1.8.9 Consolidation adjustments.

29.4.2.4.1.8.10 Investment in associates, joint ventures, subsidiaries in consolidated accounts.

29.42.4.1.8.11 Assets partly allowable for tax purposes.

29.4.2.4.1.8.12 Items expensed which are capital in nature (allowable for capital allowances).

29.4.2.4.1.8.13 Transition adjustments to a new GAAP.

29.5 Measurement of deferred tax on business combinations.

29.5.1 Extract from FRS102: Section 29.11.

29.6 Withholding tax on dividends.

29.6.1 Extract from FRS102: Section 29.18-29.19.

29.7.1 Extract from FRS102: Section 29.24-29.24A.

29.7.2.1 Off setting current tax.

29.7.2.2 Offsetting deferred tax assets and liabilities.

29.8 Value Added Tax (“VAT”) and other similar taxes.

29.8.1 Extract from FRS 102: Section 29.20.

29.9 Presentation and disclosures.

29.9.1 Extract from FRS102: Section 29.21-29.27.

29.9.2.1.1 Where to recognise the tax charge/credits in the statements of comprehensive income.

29.9.2.1.2 Where to recognise the tax asset or liability on the balance sheet.

29.9.2.2.2 Accounting Policies.

29.9.2.2.3 Notes to the financial statements.

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.17.6″]

The below extracts and guidance is applicable for periods beginning before 1 January 2019 and are based on the September 2015 version of FRS 102. For periods beginning on or after 1 January 2019, the March 2018 version of FRS 102 applies which incorporates the changes made by the Triennial review of FRS 102. Note the March 2018 version of FRS 102 can be voluntarily applies for periods beginning before 1 January 2019. For the extracts from the March 2018 version of FRS 102 and the related guidance please click on the following link. For details of a summary of the main changes as a result of the triennial review please see the following link.

29.4 Recognition of deferred tax

29.4.1 Extract from FRS102: Section 29.6–29.17

Timing differences

29.6 Deferred tax shall be recognised in respect of all timing differences at the reporting date, except as otherwise required by paragraphs 29.7 to 29.9 and 29.11 below. Timing differences are differences between taxable profits and total comprehensive income as stated in the financial statements that arise from the inclusion of income and expenses in tax assessments in periods different from those in which they are recognised in financial statements.

29.7 Unrelieved tax losses and other deferred tax assets shall be recognised only to the extent that it is probable that they will be recovered against the reversal of deferred tax liabilities or other future taxable profits (the very existence of unrelieved tax losses is strong evidence that there may not be other future taxable profits against which the losses will be relieved).

29.8 Deferred tax shall be recognised when the tax allowances for the cost of a fixed asset are received before or after the depreciation of the fixed asset is recognised in profit or loss. If and when all conditions for retaining the tax allowances have been met, the deferred tax shall be reversed.

29.9 Deferred tax shall be recognised when income or expenses from a subsidiary, associate, branch, or interest in joint venture have been recognised in the financial statements, and will be assessed to or allowed for tax in a future period, except where: (a) the reporting entity is able to control the reversal of the timing difference; and (b) it is probable that the timing difference will not reverse in the foreseeable future. Such timing differences may arise, for example, where there are undistributed profits in a subsidiary, associate, branch or interest in a joint venture.

Permanent differences

29.10 Permanent differences arise because certain types of income and expenses are non-taxable or disallowable, or because certain tax charges or allowances are greater or smaller than the corresponding income or expense in the financial statements. Deferred tax shall not be recognised on permanent differences except for circumstances set out in paragraph 29.11.

Business combinations

29.11 When the amount that can be deducted for tax for an asset (other than goodwill) that is recognised in a business combination is less (more) than the value at which it is recognised, a deferred tax liability (asset) shall be recognised for the additional tax that will be paid (avoided) in respect of that difference. Similarly, a deferred tax asset (liability) shall be recognised for the additional tax that will be avoided (paid) because of a difference between the value at which a liability is recognised and the amount that will be assessed for tax. The amount attributed to goodwill shall be adjusted by the amount of deferred tax recognised.

Measurement of deferred tax

29.12 An entity shall measure a deferred tax liability (asset) using the tax rates and laws that have been enacted or substantively enacted by the reporting date that are expected to apply to the reversal of the timing difference except for the cases dealt with in paragraphs 29.15 and 29.16 below.

29.13 When different tax rates apply to different levels of taxable profit, an entity shall measure deferred tax expense (income) and related deferred tax liabilities (assets) using the average enacted or substantively enacted rates that it expects to be applicable to the taxable profit (tax loss) of the periods in which it expects the deferred tax asset to be realised or the deferred tax liability to be settled.

29.14 In some jurisdictions, income taxes are payable at a higher or lower rate if part or all of the profit or retained earnings is paid out as a dividend to shareholders of the entity. In other jurisdictions, income taxes may be refundable or payable if part or all of the profit or retained earnings is paid out as a dividend to shareholders of the entity. In both of those circumstances, an entity shall measure current and deferred taxes at the tax rate applicable to undistributed profits until the entity recognises a liability to pay a dividend. When the entity recognises a liability to pay a dividend, it shall recognise the resulting current or deferred tax liability (asset), and the related tax expense (income).

29.15 Deferred tax relating to a non-depreciable asset that is measured using the revaluation model in Section 17 Property, Plant and Equipment shall be measured using the tax rates and allowances that apply to the sale of the asset.

29.16 Deferred tax relating to investment property that is measured at fair value in accordance with Section 16 Investment Property shall be measured using the tax rates and allowances that apply to sale of the asset, except for investment property that has a limited useful life and is held within a business model whose objective is to consume substantially all of the economic benefits embodied in the property over time.

29.17 An entity shall not discount current or deferred tax assets and liabilities

29.4.2 OmniPro comment

29.4.2.1 Deferred tax defined and the purpose of deferred tax

Appendix 1 of FRS 102 defines deferred tax as the income tax payable /(recoverable) in respect of the taxable profit (or tax less) for future reporting periods as a result of past transactions of events. Deferred tax is recognised on a timing difference plus approach. Deferred tax represents the future consequences of transactions and events recognised in the current and prior periods financial statements. The reason why deferred tax is recognised is due to the fact that this future tax will be payable even where the company decides to cease trading i.e. it is certain the future tax will have to be paid or will be refundable. The provision for deferred tax ensures the tax charge shown eliminates any timing differences i.e. the tax charge would usually be the profit before tax multiplied by the tax rate less any permanent differences. Any timing differences are deferred on the balance sheet.

29.4.2.2 Permanent differences

29.4.2.2.1 Analysis

Permanent differences occur as a result of certain types of expenditure/income being posted as a charge/credit in the profit and loss but are added back/deducted in the tax computation as it was never tax deductible/taxable for tax purposes i.e. the tax authorities will never allow a deduction for these costs. As these are permanent they do not come within the scope of deferred tax unless they arise on a business combination as stated section 29.10 and 29.11 of FRS 102 above.

29.4.2.2.1.1 The one exception for recognising a permanent difference for deferred tax

Section 29.10 of FRS 102 makes it clear that deferred tax can only be recognised on permanent differences where they arise on a business combination (all other times permanent differences are ignored) see details at 29.5.2.

29.4.2.2.1.2 Examples of temporary differences for deferred tax purposes

Examples of permanent differences are:

- Customer entertainment

- Charitable donations not above a certain value

- Amortisation/depreciation on assets not allowable for capital allowance purposes (on initial recognition only if revolution policy chosen)

- Expenses deemed to be capital in nature for tax purposes, but no capital allowances are allowed to be claimed

- Certain payments made on leases

- Write off/provisions against investments, fixed assets (where they are not allowable for capital allowance purposes and/or have not been revalued and are not capital assets for capital gains tax purposes))

- Deemed debit/credit posted to profit and loss on recognition of a loan given/received at non-market rates (assuming the company is not engaged in the giving and receiving of loans as its trade)

29.4.2.3 Temporary differences

29.4.2.3.1 Temporary differences defined

As detailed in section 29.6 of FRS 102 timing differences arise due to expenses being charged to the profit and loss account or ‘other comprehensive income’ in a period but are not allowable for tax purposes until future periods or where the expense has been allowed for tax purposes but has not hit the profit and loss account by the year end.

29.4.2.3.2 Definition of deferred tax assets and instances where they arise

The Glossary to FRS 102 defines a deferred tax asset as income tax recoverable in future reporting periods in respect of: (a) future tax consequences of transactions and events recognised in the financial statements of the current and previous periods; (b) the carry forward of unused tax losses; and (c) the carry forward of unused tax credits.

29.4.2.3.2.1 When does a deferred tax asset exist including examples

A deferred tax asset exists where:

– The company has charged an expense/deduction to the profit and loss account during the period but it has not been allowed for tax purposes in that period but it will be allowed as a tax deduction in the future (i.e. the tax authorities will allow the deduction in the future). Examples would include:

– Instances where capital allowances are claimed over a life greater than the life the asset is depreciated over. (i.e tax written down value greater than NBV)

– Losses carried forward

– Pension deductions only allowed on a paid basis

– General accruals/provisions not allowable until paid

– Capital items expensed, added back in the tax comp but allowed for capital allowance purposes

– Revaluation of assets downward

– Profit/loss on disposal of assets allowed for capital allowance purposes

See further details at 29.4.2.4.1.8

29.4.2.3.3 Definition of deferred tax liabilities and instances where they arise

The Glossary to FRS 102 defines a deferred tax liability as Income tax payable in future reporting periods in respect of future tax consequences of transactions and events recognised in the financial statements of the current and previous periods.

29.4.2.3.3.1 When does a deferred tax liability exist including examples

A deferred tax liability exists where:

– The company has obtained a tax deduction in the current or prior accounting period but it has not been charged to the profit and loss account at that time. Examples would include:

– Instances where capital allowances are claimed over a life shorter than the life the asset is depreciated over (i.e tax written down value less than NBV)

– Income/gain has been recognised in the current or prior accounting period but was not taxed in the tax computation in that period but will be taxable at a future time e.g. interest receivable or revaluation of assets upwards. See further details at 29.4.2.4.1.8

29.4.2.3.4 Recognition of timing differences – the rules.

Section 29.6 of FRS 102 requires all timing differences to be recognised as deferred tax on the balance sheet with the exception of timing differences arising from:

29.4.2.3.4.1 Unrelieved tax losses – The rule recognition or not

1) Unrelieved tax losses (i.e. deferred tax asset) where it is not probable that future taxable profits will exist to utilise these tax losses carried forward or stated in section 29.7 of FRS 102. Before these losses can be recognised as a deferred tax asset it must be probable (more likely than not that there will be taxable profits to utilise the tax losses). Section 29.7 of FRS 102 makes it clear that the very existence of unrelieved tax losses is strong evidence that there may not be other future taxable profits against which the losses can be relieved. Therefore, when assessing whether the deferred tax asset should be recognised care should to be taken to review future projections (it is not enough to just look at prior year results as a basis for future years) and assess how long it will take to recover these losses based on those projections or if in fact it is possible to recover these. Consideration also needs to be given as to whether the losses expire at a point in time. It may be possible to look at future tax strategies to prove the recoverability of losses forward if it is probable these will be put in place.

Example 6: Losses forward – recognition of deferred tax

Company A has losses forward of CU200,000. The projected profits over the next 6 years is CU100,000. In this example given that it is going to take 6 years to recover only CU100,000 of the losses, the entity should at a maximum recognise a deferred tax asset of CU100,000. Whether to recognise this CU100,000 will depend on the strength of projections and how accurate the Company has been with projecting in the past.

29.4.2.3.4.1.1 Deferred tax (inc losses) recoverable against deferred tax liabilities

Where there are deferred tax liabilities in addition to deferred tax assets than as long as the asset and liabilities arise from the same tax district and are the same type (e.g. deferred tax liabilities and deferred tax assets relate to profits taxable at the same tax rate or deferred tax liabilities and assets which relate to capital (CGT) items. You cannot mix passive income items with trade items or capital items with trader or passive items) then as long as it is probable that the deferred tax assets (e.g. Losses) will be relieved against the reversal of the deferred tax liabilities, the deferred tax assets can be recognised. Section 29.7 and 29.24A of FRS 102 refers. Note however where the deferred tax assets exceed the deferred tax liability then the deferred tax assets should only be recognised to the extent that the net deferred tax overall is nil. Any further amount of the deferred tax assets should only be recognised if it is probable that there will be future taxable profits to utulise the deferred tax assets.

Example 7: Deferred tax liabilities available to utilise deferred tax assets

Company A has losses in the year of CU100,000 in tax terms which therefore is a deferred tax asset. The company also has deferred tax liabilities of CU 150000 which are trade related to the net book value of plant being in excess of tax written value. In this case assuming the reversal of the deferred tax liability will reverse simultaneously (with the losses forward) then the entity should recognise a deferred tax liability at CU50,000 in line with section 29.7 of FRS 102 and section 29.24A of FRS 102. If in this example the losses in tax terms were CU200,000 then only CU150,000 of those losses should be set against the liability (assuming it is probable they will be recovered through the reversal of the deferred tax liability) so as to come to a CUNIL deferred tax balance. Whether the additional CU50000 is recognised as a deferred tax asset will depend on whether it is probable there will be future taxable profits to utilise the losses forward. If these were pension contributions that made up the deferred tax assets the same process would need to be done to access how much can be recognised. The adequacy of providing for a deferred tax asset in relation to unrelieved assets should be carried out at each reporting period.

29.4.2.3.4.2 Where conditions for retaining the tax allowances have been met – no requirement to recognise timing differences.

2) Assets where the conditions for retaining the tax allowances have been met. This applies where an asset has a certain tax life and after that tax life has elapsed no tax claw back arises. Examples where this applies would include: capital allowances on hotels, industrial buildings, certain property-based incentives.

Example 8: Conditions for retaining tax allowances have been met

Company A purchased an industrial property 25 years ago for CU500,000. This property is being depreciated for tax purposes over 50 years but capital allowances are being claimed for tax purposes over 25 years after which no claw back arises for previous tax deductions claimed. Assume the deferred tax rate is 10%. Therefore in the accounts at the end of year 25 the deferred tax liability recognised was:

| CU | |

| NBV Per Accounts (CU500,000/50yrs*25yrs)= | 250,000 |

| Tax Written Down Value (CU500,000/25yrs*0yr left)= | (0 ) |

| Deferred Tax Liability | 250,000 |

| Deferred Tax Rate @ 10% | 25,000 |

At the end of year 26, the previous years deferred tax liability can be released in full as the tax life is over and no balancing charge/allowance can arises following a sale.

29.4.2.3.4.3 Non-recognition of timing difference arising as a result of associates/JV’s branches subsidiaries in consolidated financial statements where certain conditions exist

3) Income/expenses from an associate, joint venture, branch or subsidiary recognised in the group’s consolidated financial statements will be assessed for tax purposes in the future but the reporting entity can control the reversal of the timing difference and it is probable the timing difference will not reverse in the foreseeable future. This would be applicable where there are undistributed profits in the associate, joint venture, branch or subsidiary.

29.4.2.3.4.4 No recognition of timing difference on goodwill recognised in a business combination

4.) Goodwill recognised in a business combination. As detailed in section 29.11 of FRS 102 a temporary difference arising from the recognition of goodwill in a business combination cannot be recognised. Note however permanent differences arising on differences other than goodwill must be recognised. See details at 29.5.2.

29.4.2.4 Measurement

29.4.2.4.0 Initial recognition exception

Any temporary difference on initial recognition is ignored for deferred tax purposes as it is treated as permanent (other than in the case of business contributions detailed in 29.5.2). See an example at same at 29.4.2.4.1.8.11 and 29.4.2.4.1.2.3

29.4.2.4.1 What tax rate to use

Section 29.12 of FRS 102 states that deferred tax should be measured at the tax rates enacted or substantively enacted at the balance sheet date. See example 1 at 29.2.2.1 above where this is illustrated. Note if an item is not taxable based on how it is to be realized then no deferred tax arises. In measuring deferred tax an entity is required to apply the enacted rate that is expected to apply to the reversal of the timing difference (i.e. the sales tax rate or the trading rate), except in the case of timing differences arising from the:

- revaluation of non-depreciable assets where a revaluation option taken. In this case the sales tax rate (the tax rate on sale of the asset) should be used to measure the deferred tax liability as required by Section 29.15 of FRS 102. An example of this type of asset is land.

- recognition of investment properties at fair value (which is accounted for in accordance with Section 16). In this case the sales tax rate (the tax rate on sale of the asset) should be used to measure the deferred tax liability as required by Section 29.16 of FRS 102.

29.4.2.4.1.1 The rate to use for non- depreciable land and investment property

Section 29.15 and 29.16 of FRS 102 requires non-depreciable land and investment property to be measured at the sales tax rate. For all other assets the rate to use is the rate the deferred tax assets is realised/settled.

29.4.2.4.1.2 Review of the recovery of how a deferred tax asset/liability is recovered/settled

Other than the two items mentioned at 29.4.2.4.1.1 consideration of the manner in which the asset will be recovered/liability settled should be given. The manner in which the asset can be recovered, or liability settled is key in deciding whether to apply the sales tax rate or the trading tax rate. The entity should consider the expected manner of recovery at each reporting date to assess if it is necessary to change the rate used. There are three ways in which an asset can be recovered:

- through use in the business (see 29.4.2.4.1.2.2) or

- through sale of the asset (see 29.4.2.1.1.2.3) or

- through use and sale of the asset (see 29.4.2.4.1.2.4)

Section 29 does not specifically deal with the above in detail.

29.4.2.4.1.2.1 Manner of recovery through use

Where the asset is expected to be recovered through use, then it would be reflected in the depreciation charged during the assets life and it would usually be expected to have a nil residual value. The rate to be used in measuring deferred tax would be the trade rate in this instance (i.e. 12.5% in Ireland or 25% where the entity carries on a passive trade). Examples of assets under this class may include:

- depreciable assets used in its trade

- current assets and liabilities relating to the trade

29.4.2.4.1.2.2 Manner of recovery through sale

Where the asset is expected to be recovered through eventual sale, then the tax rate to use would be the rate that would be applicable on sale (i.e. the capital gains tax rate which would be 33% in Ireland or if there are special tyes of long term investments exit tax at 25% may apply). Examples of assets under this class may include:

- investments in equities (<20% ownership)

- investment in subsidiaries/associates/joint ventures

- investment property

- land

29.4.2.4.1.2.3 Manner of recovery – dual use

Where the asset has a dual use, Section 29 does not detail the rate that should be used so therefore it is an accounting policy choice as to how best to treat such a situation and judgement will be required. It may be necessary to ascertain the residual value and apply the sales tax rate on this element and apply the trading tax rate to the element that is depreciated. In developing an accounting policy an entity should use the guidance with regard to the concepts in Section 2 of FRS 102 or alternatively look to the guidance in IAS 12 in IFRS as permitted by Section 10 of FRS 102. The below illustrates the guidance from IFRS.

Example 9: Dual use manner of recovery

Company A acquired a property and some land for €200,000 a number of years ago which is used for the purposes of the trade. The cost was split CU150,000 to the property and CU50,000 to the land. The residual value of the property at the end of its useful life was estimated at CU5,000, therefore the depreciable amount was CU145,000 in relation to the property. The company obtained capital allowances on CU150,000 of the premises cost (CU50,000 was not allowed). A number of years ago the property and land was revalued to CU160,000 and CU60,000 respectively. The carrying amount at the reporting date of the land was CU60,000 and the property was CU100,000. The new residual estimated value at that date was CU6,000 and the tax written down value was CU40,000. The carrying amount of the unallowed portion on the property following the previous revaluation was CU30.000 (if no revaluation had of been undertaken the carrying amount would have been CU20,000). As there is a residual value this will be subject to CGT as it is a capital asset. As Section 29 does not deal with how to account for a dual use asset the entity has decided to follow the guidance in IFRS. Assume a deferred tax rate of 10%.

Deferred tax at trading rate on the premises

| CU | |

| Carrying amount of premises | 100,000 |

| Less carrying amount of assets not allowable for Capital allowances purposes (using original cost figures where a revaluation has arisen, if no revaluation then this amount will already be the original cost) | (20,000) |

| Less residual amount (including any revaluation element included in carrying amount not extracted in line above (amount of carrying amounts realised through sale | (6,000) |

| 74,000 | |

| Less TWDV | (40,000) |

| Deferred tax (asset)/liability | 34,000 |

| Deferred tax at 10% | 3,400 |

If in this example there was a deferred tax asset you would only recognise this asset if it can be recovered through future profits or can be set against other deferred tax liabilities which can be set off against the capital allowances. If it cannot be utilised by future profits – recognise no deferred tax asset should be recognised. Note Section 29 does not state how dual use should be accounted for therefore the above example illustrates the guidance in IFRS for a dual use asset where capital allowances are being claimed. You could possibly ignore taking the residual amount off here and possible not calculate the capital deferred tax asset/liability as there is no guidance in FRS 102.

Deferred tax at CGT rate on residual value of premises

| Residual amount included in carrying amount of premises inc. any Movement on residual amount due to revaluations | 6,000 |

| Tax cost inc. indexation | (150,000) |

| Difference | (144,000) |

| Add timing difference on initial recognition (no Deferred tax recognised on this) (original cost of whole asset of CU150,000-CU5,000 residual value) | 145,000 |

| Deferred tax asset | 1,000 |

| Deferred tax 33% | 330 |

Here this is a deferred asset. This can only be recognised if it can be recovered through future chargeable gains or can be set against other capital deferred tax liabilities. As there is a capital deferred tax liability on the land as calculated below, this can be set off against this assuming the land and buildings will be sold at the same time. Deferred tax at CGT rate on land

| Carrying amount of land inc. any revaluations | 60,000 |

| Less carrying amount of assets not allowable for Capital allowances purposes (using original cost figures where a revaluation has arisen, if no revaluation then this amount will already be the original cost) | (50,000) |

| 10,000 | |

| Less TWDV | (-) |

| Deferred tax (asset)/liability | 10,000 |

| Deferred tax at 10% | 1,000 |

If the capital deferred tax at CGT rate were a liability on the land, then this gain could be set against that liability assuming that the premises and land would be sold at the same time. This would also be the case if the residual value was nil here but the premises was sold at the end of its life.

29.4.2.4.1.3 Effect of change in classification of assets

Section 29 provides no detail on what rate is to be used where investment property is classified from investment properties due to an inability to measure fair value due to undue cost or effort. In this particular circumstance consideration should be given to the manner in which the asset can be recovered. Given that this property had been measured at the sales tax rate while accounted for as an investment property asset under Section 16, it would not be unreasonable to assume the sales tax rate should be used in this instance.

29.4.2.4.1.4 Determining the value of timing difference

29.4.2.4.1.4.1 Overview

The amount to be considered for deferred tax is the difference between the tax base cost and the assets carrying amount. The tax base cost can be the tax written down value where capital allowances can be claimed on the assets or base cost of the asset where the asset is to be recovered through a sale.

29.4.2.4.1.4.2 Indexation and how is this accounted for

Where deferred tax is measured on a sales tax rate basis, Section 29 would require that the tax cost would incorporate any indexation allowed for tax purposes. Indexation is not applicable for assets/liabilities that we recognise The difference between the carrying amount of the asset in the accounts and the indexed base cost is the deferred tax timing difference. However indexation cannot create or increase a loss. Note indexation only applies where the timing difference is not recovered through use. In the foregoing examples we have ignored inflation.

Example 10: Indexation of base cost – non depreciable asset

Company A purchased a piece of land for CU100,000 in 1990. Assume the carrying amount in the accounts is CU500,000 following a revaluation. Under local tax rules, indexation is allowed to be applied when determining the tax to be paid on the sale of the land. If we assume that indexation allowed is 2.5 times the original cost and the deferred tax rate on sale is 20%, the deferred tax asset to be recognised at the year end is: CU500,000 – (CU100,000*2.5 times)= CU250,000 * the sales tax rate of 20%= CU50,000 Note if no revaluation had of been booked in the accounts, then no deferred tax would be recognised as there is no difference between the carrying amount in the accounts and the tax base cost. Also if the above was a loss, the loss would be restricted to the actual loss excluding indexation. Whether a deferred tax asset should be recognised for the loss will be determined by whether the entity believes the capital loss can be utilised in the foreseeable future.

29.4.2.4.1.5 Discounting

As per Section 29.17 of FRS 102, deferred tax cannot be discounted.

29.4.2.4.1.6 Deferred tax impact if unlikely to be taxable/tax deductible on future sale

Note in assessing whether deferred tax needs to be recognised, one should assess if tax is payable on future settlement. If an item is exempt from tax then no deferred tax needs to be recognised (e.g. CGT exempt on certain assets purchased during a certain period).

29.4.2.4.1.7 Steps involved to working out deferred tax

- Identify the timing differences at the balance sheet date

- Quantify the timing difference and whether it is a deferred tax asset or liability.

- Calculate the timing difference before applying the deferred tax rate

- Apply the tax rate to step 3

- Decide where to post the deferred tax. The deferred tax posting should be posted to either the P&L, OCI/revaluation reserve. The posting will be to wherever the depreciation/revaluation etc was posted.

See application of the above at 29.4.2.4.1.8

29.4.2.4.1.8 Some examples of timing differences

29.4.2.4.1.8.1 Timing differences on depreciable fixed assets including revaluations (accelerated/decelerated capital allowances).

A timing differences arises on property, plant and equipment due to the fact that an item of PPE might be depreciated in the accounts at a different rate to which a deduction is allowed for tax purposes in the form of capital allowances. The general rule in this regard is:

- Where the NBV of the PPE > the tax written down value (TWDV) of PPE for tax purposes, then a deferred tax liability exists. The reason for this being a liability is due to the fact that in the future there will be more depreciation charged to the accounts which will not be allowed for tax purposes.

- Where the NBV of the PPE < the tax written down value (TWDV) of PPE for tax purposes, then a deferred tax asset exists. The reason for this being an asset is due to the fact that in the future there will be less depreciation charged to the accounts but there will still be a deduction allowed for tax purposes.

29.4.2.4.1.8.1.2 Steps to calculate deferred tax for fixed asset timing differences

Where an asset is allowable for tax purposes the way in which the deferred tax should be calculated at each year end is:

- Determine the NBV of the assets at period end

- Deduct the net book value of assets not allowable for capital allowance purposes (the net book value here should exclude revaluations on such assets. – i.e. it should be the historical cost less accumulated depreciation on that cost) – this includes NBV of assets held on finance lease

- Determine the TWDV (or the tax base cost) of the asset at period end

- Take the NBV (that being step 1 less step 2 above) from the TWDV as determined in step 1 to give the deferred tax asset/liability or for costs which have already been expensed and are being allowed differently for tax purposes take the actual amount to be deducted/taxed in the future

- If NBV>TWDV then a deferred tax liability exists and vice versa.

- Apply the deferred tax rate based on the expected use of the asset. The deferred tax should follow where the depreciation/revaluation was posted

- Post the difference between the prior year deferred tax and the current year as a charge/credit to P&L.

See application of the above guidance at 29.4.2.4.1.8.1.3 29.4.2.4.1.8.1.3 Application of deferred tax to fixed assets 29.4.2.4.1.8.1.3.1 Deferred tax allowable for tax and depreciable

Example 11: Allowable for tax and depreciable

At the start of year 1, Company A purchased a machine for CU100,000 which is fully allowable for capital allowance purposes. The asset is written off over a life of 10 years for accounting purposes and a life of 8 years for tax purposes. As a result of the mismatch in the life for tax and accounting purposes a timing difference arises as the depreciation charged to the profit and loss each year differs from the capital allowances used to reduce profit in the tax computation for that year. Assume trading tax rate of 10% and the profit before tax is CU50,000. To determine the timing difference at the end of year 1, do the following:

| CU | |

| NBV of Machine (CU100,000/10yrs*9yrs)= | 90,000 |

| TWDV of Machine (CU100,000/8yrs*7yrs)= | (87,500) |

| Deferred Tax Timing Difference – Liability | 2,500 |

| Deferred Tax Liability (CU2,500*10%) | 250 |

Journal to post at the end of year 1 is:

| CU | CU | |

| Dr Deferred Tax in Profit and Loss | 250 | |

| Cr Deferred Tax Liability | 250 |

Being journal to recognise deferred tax. The reason for the difference is that depreciation was booked in the accounts of CU10,000 in the year whereas CU12,500 was allowed in the tax computation. Applying the accounting profit of CU50,000 and taking the current tax rate at 10% would give a profit of CU5,000 to be shown in the tax line in the accounts. However the actual tax charge is CU4,750 (50,000 accounting profit + depreciation addback of CU10,000 less capital allowance deduction of CU12,500 multiplied by 10%). Therefore by accounting for the deferred tax this CU4,750 is increased to CU5,000 so as to eliminate the effect of this timing difference in the P&L for the year which is what Section 29 tries to achieve. The deferred tax to be recognised in the profit and loss in year 2 is obtained by taking the deferred tax timing difference at the end of year 2 from the timing difference at the end of year 1.

| Year 1 | Year 2 | |

| NBV (CU100,000/10yrs by number of years remaining) | CU90,000 | CU80,000 |

| TWDV (CU100,000/8yrs by number of years remaining) | CU87,500 | CU75,000 |

| Deferred Tax Timing Difference Liability | CU2,500 | CU5,000 |

| Deferred Tax Liability (amount*10%) | CU250 | CU500 |

Journal to post at the end of year 2 is:

| CU | CU | |

| Dr Deferred Tax in Profit and Loss | 250 | |

| Cr Deferred Tax Liability (CU500-CU250) | 250 |

Being journal to recognise deferred tax.

29.4.2.4.1.8.1.3.2 Asset allowable for tax, depreciable and revalued

Example 12: Asset allowable for tax, depreciable and revalued

At the start of year 1, Company A purchased an industrial building for CU100,000 which is fully allowable for capital allowance purposes. The asset is written off over a life of 10 years for accounting purposes and a life of 8 years for tax purposes. At the start of year 2 the asset was revalued to CU150,000. As a result of the mismatch in the life for tax and accounting purposes a timing difference arises as the depreciation charged to the profit and loss each year differs from the capital allowances used to reduce profit in the tax computation. Assume trading tax rate of 10%. To determine the timing difference, do the following: The deferred tax liability at the end of year 1 is as per example 6 above as the numbers are the same. At the end of year 2 the timing difference is as follows:

| Cost | |

| NBV of building | CU133,333* |

| TWDV of Building (CU100,000/8yrs*6yrs)= | (CU75,000) |

| Deferred Tax Timing Difference – Liability | CU58,333 |

| Deferred Tax Liability (CU58,333*10%) | CU5,833 |

*carrying amount of the building at the end of year 1 was CU90,000 plus the revaluation at start of year 2 to bring the value up to CU150,000. Therefore an adjustment of CU60,000 was posted to the revaluation reserve. At time of revaluation the asset is depreciated over the remaining life of 9 years. NBV at the end of year 2 is therefore = CU150,000/9yrs*8yrs=CU133,333 Posting of movement in deferred tax: Movement = deferred tax liability at end of year 1 of CU250 less deferred tax liability at end year 2 of CU5,833 However where a revaluation is recognised, the deferred tax on initial recognition of the CU60,000 follows how the revaluation was treated under Section 17. Section 17 requires the revaluation to be posted to OCI/revaluation reserve. Therefore the deferred tax on initial recognition of CU6,000 (CU60,000*10%) should be debited to the revaluation reserve/OCI. The journal required at the end of year 2 is:

| CU | CU | |

| Dr Revaluation Reserve | 6,000 | |

| Cr Deferred Tax Liability | 5,583* | |

| Cr Deferred Tax in P&L | 417 |

Being journal to correctly classify the deferred tax on initial recognition to the revaluation reserve and the balance to the profit and loss (CU417 is the difference between the depreciation charge posted in the year of CU16,667 (CU150,000/9yrs) less the capital allowance claimed of CU12,500 by the 10% tax rate). For year 3, the deferred tax journal will be CU417

29.4.2.4.1.8.1.3.3. Accounting for revaluations and subsequent movements including deferred tax – depreciable/not allowable for capital allowance purposes

Example 13: Accounting for revaluations and subsequent movements including deferred tax – depreciable/not allowable for capital allowance purposes

Company A has adopted a policy of revaluation on its PPE. The company purchased an asset for CU500,000 at the start of year 1 and determined the useful life to be 20 years. By the end of year one, there were indicators of a change in market conditions and a valuation exercise was performed which showed the market value at CU525,000. At the end of year 4, a further valuation was performed as the difference in fair value and the carrying value was material, at this time the value was reduced to CU300,000. In year 8, a further valuation was performed which indicated a fair value of CU600,000. Assume the deferred tax rate is 10% (this is not the sales rate as the asset is depreciated) and the asset does not qualify for capital allowances. Assume the depreciation on the revalued amount is transferred from the revaluation reserve to profit and loss reserves on a year by year basis as the depreciation is charged. Company A would account for the changes in value in the following way:

At end of year 1: The carrying value of the asset is CU475,000 (i.e. CU500,000 less depreciation for one year of CU25,000 (CU500,000/20yrs))

| CU | CU | |

| Dr Fixed Assets (CU525,000-CU475,000) | 50,000 | |

| Cr OCI/Revaluation Reserve | 50,000 |

From then on the carrying amount of CU525,000 will be depreciated over the remaining life of 19 years (CU27,632 per annum).

Deferred tax

| CU | CU | |

| Dr OCI/Revaluation Reserve | 5,000 | |

| Cr Deferred Tax in Balance Sheet (CU50,000 *10%) | 5,000 |

Therefore, the net amount posted to the revaluation reserve is CU45,000 (CU50,000-CU5,000). For year 2 to year 4, the deferred tax will be reduced and posted to the profit and loss account in line with the additional depreciation charged on the uplift in value of CU2,632 (i.e. CU27,632 less depreciation under cost basis of CU25,000).

At end of year 4: The carrying value of the asset is CU442,104 (i.e. CU525,000 less depreciation of CU27,632 for three years totalling CU82,896)

| CU | CU | |

| Dr Profit and Loss (CU142,104-CU42,104) | 100,000 | |

| Dr Revaluation Reserve (reversal of amount recognised in yr 1) net of depreciation charged on revalued amount for three years and the related deferred tax recognised i.e. (2,632)x3 | 42,104 | |

| Cr Fixed Assets (CU442,104-CU300,000) | 142,104 |

From then on the carrying amount of CU300,000 will be depreciated over the remaining life of 16 years (CU18,750 per annum).

Deferred tax

| CU | CU | |

| Dr Deferred Tax in Balance Sheet (CU5,000 less ((CU2,632 * 10%) * 3 years) = CU789) | 4,211 | |

| Cr OCI/Revaluation Reserve | 4,211 |

Note deferred tax asset on the write down is not recognised on the basis that it is not reasonable that future economic benefits will be derived from the capital losses At end of year 8: The carrying value of the asset is CU225,000 (i.e. CU300,000 less depreciation of CU18,750 for 4 years totalling CU75,000)

| CU | CU | |

| Dr Fixed Assets (CU600,000 mkt value-CU225,000 NBV) | 375,000 | |

| Cr Profit and Loss (CU100,000 previously posted-CU25,000 See note 1) | 75,000 | |

| Cr Revaluation Reserve (CU375,000-CU75,000) | 300,000 |

Deferred tax

| CU | CU | |

| Dr OCI/Revaluation Reserve | 30,000 | |

| Cr Deferred Tax in Balance Sheet ((CU600,000-CU300,000) * 10%) | 30,000 |

From then on the carrying amount of CU600,000 will be depreciated over the remaining life of 12 years. Note 1: The amount that can be credited to the P&L is reduced by the additional depreciation that would have been charged had the asset not been revalued downward in the past i.e. original cost prior to downward revaluation of CU500,000 / useful life of 20 years= CU25,000 * 4 years = CU100,000. This compares to depreciation charged while the asset was being depreciated on the reduced amount of CU75,000 (year 5 to year 8 – CU300,000/UEL of 16 years* 4 years) = CU25,000

29.4.2.4.1.8.1.3.3.1 Treatment of depreciation on upward revaluation

The revaluation surplus included in equity may be transferred directly to retained earnings when the surplus is realised i.e. disposed of, retired from use or as the asset is used by the entity. The transfer is made through reserves and not through the profit and loss. In relation to a transfer being completed as a result of the asset being used by the entity, the amount to be transferred is the difference between the depreciation charged to the profit on loss on the revalued amount compared to the depreciation that would have been charged if revaluation had not occurred.

Example 14: Transfer of depreciation on revalued amount from profit and loss reserves

Taking the above example, at the end of year 2 for the depreciated asset, the additional depreciation charged of CU2,632 (CU27,632-CU25,000) as a result of the revaluation and the related deferred tax credit on this of CU263 (CU2,632*10%), would be transferred from P&L reserves to the revaluation reserve. The below would be shown in the statement of changes to equity in the financial statements.

| Year 2 | |

| Revaluation Reserve at 01/01/Year 2 | 45,000 |

| Transfer from Profit & Loss Reserve (CU2,632-CU263) | (2,369) |

| Revaluation Reserve at 31/12/Year 2 | 42,631 |

| Profit and Loss Reserves at 01/01/Year 2 | 50,000 |

| Transfer to Revaluation Reserve | 2,369 |

| Profit and Loss Reserves Reserve at 31/12/Year 2 | 52,369 |

29.4.2.4.1.8.2 Accounting for deferred tax on non-depreciable land (Section 29.15 of FRS 102)

Example 15: Accounting for initial and subsequent revaluations on non-depreciable assets – i.e. on land

Company A has adopted a policy of revaluation on its PPE. The company purchased land for CU500,000 at the start of year 1. By the end of year 1, there were indications of a change in market conditions and a valuation exercise was performed which showed the market value at CU525,000. At the end of year 4, a further valuation was performed as the difference in fair value and the carrying value was material, at this time the value was reduced to CU300,000. In year 8, a further valuation was performed which indicated a fair value of CU700,000.

Assume the deferred tax rate on a sale is 20% (required to use sales rate under section 29.15 of FRS 102)

Company A would account for the changes in value in the following way:

At end of year 1:

| CU | CU | |

| Dr Fixed Assets (CU525,000-CU500,000) | 25,000 | |

| Cr OCI/Revaluation Reserve | 25,000 |

Deferred tax

| CU | CU | |

| Dr OCI/Revaluation Reserve | 5,000 | |

| Cr Deferred Tax in Balance Sheet (CU25,000* 20%) | 5,000 |

Therefore, the net amount posted to the revaluation reserve is CU20,000.

At end of year 4:

| CU | CU | |

| Dr Profit and Loss | 200,000 | |

| Dr OCI/Revaluation Reserve (being the amount previously recognised) | 25,000 | |

| Cr Fixed Assets (CU525,000-CU300,000) | 225,000 |

Deferred tax

| CU | CU | |

| Dr Deferred Tax in Balance Sheet (CU25,000 * 20%) | 5,000 | |

| Cr OCI/revaluation Reserve (CU25,000 * 20%) | 5,000 |

Note deferred tax asset on the write down of the land is not recognised on the basis that it is not reasonable that future economic benefits will be derived from the capital losses. At end of year 8:

| CU | CU | |

| Dr Fixed Assets (CU700,000-CU300,000) | 400,000 | |

| Cr Profit and Loss (i.e. reversal of amounts previously recognised in P&L) | 200,000 | |

| Cr OCI/Revaluation Reserve (CU400,000-CU200,000) | 200,000 |

Deferred tax

| CU | CU | |

| Dr OCI/Revaluation Reserve (CU200,000 * 20%) | 40,000 | |

| Cr Deferred Tax in Balance Sheet ((CU400,000-CU200,000) * 20%) | 40,000 |

29.4.2.4.1.8.3 Deferred tax on investment properties carried at fair value (Section 29.16 of FRS 102)

Example 16: Fair value movements and deferred tax impact

Company A purchased a property on 1 February 2015 for CU200,000 which was rented out on 1 March 2015 and therefore met the definition of investment property. Legal costs of CU10,000 were incurred on the purchase and property assessment costs were incurred of CU5,000. At the 31 December 2015 the fair value was CU250,000. The sales deferred tax rate is 20%. The accounting requirements are as follows: On initial recognition

| CU | CU | |

| Dr Investment Property (property assessment costs are not directly attributable) | 210,000 | |

| Cr Bank | 210,000 |

On 31 December 2015

| CU | CU | |

| Dr Investment property (CU250,000-CU210,000) | 40,000 | |

| Cr Fair Value Movement on Investment Property in P&L | 40,000 |

| CU | CU | |

| Dr Deferred Tax P&L (CU40,000*20%) | 8,000 | |

| Cr Deferred Tax in Balance Sheet | 8,000 |

Being journal to reflect the movement in fair value during the year including the deferred tax impact Note if the client wants to it may be a good idea to identify the upward movement on the investment property above original cost separately in the profit and loss reserves so that distributable profits can be tracked as this would be non-distributable.

| CU | CU | |

| Dr Profit and loss reserve (40k-8k) | 32,000 | |

| Cr Non-distributable reserve | 32,000 |

On 31 December 2016

| CU | CU | |

| Dr Fair Value Movement on Investment Property in P&L | 60,000 | |

| Cr Investment Property | 60,000 | |

| Dr Deferred Tax in Balance Sheet (CU40,000*20%) | 8,000 | |

| Cr Deferred Tax in P&L | 8,000 |

Being journal to reflect the movement in fair value during the year including the deferred tax impact. Note a deferred tax asset has not been recognised on the basis that there are no other chargeable gains to utilise this loss

29.4.2.4.1.8.3.1 Deferred tax – assessing if tax is payable on settlement/realisation of timing difference

Note deferred tax is only recognised where it will be subject to CGT/sales tax rate on disposal – if the future disposal is exempt then no deferred tax liability should be recognised (e.g. CGT exemption for certain properties purchased during a certain period (7/12/11-31/12/14) if it is probable they will be held for the required period – in this situation only when the exemption period is up (7 years) should deferred tax be recognised and this should be based on the rules stated by tax authorities)

Example 17: Investment Property Fair value movements and deferred tax impact (no tax expected when settled until a certain date)

Company A purchased a property on 30 December 2014 for CU210,000 which was rented out on 1 March 2015 and therefore met the definition of investment property. At the 31 December 2015 the fair value was CU250,000 and did not change during the 7 year period. The sales deferred tax rate is 20% (Capital Gains tax rate). Assume indexation is not applicable. Assume this property meets the requirement for CGT exemption and at 31 December it is probable it will be held until the elapsing of a 7 year period. This property was sold in year 10 and the value remained the same throughout.

The journals required for year ended 31 December 2015 was:

| CU | CU | |

| Dr Investment Property | 40,000 | |

| Cr Fair Value Movement on Investment Property in P&L (other operating income) | 40,000 |

Being journal to reflect the movement in fair value during the year. No deferred tax impact as it is exempt from CGT.

The journals required at 31 December 2021 and before:

No journal required as full gain of €250,000 is exempt.

The journals required at 31 December 2022:

| CU | CU | |

| Dr Deferred Tax in P&L ((CU250,000-210,000) / 8yrs * 1yr )*20%) | 1,000 | |

| Cr Deferred Tax in Balance Sheet | 1,000 |

29.4.2.4.1.8.4 Pension contributions/royalty charges

From an accounting perspective pension costs/royalty fees are accounted for on an accruals basis. However only pension contributions/royalties paid are allowable for tax purposes. This creates a timing difference. In effect it creates a deferred tax asset as the deductions will be allowable in the tax computation when paid.

Example 18: Pensions/royalties

Company A pays pension contributions for its employees. Total charge posted to the profit and loss in the year was CU100,000, CU20,000 of which had not been paid over to the pension scheme by the year end. Assume tax rate of 10%. For tax purposes, only the CU80,000 would be allowable. Therefore the remaining CU20,000 will be allowable when it is paid. On this basis a deferred tax asset of CU2,000 should be recognised to reflect this tax asset. If we assume that a deferred tax asset was in existence in the prior year for CU30,000 in relation to unpaid contributions (i.e. deferred tax asset of CU3,000), the amount to be posted to the profit and loss is a debit of CU1,000 (CU3,000 paid in year re prior year less CU2,000 unpaid at year end).

There are circumstances where a one off lump sum if paid into a pension scheme which is posted directly to the profit and loss for accounting purposes in the period it is paid however for tax purposes it is only allowable over a number of years. This also creates timing differences.

Example 19: Pensions/royalties

Company A paid a one off lump sum to a directors pension scheme of CU200,000 which is expensed in the year for accounting purposes as required. However assume for tax purposes this is only allowed over two years. Assume the tax rate is 10%. Therefore, a deferred tax asset of CU10,000 (CU100,000*10%) should be recognised at the year-end assuming there are other taxable profits to utilise this or there are other deferred tax liabilities to set this against.

29.4.2.4.1.8.5 Finance leases

Timing differences usually arise where entities hold finance leases. From an accounting perspective in accordance with Section 20 of FRS 102 the asset is recognised on the balance sheet and depreciated over its lease life or longer if the asset has a longer useful life, and the interest on the lease charged to the profit and loss. This differs from a tax perspective in that for tax purposes, the depreciation charge, and interest is added back and instead the actual lease payments are allowed. As a result, a deferred tax difference arises.

In order to determine the deferred tax in this case, the following should be performed:

NBV of the leased asset – carrying amount of the finance lease liability on the balance sheet * deferred tax rate.

If NBV of asset is > finance lease liability = deferred tax liability

If NBV of asset is < finance lease liability = deferred tax asset

Example 20: Finance lease

Company A entered into a finance lease for a machine. From an accounting perspective the asset was capitalised as CU30,000 and a finance liability recognised for CU30,000. The total cost including finance charges is CU36,000 over a two year life. At the end of year 1 the NBV of the asset was CU25,000 and carrying amount of the finance lease liability was CU16,000. Details on the postings for the year include:

| Depreciation | CU5,000 |

| Finance Lease Interest | CU4,000 |

| Finance Lease Rentals Paid | CU18,000 |

The deferred tax at the year-end is calculated as follows:

| NBV of Finance Leased Asset (CU30,000-CU5,000 depreciation) | CU25,000 |

| Carrying Amount of Lease (CU30,000-CU18,000 payments+CU4,000 in lease interest) | CU16,000 |

| Deferred Tax Liability | CU9,000 |

| Deferred Tax at 10% | CU900 |

The reason for the timing difference is that CU9,000 was only charged to the P&L (i.e. depreciation of CU5,000 and finance interest of CU4,000) whereas a tax deduction was allowed for CU18,000.

29.4.2.4.1.8.6 Unrelieved tax losses

Timing differences arise due to losses being recognised in the statement of comprehensive income in a year but these losses cannot be utilised for tax purposes until future taxable profits exist. Therefore a deferred tax (see further details at 29.4.2.3.4.1) asset should be recognised for this subject to there being taxable profits to utilise these losses in the future. Before these losses can be recognised as a deferred tax asset it must be probable (more likely than not that there will be taxable profits to utilise the tax losses). Section 29.7of FRS 102 makes it clear that the very existence of unrelieved tax losses is strong evidence that there may not be other future taxable profits against which the losses can be relieved. Therefore, when assessing whether the deferred tax asset should be recognised care should to be taken to review future projections (it is not enough to just look at prior year results as a basis for future years) and assess how long it will take to recover these losses based on those projections or if in fact it is possible to recover these. Consideration also needs to be given as to whether the losses expire at a point in time. It may be possible to look at future tax strategies to prove the recoverability of losses forward if it is probable these will be put in place.

29.4.2.4.1.8.6.1 Ability to recognise unutilised losses against other deferred tax liabilities

Where there are deferred tax liabilities for the same tax district to offset the deferred tax assets these can also be taken into account. See 29.4.2.3.4.1.1 for further details.

29.4.2.4.1.8.7 Fair value adjustments

There may be instances where fair value adjustments result in deferred tax. Examples would include investments carried at market value. The difference between market value and the tax base cost should be accounted for as deferred tax at the sales tax rate and the tax should follow where the market value differences are posted i.e. the profit and loss (section 29.22 of FRS 102 refers). This is the same case for investment properties. Other examples here are derivatives (Deferred tax may arise where hedge accounting is applied). Depending on the tax jurisdiction, deferred tax may be required on other fair value adjustments, however usually for trade related items, the adjustments are taxed/taxable in the period they arise. 29.4.2.4.1.8.3 illustrates this point in relation to investment property.

29.4.2.4.1.8.7.1 Further exampls of deferred tax where fair value adjustments are recognised

Example 21:

29.4.2.4.1.8.7.1.1 Non-puttable ordinary shares and deferred tax

See example at 11.7.2.1.1

Example 22:

29.4.2.4.1.8.7.1.2 Interest rate swaps – derivatives and deferred tax

See example at <JM To UPDATE>

Example 23:

29.4.2.4.1.8.7.1.3 Forward foreign currency contract and deferred tax

See the deferred tax journal at < JM TO UPDATE>

Example 24:

29.4.2.4.1.8.7.1.4 Investment is associates/joint ventures or subsidiaries held at fair value and deferred tax

See the deferred tax impact at <JM TO UPDATE>

Example 25:

29.4.2.4.1.8.7.1.5 Investment in associates, joint venture, subsidiary carry at revolved amount and deferred tax

See example at <JM TO UPDATE>

Example 26:

29.4.2.4.1.8.7.1.6 Complex financial instruments held at fair value through profit and loss and deferred tax

See example at < JM TO UPDATE>

Example 27:

29.4.2.4.1.8.8 Defined benefit obligations

Section 29 requires deferred tax to be recognised on defined benefit obligations. The deferred tax rate to measure the timing difference is the trading tax rate. Note deferred tax assets are only recognised where it is probable that there will be future pension payments into the scheme. The reason why timing difference arise is due to the fact that for tax purposes only pension payments which are made can be deducted from the taxable profits. However in accordance with Section 28 of FRS 102, the estimated current service costs, interest cost, actuarial gain/loss are recognised in the profit and loss/OCI. These costs are added back for tax purposes. These are allowable in the future when pension payments are made. Deferred tax should be recognised at the rate in which the timing difference is expected to reverse. Therefore where the pension scheme is in a deficit it would be the expected timing of future contributions by the employer.

Example 28:

29.4.2.4.1.8.8.1 Presentation of deferred tax on balance sheet and in the statement of comprehensive income

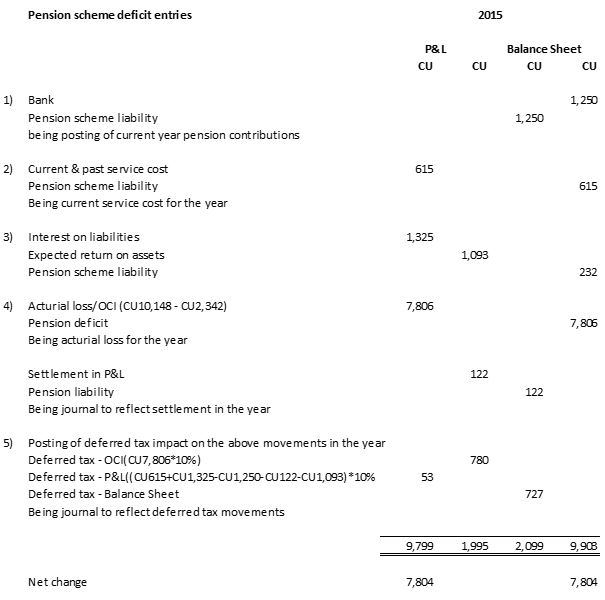

The deferred tax asset should be shown separately within the deferred tax asset line in the balance sheet. It should not be netted against the defined benefit carrying amount. The deferred tax on each posting follows where the journals were posted to recognise the movements on the pension liability/asset during the year. The example below shows the deferred tax calculation and the amount posted to the profit and loss and other comprehensive income in the period. The general rule is that the deferred tax on the actuarial gain/loss and actual versus expected return on plan assets is posted to other comprehensive income. The remainder is posted to the tax line in the profit and loss.

Example 29: Deferred tax on net defined benefit asset/liability

See below extract from an actuarial report detailing the movement in the plan assets during the year. See below the way in which this will be presented in the financial statements and the journals required to reflect these movements. Assume the prior year discount rate was 3.49% and the 2015 discount rate is 2.6%: Changes in the present value of the defined benefit obligation are as follows:

| 2015 | 2014 | |

| CU | CU | |

| Benefit obligation at start of year | (26,724) | (26,236) |

| Current Service Cost | (615) | (689) |

| Interest Cost | (1,325) | (1,270) |

| Plan participants’ contributions | (334) | (334) |

| Actuarial gain/(loss) | (10,148) | 1,601 |

| Benefits paid | 313 | 204 |

| Curtailment | 122 | 0 |

| Benefit obligation at end of year | (38,711) | (26,724) |

Changes in the fair value of plan assets are as follows:

| 2015 | 2014 | |

| CU | CU | |

| Fair Value of Plan Assets at start of year | 18,030 | 17,318 |

| Expected Return on Plan Assets | 1,093 | 1,161 |

| Employer contribution | 1,250 | 1,535 |

| Plan participants’ contributions | 334 | 334 |

| Benefits paid | (313) | (204) |

| Actuarial gain (Actual less expected) | 2,342 | (2,114) |

| Fair Value of Plan Assets at end of year | 22,736 | 18,030 |

The net pension liability as at 31 December 2014 and 2015 is analysed as follows:

| 2015 | 2014 | |

| CU | CU | |

| Present value of defined obligations | (38,711) | (26,724) |

| Fair Value of Plan Assets | 22,736 | 18,030 |

| Net Pension Liability | (15,975) | (8,964) |

See below the journals required in the entity’s financial statements assuming a deferred tax rate of 10%.

Example 30: Recognising deferred tax

If we take the example above, the net defined benefit pension liability was CU15,975. Therefore the deferred tax asset to be recognised assuming the expected tax rate is 10% is CU1,598 (CU15,975*10%). This is a deferred tax asset as the expense has hit the profit and loss or other comprehensive income but has not yet been allowable for tax. Therefore when the pension contributions are made to reduce this liability they will be allowable for tax purposes. The same approach should be taken in relation to a net defined benefit pension asset i.e. a deferred tax liability should be recognised. Given that a defined benefit asset is only recognised where it is deemed recoverable, if an asset is shown then it is appropriate to recognise a deferred tax liability for this asset.

29.4.2.4.1.8.9 Consolidation adjustments

In the consolidated financial statements sales by one group company to another are eliminated. The creates a timing difference as the legal entity in the group has been taxed on this, however the profit on this sale has been excluded in the consolidated accounts. Therefore a deferred tax asset should be created for the fact that tax has been paid on this profit but it has not been shown in the consolidated financial statements.

Example 31 – Deferred tax on consolidated adjustments – elimination of profit from inventory

During the year Subsidiary B sold goods to Subsidiary A for €100,000. The cost of the sale for Subsidiary A was €50,000. At the year-end Subsidiary B still had €30,000 of this in inventory. Assume a deferred tax rate of 10%. Detailed below are the accounting entries required on consolidation.

| CU | CU | |

| Dr Sales | 100,000 | |

| Cr Cost of Sales (i.e. the cost of sales posted in sub accounts ex item in stock excluding the intra-group profit) | 85,000 | |

| Cr Inventory (€30,000*50% profit margin) | 15,000 |

Being journal to derecognise intercompany sales as consolidated financial statements should only show external sales and purchases and eliminate profit included in inventory. The deferred tax journal required in the consolidated financial statements is:

| CU | CU | |

| Dr Deferred Tax Asset (€15,000*10% assuming a deferred tax rate of 10%) | 1,500 | |

| Cr Deferred Tax in P&L | 1,500 |

Being journal to reflect deferred tax on the above journal (as this is taxed in the entity accounts and included in the group accounts but the income has been reversed out of group accounts there is therefore a timing difference.

29.4.2.4.1.8.10 Investment in associates, joint ventures, subsidiaries in consolidated accounts

Where income and expenses for these entities are included in the consolidated accounts but they will not be taxable in the Parent Company’s books until a distribution is received or until the investments are sold, this may create a timing difference. As a result, a deferred tax asset/liability should be created. In determining the rate to apply, consideration should be given as to the expected method of recovery of the asset i.e. through sale or through dividend receipts. As noted in Section 29.9 of FRS 102, deferred tax cannot be recognised where the parent can control the reversal of the timing difference and it is probable the timing difference will not reverse in the foreseeable future. In reality for Irish subsidiaries there is unlikely to be deferred tax as the entity will not be taxed on receipt of dividend income from the subsidiary as it is not taxable. In reality deferred tax will always need to be recognised on the difference between the carrying amount (which will include the entities allocation of profits/losses since acquisition) and the book value of an investment in an associate where the asset is likely to be realised on sale as the parent cannot control an associate However the capital tax may be avoidable if participation relief applies such that there will be capital tax payable on a sale if the conditions for participation relief are met. This would not be the case if the realisation of the asset is through dividend to be paid where the associate is resident in Ireland as the dividend income would not be taxable i.e. it would then be a permanent difference and no deferred tax recognised.

Example 32: Undistributed profits of a subsidiary

Parent A has a subsidiary Company B. As Parent A controls the dividend policy and it is unlikely to pay a dividend in the foreseeable future, the entity should not recognise deferred tax assuming the asset will be realised from dividends.

29.42.4.1.8.11 Assets partly allowable for tax purposes

There will be instances where assets are purchased which are to be used in the trade, but part of this asset is not allowable for tax purposes because it does not meet the definition of plant timing. On initial recognition the initial timing difference is ignored for deferred tax. See further details at 29.4.2.4.0 In this instance, the depreciation on the non-allowable element is considered a permanent difference and no deferred tax should be provided. In this case the net book value of the non-allowable element is identified and then excluded when comparing the NBV to the TWDV.

Example 33: Assets partly allowable for tax purposes

Company A acquired a car at a cost of CU10,000. Assume under tax rules only CU4,000 is allowable for capital allowances. The asset is depreciated over 10 years and the tax life is also 10 years for the sake of simplicity. The deferred tax to be recognised is:

| NBV at Year End (CU10,000/10yrs*9yrs) | CU9,000 |

| Less NBV of Non-Allowable Element (CU6,000/10yrs*9yrs) | CU5,400 |

| NBV of Allowable Element of Asset | CU3,600 |

| TWDV at Year End | CU3,600 |

| Deferred Tax at Year End | CUNil |

The same could be the case for other items of plant, a car is just used as an example here.

29.4.2.4.1.8.12 Items expensed which are capital in nature (allowable for capital allowances)

Sometimes certain items are expensed which are capital in nature for tax purposes as they are immaterial to capitalise based on an accounting policy. In these instances this is a timing difference i.e. they have been expensed in the accounts in the year but are added back in the tax computation but allowed for capital allowance purposes.

29.4.2.4.1.8.13 Transition adjustments to a new GAAP

Deferred tax will arise on certain transition adjustments. This deferred tax arises as a result of certain items being included in the prior year comparatives which were not taxed previously or a tax deduction was not obtained in the prior year tax computation as the tax computation was performed under old GAAP. Examples of some of the deferred tax adjustments that arise are detailed in the principal transition adjustment sections below at <LINK TO TRNSITION SECTIION FOR SECTION 29>.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 1: Impact of change in tax rate – substantively enacted just after year end.

Example 2: Change in rate during the year.

Example 3: Carry back of losses.

Example 4: Close company surcharge.

Example 5: Close company surcharge – no distributable reserves.

Example 6: Losses forward – recognition of deferred tax.

Example 7: Deferred tax liabilities available to utilise deferred tax assets.

Example 8: Conditions for retaining tax allowances have been met.

Example 9: Dual use manner of recovery.

Example 10: Indexation of base cost – non depreciable asset.

Example 11: Allowable for tax and depreciable.

Example 12: Asset allowable for tax, depreciable and revalued.

Example 14: Transfer of depreciation on revalued amount from profit and loss reserves.

Example 16: Fair value movements and deferred tax impact.

Example 18: Pensions/royalties.

Example 19: Pensions/royalties.

Example 21: Non-puttable ordinary shares and deffered tax.

Example 22: Interest rate swaps – derivatives and deffered tax.

Example 23: Forward foreign currency contract and deffered tax.

Example 27: Defined benefit obligations.

Example 29: Deferred tax on net defined benefit asset/liability.

Example 30: Recognising deferred tax.

Example 31: Deferred tax on consolidated adjustments – elimination of profit from inventory.

Example 32: Undistributed profits of a subsidiary.

Example 33: Assets partly allowable for tax purposes.

Example 34: Deferred tax on business combinations.

Example 36: Dividend received.

Example 37: Offset of current tax assets and liabilities.

Example 38: Offset of current tax assets and liabilities.

Example 39: Offset of current tax assets and liabilities.

Example 40: Offset of deferred tax assets and liabilities.

Example 41: Extract from the accounting policy note and notes to the financial statements.

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]