[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”]

[breadcrumb]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.95″ open=”off” title=”Index”]

Section 27 – Impairment of Assets

Section 27: Impairment of Assets.

27.1.1 Extract from FRS102: Section 27.1 – 27.1A.

27.1.2 OmniPro comment – Objective and scope.

27.2 Impairment of inventories.

27.2.1 Extract from FRS102: Section 27.2 – 27.4.

27.2.2 OmniPro comment – Impairment of Inventories.

27.3 Impairment of assets other than inventories.

27.3.1 Extract from FRS102: Section 27.5 – 27.6.

27.4 Impairment – assessing if an impairment is required.

27.4.1 Extract from FRS102: Section 27.7 – 27.8.

27.4.2.1 Assessing if an impairment is required.

27.5.1 Extract from FRS102: Section 27.9 – 27.10.

27.5.2 OmniPro comment – Indicators of Impairment

27.6 Measuring recoverable amount

27.6.1 Extract from FRS102: Section 27.11 – 27.13.

27.6.2 OmniPro comment – Measuring recoverable amount

27.7 Fair value less costs to sell

27.7.1 Extract from FRS102: Section 27.14 – 27.14A.

27.7.2.1 Fair value less cost to sell – active market

27.7.2.2 Fair value less cost to sell – no active market – valuation model

27.7.2.3 Discount rate for fair value less cost to sell

27.8.1 Extract from FRS102: Section 27.15 – 27.20.

27.8.2.2 Estimating the future pre-tax cash flows.

27.8.2.4 Steps in calculating Value in Use.

27.8.2.5 Value in use – discount rate.

27.8.2.6 Value in use – terminal value.

27.9 Assets held for service potential

27.9.1 Extract from FRS102: Section 27.20A.

27.9.2 OmniPro comment – Asset held for service potential

27.10 Recognising and measuring an impairment loss for a cash-generating unit

27.10.1 Extract from FRS102: Section 27.21 – 27.23.

27.10.2.1 Allocation of the improvement loss in a CGU.

27.10.2.2 Restoration on reduction of assets as a result of impairment

27.11 Additional requirements for impairment of goodwill

27.11.2.1 – Impairment of Goodwill

27.12 Reversal of an impairment loss.

27.12.1 Extract from FRS102: Section 27.28 – 27.30.

27.12.2.1 Impairment reversals generally.

27.13 Reversal when recoverable amount was estimated for a cash-generating unit

27.13.1 Extract from FRS102: Section 27.31.

27.13.2 OmniPro comment – Reversal of impairment when recoverable amount based on CGU

27.14.1 Extract from FRS102: Section 27.32 – 27.33A.

27.14.2 OmniPro comment – Disclosures.

27.14.2.1 Tangible fixed assets accounting policy disclosure.

27.14.2.2 Extract from notes to the financial statements.

27.14.2.2.1 Exceptional item – impairment charge.

27.14.2.2.2Tangible fixed assets.

27.14.2.2.3 Extract from profit and loss where impairment is shown as an exceptional item.

27.14.2.2.4 Extract from notes to the financial statements

27.14.2.2.5 Extract from notes where impairment is not deemed exceptional

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.17.6″]

27.3 Impairment of assets other than inventories

27.3.1 Extract from FRS102: Section 27.5 – 27.6

27.5 If, and only if, the recoverable amount of an asset is less than its carrying amount, the entity shall reduce the carrying amount of the asset to its recoverable amount. That reduction is an impairment loss. Paragraphs 27.11 to 27.20A provide guidance on measuring recoverable amount.

27.6 An entity shall recognise an impairment loss immediately in profit or loss, unless the asset is carried at a revalued amount in accordance with another section of this FRS (for example, in accordance with the revaluation model in Section 17 Property, Plant and Equipment). Any impairment loss of a revalued asset shall be treated as a revaluation decrease in accordance with that other section.

27.3.2 OmniPro comment – Impairment of assets other than inventory – assessing if an impairment is required

As detailed in Section 17 Property, Plant and Equipment (see 17.2.5.2.2 of Section 17), any impairment identified on a revalued asset is first set against the revaluation reserve and then to the profit and loss account.

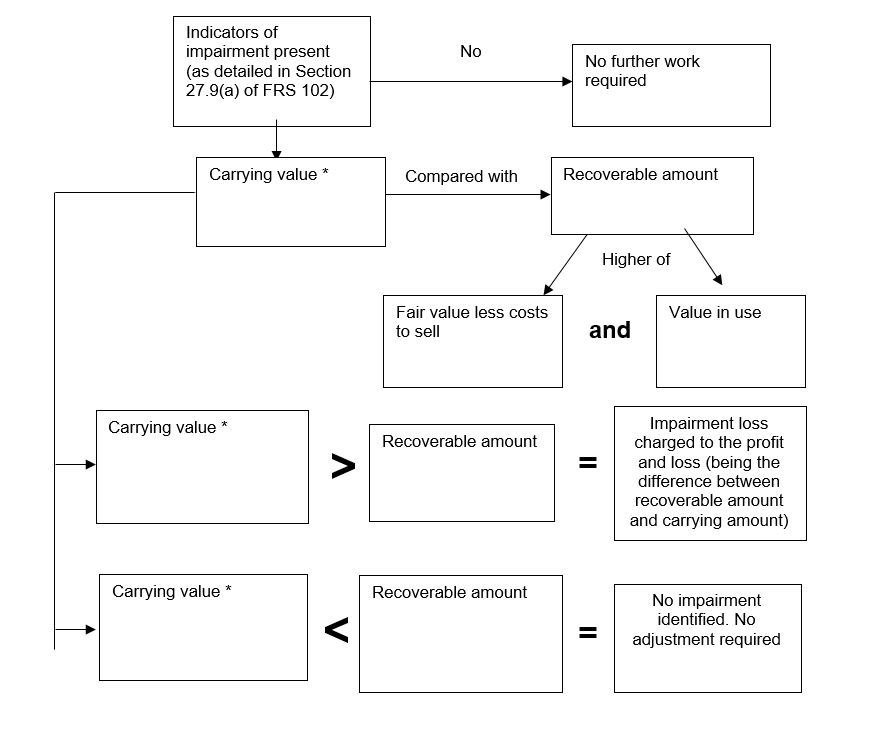

See diagrammatic representation of the analysis to be performed when assessing if an impairment is present. The requirements are detailed in Section 27.7 and 27.8 of FRS 102

Diagnostic assessment if Impairment is required

*Note the carrying value can be the value of the individual assets where cash flows can be identified from the asset or it can be a carrying value of a cash generating unit where cash flows cannot be identified as specific to an asset. The starting point is an individual asset, then one should move to a CGU. As can be seen from the above, it may not always be necessary to calculate the fair value less costs to sell and the value in use. If one of the measures give a value which is greater than the carrying value this indicates no impairment is required so there is no need for further work to be performed to assess the other measure.

Recoverable amount is defined in Appendix I of FRS 102 as ‘the higher of an asset’s (or cash generating unit’s) fair value less costs to sell and its value in use.

Fair value less cost to sell is defined as ‘the amount obtainable from the sale of an asset or CGU in an arm’s length transaction between knowledgeable willing parties, less the costs of disposal.

Value in use is the present value of the future cash flows expected to be derived from an asset or cash-generating unit. As can be seen from the above, it may not always be necessary to calculate the value in use.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples:

Example 1: Lowest available CGU.

Example 2: Lowest available CGU.

Example 3: A decline in the asset’s market value.

Example 4: Significant adverse changes that have taken/will take place in the market

Example 5: Change in assets use.

Example 6: Introduction of new competitor

Example 7: Impairment indicators – decision to close.

Example 8: Performance of an asset is worse than expected.

Example 9: Investment in subsidiary.

Example 10: Value in use differs from fair value less costs to sell

Example 11: Fair value less costs to sell

Example 12: Determining cash flow to include.

Example 14: Impairment loss for a CGU with goodwill

Example 15: Restriction of reduction of assets as a result of an impairment

Example 16: Impairment loss on a CGU with goodwill and non-controlling interests

Example 17: Reversal of impairment on an individual asset

Example 18: Reversal of cash generating unit

Example 19: extract from an accounting policy note and disclosure requirements.

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]