[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.106″ open=”off” title=”Index”]

Section 11: Basic Financial Instruments.

11.2 Accounting policy choice.

11.2.1 Extract from FRS 102 Section 11.2-11.2A.

11.2.2 OmniPro comment – Accounting Policy Choice.

11.3 Scope of the Section 11 and Section 12.

11.3.1 Extract from FRS 102 Section 11.3, 11.5, 11.7 and Glossary to FRS 102.

11.3.2 OmniPro comment – Scope of Section 11.

11.3.2.1 Financial assets and liabilities not within the remit of Section 11 and 12.

11.4 Classification of financial instruments.

11.4.1 Extract from FRS 102 Section 11.6 and 11.8.

11.4.2 OmniPro comment – classification of financial instruments and scope (within Section 11 or 12)

11.4.2.2 – Investment in Shares.

11.5 Conditions for debt instruments to meet the definition of a basic financial instrument

11.5.1 Extract from FRS 102 Section 11.9.

11.5.2 OmniPro comment – basic financial instruments.

11.6 Initial and subsequent measurement of debt instruments.

11.6.1 Extract from FRS 102 Section 11.12-11.20.

11.6.1.2 Subsequent measurement

11.6.1.3 Amortised cost and effective interest method.

11.6.2.2 Short-term receivables/payable within one year

11.6.2.3 Transaction costs – definition/treatment

11.6.2.4 Effective interest rate calculation and amortised cost

11.6.2.4.1 Effective interest rate

11.6.2.4.3 Put or call options when calculating effective interest rate

11.6.2.4.4 Diagram 1 Rules for Accounting for basic financial instruments

11.6.2.4.5 – Financing Arrangement

11.6.2.4.6 Steps in determining the effective interest rate

11.6.2.4.7 Changes in cash flow estimates (amortised cost model)

11.6.2.4.8 Non market loans- inter-company loan / director’s loans

11.6.2.4.8.1 Determining the market rate of interest

11.6.2.4.8.2: Analysis of debt and credits on initial recognition of loans – financing arrangements.

11.6.2.4.9 Sales and purchases made under unusual credit terms – Debtors/creditors

11.6.2.4.11 Loans repayable on demand

11.6.2.4.12 Loan repayable on demand but with notice of 1 year and 1 day

11.6.2.4.15 Variable interest rate over the life of the loan

11.6.2.4.16 Issues surrounding directors or intra-group loans

11.6.2.4.16.1 Factors that indicate a related party loan is not at market rates.

11.7.1 Extract from FRS 102 Section 11.27-11.32.

11.7.2.1.2 Fair value hierarchy

11.8 Impairments of financial assets held at cost or amortised cost

11.8.1 Extract from FRS 102 Section 11.21-11.26.

11.8.2.1 Indicators of Impairment

11.8.2.2 Individual and group impairments.

11.8.2.3 Impairment debt instruments.

11.8.2.4 Reversal of Impairments.

11.8.2.5 Impairment of financial assets carried at cost

11.9 Derecognition of a Financial Asset

11.9.1 Extract from FRS 102 Section 11.33-11.35.

11.9.2 OmniPro comment – Decrecognition of Financial Assets.

11.10 Derecognition of financial liabilities.

11.10.1 Extract from FRS 102 Section 11.36-11.38.

11.6.2.4.5 Derecognition rules – overview

11.10.2.2 Derecognition of Financial Liability.

11.11.1 Extract from FRS 102 Section 11.38A.

11.11.2 OmniPro comment – Presentation – set off

11.12.1 Extract from FRS 102 Section 11.39-11.48A.

11.12.2.1 Disclosure requirements.

11.12.2.2 Sample Disclosure requirements.

11.12.2.2.1 Extract from accounting policy notes

11.12.2.2.2 Extract of notes to the financial statements – Financial instruments note disclosures

11.12.2.2.3 Extract of notes to the financial statements – interest disclosures.

11.12.2.2.3.1 Note: Interest receivable and similar income.

11.12.2.2.3.2 Note: Interest payable and similar expenses.

11.12.2.2.4 – Debtors Disclosures

11.12.2.2.5 – Creditors disclosures

11.12.2.2.7 Statement of Comprehensive Income

11.12.2.2.8 – Statement of Change in Equity

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.0.98″]

11.8 Impairments of financial assets held at cost or amortised cost

11.8.1 Extract from FRS 102 Section 11.21-11.26

Recognition

11.21 At the end of each reporting period, an entity shall assess whether there is objective evidence of impairment of any financial assets that are measured at cost or amortised cost. If there is objective evidence of impairment, the entity shall recognise an impairment loss in profit or loss immediately.

11.22 Objective evidence that a financial asset or group of assets is impaired includes observable data that come to the attention of the holder of the asset about the following loss events:

(a) significant financial difficulty of the issuer or obligor;

(b) a breach of contract, such as a default or delinquency in interest or principal payments;

(c) the creditor, for economic or legal reasons relating to the debtor’s financial difficulty, granting to the debtor a concession that the creditor would not otherwise consider;

(d) it has become probable that the debtor will enter bankruptcy or other financial reorganisation; and

(e) observable data indicating that there has been a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, even though the decrease cannot yet be identified with the individual financial assets in the group, such as adverse national or local economic conditions or adverse changes in industry conditions.

11.23 Other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates.

11.24 An entity shall assess the following financial assets individually for impairment:

(a) all equity instruments regardless of significance; and

(b) other financial assets that are individually significant.

An entity shall assess other financial assets for impairment either individually or grouped on the basis of similar credit risk characteristics.

Measurement

11.25 An entity shall measure an impairment loss on the following instruments measured at cost or amortised cost as follows:

(a) For an instrument measured at amortised cost in accordance with paragraph 11.14(a), the impairment loss is the difference between the asset’s carrying amount and the present value of estimated cash flows discounted at the asset’s original effective interest rate. If such a financial instrument has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract.

(b) For an instrument measured at cost less impairment in accordance with paragraph 11.14(c) and (d)(ii) the impairment loss is the difference between the asset’s carrying amount and the best estimate (which will necessarily be an approximation) of the amount (which might be zero) that the entity would receive for the asset if it were to be sold at the reporting date.

Reversal

11.26 If, in a subsequent period, the amount of an impairment loss decreases and the Decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtors credit rating), the entity shall reverse the previously recognised impairment loss either directly or by adjusting an allowance account. The reversal shall not result in the carrying amount of the financial asset (net of any allowance account) that exceeds what the carrying amount would have been had the impairment not previously been recognised. The entity shall recognise the amount of the reversal in the profit and loss account immediately.

11.8.2 OmniPro comment

11.8.2.1 Indicators of Impairment

Impairment of financial assets is only relevant to assets measured at amortised cost or cost. For financial assets which are held at fair value, the diminution is recognised year on year as it is carried at fair value. At the end of each reporting period an entity is required to assess whether there are indicators/objective evidence of impairment of financial assets and if there is an impairment should be booked. Detailed in Section 11.22 and 11.23 of FRS 102 above are the detailed impairment indicators. They are summarised as follows:

(a) significant financial difficulty of the issuer or obligor;

(b) a breach of contract, such as a default or delinquency in interest or principal payments;

(c) the creditor, for economic or legal reasons relating to the debtor’s financial difficulty, granting to the debtor a concession that the creditor would not otherwise consider;

(d) it has become probable that the debtor will enter bankruptcy or other financial reorganisation; and

(e) observable data indicating that there has been a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, even though the decrease cannot yet be identified with the individual financial assets in the group, such as adverse national or local economic conditions or adverse changes in industry conditions;

(f) other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates;

(h) the solvency, business and financial risk exposures of the debtor;

(i) levels of, and trends in, delinquencies for similar financial assets;

(j) A downgrade in the entity’s credit rating.

When an impairment indicator is present an impairment is required where the recoverable amount is less than carrying amount at a period end. This applies even for a temporary impairment i.e. a held to maturity model cannot be utilised. (e.g. if a bond is for 5 years and at period end the market value is less than carrying amount then an impairment is booked regardless of the fact that will get the per amount at the end of the bonds life.

11.8.2.2 Individual and group impairments

The standard requires that all ordinary and preference shares (equity instruments) are assessed for impairment individually. Other financial assets can be grouped where it is determined appropriately and can usually be done on a collective basis where it is performed on the basis of credit risks. (i.e. they have similar credit risk characteristics).

11.8.2.3 Impairment debt instruments

For debt instruments which have a fixed rate which are measured at amortised cost, the difference between the asset’s carrying amount and the present value of estimated cash flows discounted at the asset’s original effective interest rate when it was initially recognised. Is the amount of the impairment that is required to be booked (Section 11.25 (a) FRS 102).

For variable debt instruments, the discount rate to be used is the current effective interest rate determined under the contract. For example, if the debt instrument was issued at LIBOR + 50 basis points. The LIBOR rate at initial recognition was 3%, but the LIBOR rate at the date of the impairment indicator is 5%. The 5% is used as part of the impairment review as the LIBOR was stated in the contract.

Where an impairment is identified a provision can be booked against the impairment or the amount can be written off.

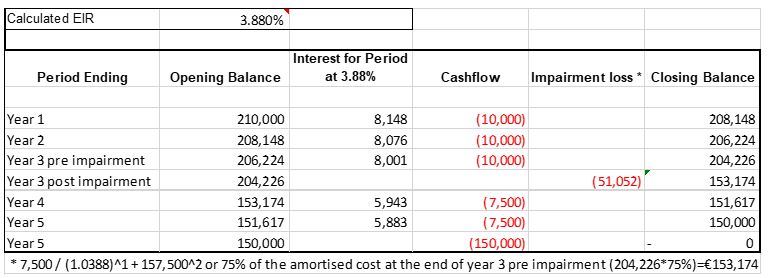

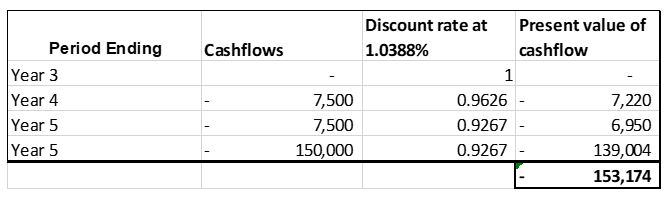

Example 20: Impairment of debt instruments

Company A issued a loan to a related company for CU200,000 and incurred costs of CU10,000 at the start of year 1 for 5 years. Interest at a fixed rate of 5% was charged (i.e. CU10,000 per annum) which was deemed to be the market rate of the loan at that date. At the end of year 3 the related company’s financial performance deteriorated and shows signs that the full amount will not be recoverable. Company A estimates that it will only receive 75% of the interest (i.e. CU150,000*5%=CU7,500) and 75% of the capital (i.e. CU200,000*75%=CU150,000). Therefore, an impairment loss is required to be booked. The effective rate on taking out the loan was 3.88% which was calculated using a mathematical model in Excel.

NOTE: if in the above example the entity determined there to be doubt about the recoverability of the full asset an impairment of CU204,226 would be booked.

11.8.2.4 Reversal of Impairments

If the impairment review reverses in a prior period, then the impairment can be reversed to the P&L. Any reversal of a prior year impairment cannot reinstate the amortised cost above that what it would have been if no impairment was required. (Section 11.26 FRS 102) See an example of the application of this guidance at example 20a at 11.8.2.5 It can only be reversed if the thing that caused the impairment reverses.

This applies to ordinary or preference shares which are not publicly traded and whose fair value cannot be reliably measured or investment in bonds which are considered basic etc. Where there is objective evidence that a loss has occurred then the amount of the impairment is the difference between the asset’s carrying amount and the best estimate of the amount the entity would receive on a sale at that reporting date.

When an impairment indicator is present an impairment is required where the recoverable amount is less than carrying amount at a period end. This applies even for temporary impairment i.e. a held to maturity model cannot be utilised. (e.g. if a bond is for 5 years and at period end the market value is less than carrying amount then an impairment is booked regardless of the fact that will get the per amount at the end of the bonds life.

11.8.2.5 Impairment of financial assets carried at cost

This applies to ordinary or preference shares which are not publicly traded and whose fair value cannot be reliably measured or investment in bonds which are considered basic etc. Where there is objective evidence that a loss has occurred then the amount of the impairment is the difference between the asset’s carrying amount and the best estimate of the amount the entity would receive on a sale at that reporting date.

When an impairment indicator is present an impairment is required where the recoverable amount is less than carrying amount at a period end. This applies even for temporary impairment i.e. a held to maturity model cannot be utilised. (e.g. if a bond is for 5 years and at period end the market value is less than carrying amount then an impairment is booked regardless of the fact that will get the per amount at the end of the bonds life.

This applies to ordinary or preference shares which are not publicly traded and whose fair value cannot be reliably measured or investment in bonds which are considered basic etc. Where there is objective evidence that a loss has occurred then the amount of the impairment is the difference between the asset’s carrying amount and the best estimate of the amount the entity would receive on a sale at that reporting date.

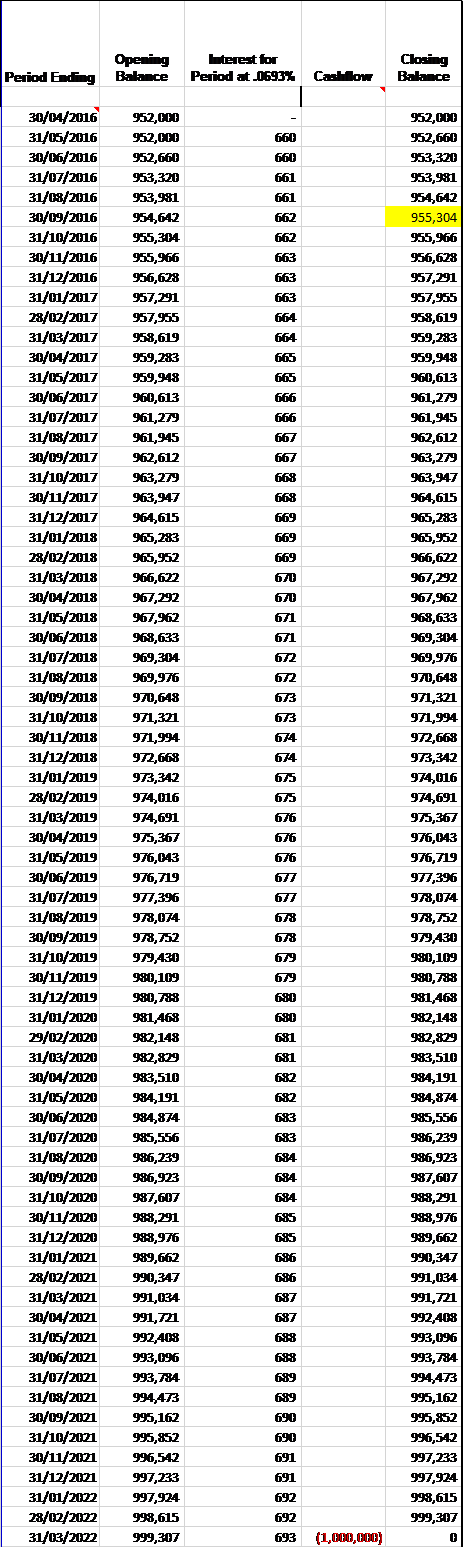

Example 20a: Bonds with an impairment

Company A acquired a capital guaranteed government bond for CU950,000 on 30 April 2016 and matures on 16 March 2021. The bond was for CU1 million and had a coupon rate of 5% with commission costs of CU2,000.

The discount should be amortised into the P&L over the life of the bond on the effective interest rate basis and held at amortised cost. The effective interest rate is calculated by mathematical formula. It is a rate of .0693% per month as per below.

The journals required to account for this in the year ended 31 December 2016 are:

Journal 1:

| CU | CU | |

| Dr investment-government bond | 5,291 | |

| Cr investment income in P&L | 5,291 |

Being journal to unwind the discount on the bond up to 31 December 2016 so as to come to CU 957,291

Note when the coupon on the government bond is paid in the year, you will continue to recognise the full 5% in income i.e.

Journal 2:

| CU | CU | |

| Dr bank

(CU1,000,000 * 5%) |

50,000 | |

| Cr investment income in P&L | 50,000 |

At each period end the Company must review the bond for indicators of impairment which are given in Section 11.22 of FRS 102. Where these are present they should be written down to the market value of bond/recoverable amount in line with Section 11.25 of FRS 102.

If come the following year the impairment has been reversed the previous impairment booked should be reversed back up to the amount it would have been stated at as if no impairment were carried out (Section 11.25 (a) FRS 102).

If we assume at 31 December 2016 or prior to the sign off of the accounts, the market value of the bond was CU940,000, then an impairment of CU17,291 (CU957,291-CU940,000) should be booked (as per Section 11.25 of FRS 102).

The Journal required would be:

| CU | CU | |

| Dr loss on investment in P&L | 17,291 | |

| Cr Government bond | 17,291 |

Being journal to reflect the temporary impairment of the bond

From that date on you need to calculate the effective interest rate that will bring the CU940,000 to CU1,000,000 by the end of the bonds life (Section 11.14 of FRS 102). Effective interest rate calculated at 0.0983% through the use of a mathematical formula. See the amount to be released per month in the calculation below:

If we assume that at the 31 December 2017 the impairment had reversed and the market value was €970,000. Then a journal would be required to reverse the previous impairment as follows

| CU | CU | |

| Dr investments – government bond (balance if no impairment had of been booked = CU965,283 as per table 1 above less carrying amount at 31 Dec 2017 of CU951,144 as per table 2 above) | 14,139 | |

| Cr gain/loss on investments in P&L | 14,139 |

Being journal to reflect reversal of previous impairment (note per Section 11.26 of FRS 102 you can only reverse the impairment up to what it would have been if no impairment had accrued where it is held at amortised cost.)

Note: If the bond was purchased at a premium (i.e. purchased the bond for CU1,050,000) then the journals in journal 1 should be reversed so as to release the premium as a debit against income in the P&L.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 1: Investment in shares.

Example 2: Investment in shares – 15%.

Example 3: variable and fixed interest payments.

Example 5: Fixed and variable interest payments.

Example 6: Fixed rate loan for a set period and then a reversion to the banks variable rate.

Example 8: Loan/bond which is convertible into the borrower’s equity.

Example 9: Loan issued which is linked to a general inflation index.

Example 10: Variation in return.

Example 11: Prepayment options.

Example 12: Loan extension option.

Example 12a: Unguaranteed Capital

Example 12b: Collective investment funds.

Example 13: loan at market rates with transaction costs.

Example 13a: Change in estimate.

Example 14: Intercompany loan from a parent company.

Example 15: Loan provided to the company by a director

Example 16a: Intercompany loan from a related party or a fellow subsidiary.

Example 16b: Loan from subsidiary to the parent company.

Example 16c: Sale with unusual credit terms.

Example 16d: Purchase with unusual credit terms.

Example 17a: Loans repayable on demand..

Example 17b: Loan repayable on demand but with notice of 1 year and 1 day.

Example 18: Bonds – discount/premium.

Example 20: Impairment of debt instruments.

Example 20a: Bonds with an impairment

Example 21: Asset recognised due to settlement

Example 22: Sale of debtors with recourse.

Example 23: Sale of debtors without recourse.

Example 24: Transfer of assets at fair value subject to a call option.

Example 25: Substantial modification of a loan.

Example 26: Sample disclosure requirements

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]