[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”]

[breadcrumb]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.106″ open=”off” title=”Index”]

Section 11: Basic Financial Instruments.

11.2 Accounting policy choice.

11.2.1 Extract from FRS 102 Section 11.2-11.2A.

11.2.2 OmniPro comment – Accounting Policy Choice.

11.3 Scope of the Section 11 and Section 12.

11.3.1 Extract from FRS 102 Section 11.3, 11.5, 11.7 and Glossary to FRS 102.

11.3.2 OmniPro comment – Scope of Section 11.

11.3.2.1 Financial assets and liabilities not within the remit of Section 11 and 12.

11.4 Classification of financial instruments.

11.4.1 Extract from FRS 102 Section 11.6 and 11.8.

11.4.2 OmniPro comment – classification of financial instruments and scope (within Section 11 or 12)

11.4.2.2 – Investment in Shares.

11.5 Conditions for debt instruments to meet the definition of a basic financial instrument

11.5.1 Extract from FRS 102 Section 11.9.

11.5.2 OmniPro comment – basic financial instruments.

11.6 Initial and subsequent measurement of debt instruments.

11.6.1 Extract from FRS 102 Section 11.12-11.20.

11.6.1.2 Subsequent measurement

11.6.1.3 Amortised cost and effective interest method.

11.6.2.2 Short-term receivables/payable within one year

11.6.2.3 Transaction costs – definition/treatment

11.6.2.4 Effective interest rate calculation and amortised cost

11.6.2.4.1 Effective interest rate

11.6.2.4.3 Put or call options when calculating effective interest rate

11.6.2.4.4 Diagram 1 Rules for Accounting for basic financial instruments

11.6.2.4.5 – Financing Arrangement

11.6.2.4.6 Steps in determining the effective interest rate

11.6.2.4.7 Changes in cash flow estimates (amortised cost model)

11.6.2.4.8 Non market loans- inter-company loan / director’s loans

11.6.2.4.8.1 Determining the market rate of interest

11.6.2.4.8.2: Analysis of debt and credits on initial recognition of loans – financing arrangements.

11.6.2.4.9 Sales and purchases made under unusual credit terms – Debtors/creditors

11.6.2.4.11 Loans repayable on demand

11.6.2.4.12 Loan repayable on demand but with notice of 1 year and 1 day

11.6.2.4.15 Variable interest rate over the life of the loan

11.6.2.4.16 Issues surrounding directors or intra-group loans

11.6.2.4.16.1 Factors that indicate a related party loan is not at market rates.

11.7.1 Extract from FRS 102 Section 11.27-11.32.

11.7.2.1.2 Fair value hierarchy

11.8 Impairments of financial assets held at cost or amortised cost

11.8.1 Extract from FRS 102 Section 11.21-11.26.

11.8.2.1 Indicators of Impairment

11.8.2.2 Individual and group impairments.

11.8.2.3 Impairment debt instruments.

11.8.2.4 Reversal of Impairments.

11.8.2.5 Impairment of financial assets carried at cost

11.9 Derecognition of a Financial Asset

11.9.1 Extract from FRS 102 Section 11.33-11.35.

11.9.2 OmniPro comment – Decrecognition of Financial Assets.

11.10 Derecognition of financial liabilities.

11.10.1 Extract from FRS 102 Section 11.36-11.38.

11.6.2.4.5 Derecognition rules – overview

11.10.2.2 Derecognition of Financial Liability.

11.11.1 Extract from FRS 102 Section 11.38A.

11.11.2 OmniPro comment – Presentation – set off

11.12.1 Extract from FRS 102 Section 11.39-11.48A.

11.12.2.1 Disclosure requirements.

11.12.2.2 Sample Disclosure requirements.

11.12.2.2.1 Extract from accounting policy notes

11.12.2.2.2 Extract of notes to the financial statements – Financial instruments note disclosures

11.12.2.2.3 Extract of notes to the financial statements – interest disclosures.

11.12.2.2.3.1 Note: Interest receivable and similar income.

11.12.2.2.3.2 Note: Interest payable and similar expenses.

11.12.2.2.4 – Debtors Disclosures

11.12.2.2.5 – Creditors disclosures

11.12.2.2.7 Statement of Comprehensive Income

11.12.2.2.8 – Statement of Change in Equity

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.17.6″]

The below extracts and guidance is applicable for periods beginning before 1 January 2019 and are based on the September 2015 version of FRS 102. For periods beginning on or after 1 January 2019, the March 2018 version of FRS 102 applies which incorporates the changes made by the Triennial review of FRS 102. Note the March 2018 version of FRS 102 can be voluntarily applies for periods beginning before 1 January 2019. For the extracts from the March 2018 version of FRS 102 and the related guidance please click on the following link. For details of a summary of the main changes as a result of the triennial review please see the following link.

11.6 Initial and subsequent measurement of debt instruments

11.6.1 Extract from FRS 102 Section 11.12-11.20

11.6.1.1 Initial Recognition

11.12 An entity shall recognise a financial asset or a financial liability only when the entity becomes a party to the contractual provisions of the instrument.

11.13 When a financial asset or financial liability is recognised initially, an entity shall measure it at the transaction price (including transaction costs except in the initial measurement of financial assets and liabilities that are measured at fair value through profit or loss) unless the arrangement constitutes, in effect, a financing transaction. A financing transaction may take place in connection with the sale of goods or services, for example, if payment is deferred beyond normal business terms or is financed at a rate of interest that is not a market rate. If the arrangement constitutes a financing transaction, the entity shall measure the financial asset or financial liability at the present value of the future payments discounted at a market rate of interest for a similar debt instrument.

Examples – financial assets

- For a long-term loan at a market rate of interest made to another entity, a receivable is recognised at the amount of the cash advanced to that entity plus transaction costs incurred by the entity (see the example following paragraph 11.20).

- For goods sold to a customer on short-term credit, a receivable is recognised at the undiscounted amount of cash receivable from that entity, which is normally the invoice price.

- For an item sold to a customer on two-years interest-free credit, a receivable is recognised at the current cash sale price for that item (in financing transactions conducted on an arm’s length basis the cash sales price would normally approximate to the present value). If the current cash sale price is not known, it may be estimated as the present value of the cash receivable discounted using the prevailing market rate(s) of interest for a similar receivable.

- For a cash purchase of another entity’s ordinary shares, the investment is recognised at the amount of cash paid to acquire the shares.

Examples – financial liabilities

- For a loan received from a bank at a market rate of interest, a payable is recognised initially at the amount of the cash received from the bank less separately incurred transaction costs.

- For goods purchased from a supplier on short-term credit, a payable is recognised at the undiscounted amount owed to the supplier, which is normally the invoice price.

11.6.1.2 Subsequent measurement

11.14 At the end of each reporting period, an entity shall measure financial instruments as follows, without any deduction for transaction costs the entity may incur on sale or other disposal:

(a) Debt instruments that meet the conditions in paragraph 11.8(b) shall be measured at amortised cost using the effective interest method. Paragraphs 11.15 to 11.20 provide guidance on determining amortised cost using the effective interest method. Debt instruments that are payable or receivable within one year shall be measured at the undiscounted amount of the cash or other consideration expected to be paid or received (ie net of impairment—see paragraphs 11.21 to 11.26) unless the arrangement constitutes, in effect, a financing transaction (see paragraph 11.13). If the arrangement constitutes a financing transaction, the entity shall measure the debt instrument at the present value of the future payments discounted at a market rate of interest for a similar debt instrument.

(b) Debt instruments that meet the conditions in paragraph 11.8(b) and commitments to receive a loan and to make a loan to another entity that meet the conditions in paragraph 11.8(c) may upon their initial recognition be designated by the entity as at fair value through profit or loss (paragraphs 11.27 to 11.32 provide guidance on fair value) provided doing so results in more relevant information, because either:

(i) it eliminates or significantly reduces a measurement or recognition inconsistency (sometimes referred to as ‘an accounting mismatch’) that would otherwise arise from measuring assets or debt instruments or recognising the gains and losses on them on different bases; or

(ii) a group of debt instruments or financial assets and debt instruments is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information about the group is provided internally on that basis to the entity’s key management personnel (as defined in Section 33 Related Party Disclosures, paragraph 33.6), for example members of the entity’s board of directors and its chief executive officer.

(c) Commitments to receive a loan and to make a loan to another entity that meet the conditions in paragraph 11.8(c) shall be measured at cost (which sometimes is nil) less impairment.

(d) Investments in non-convertible preference shares and non-puttable ordinary shares or preference shares shall be measured as follows (paragraphs 11.27 to 11.32 provide guidance on fair value):

(i) if the shares are publicly traded or their fair value can otherwise be measured reliably, the investment shall be measured at fair value with changes in fair value recognised in profit or loss; and

(ii) all other such investments shall be measured at cost less impairment.

Impairment or uncollectability must be assessed for financial assets in (a), (c) and (d)(ii) above. Paragraphs 11.21 to 11.26 provide guidance.

11.6.1.3 Amortised cost and effective interest method

11.15 The amortised cost of a financial asset or financial liability at each reporting date is the net of the following amounts:

(a) the amount at which the financial asset or financial liability is measured at initial recognition;

(b) minus any repayments of the principal;

(c) plus or minus the cumulative amortisation using the effective interest method of any difference between the amount at initial recognition and the maturity amount;

(d) minus, in the case of a financial asset, any reduction (directly or through the use of an allowance account) for impairment or uncollectability.

Financial assets and financial liabilities that have no stated interest rate (and do not constitute a financing transaction) and are classified as payable or receivable within one year are initially measured at an undiscounted amount in accordance with paragraph 11.14(a). Therefore, (c) above does not apply to them.

11.16 The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability (or a group of financial assets or financial liabilities) and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate, a shorter period, to the carrying amount of the financial asset or financial liability. The effective interest rate is determined on the basis of the carrying amount of the financial asset or liability at initial recognition. Under the effective interest method:

(a) the amortised cost of a financial asset (liability) is the present value of future cash receipts (payments) discounted at the effective interest rate; and

(b) the interest expense (income) in a period equals the carrying amount of the financial liability (asset) at the beginning of a period multiplied by the effective interest rate for the period.

11.17 When calculating the effective interest rate, an entity shall estimate cash flows considering all contractual terms of the financial instrument (e.g. prepayment, call and similar options) and known credit losses that have been incurred, but it shall not consider possible future credit losses not yet incurred.

11.18 When calculating the effective interest rate, an entity shall amortise any related fees, finance charges paid or received (such as ‘points’), transaction costs and other premiums or discounts over the expected life of the instrument, except as follows. The entity shall use a shorter period if that is the period to which the fees, finance charges paid or received, transaction costs, premiums or discounts relate. This will be the case when the variable to which the fees, finance charges paid or received, transaction costs, premiums or discounts relate is repriced to market rates before the expected maturity of the instrument. In such a case, the appropriate amortisation period is the period to the next such repricing date.

11.19 For variable rate financial assets and variable rate financial liabilities, periodic re-estimation of cash flows to reflect changes in market rates of interest alters the effective interest rate. If a variable rate financial asset or variable rate financial liability is recognised initially at an amount equal to the principal receivable or payable at maturity, re-estimating the future interest payments normally has no significant effect on the carrying amount of the asset or liability.

11.20 If an entity revises its estimates of payments or receipts, the entity shall adjust the carrying amount of the financial asset or financial liability (or group of financial instruments) to reflect actual and revised estimated cash flows. The entity shall recalculate the carrying amount by computing the present value of estimated future cash flows at the financial instrument’s original effective interest rate. The entity shall recognise the adjustment as income or expense in profit or loss at the date of the revision.

11.6.2 OmniPro comment

11.6.2.1 Initial recognition

A basic financial instrument is recognised at the transaction price including transaction costs with the exception of financial asset and liabilities which are required to be fair valued i.e. investments in shares where ownership is less than 20% (or where significant influence as defined in Section 14 of FRS 102 is not obtained) or where debt instruments meet the definition in 11.14 (b) of FRS 102.

11.6.2.2 Short-term receivables/payable within one year

Section 11.14 (a) of FRS 102 allows short term receivables or payables i.e. repayable/payable within one year to be carried at the undiscounted rate which is normally the invoice price. However where a financing arrangement exists it may need to be carried based on present value depending on materiality. See 16.6.2.4.5 for accounting for debt instrument rate where a financing arrangement exists and how to identify such an arrangement. See Diagram for Summary of Requirements under Section 11.12 to 11.20 of FRS 102 at 11.6.2.4.4

11.6.2.3 Transaction costs – definition/treatment

Transaction costs are incidental costs directly attributable to the acquisition, issue or disposal of the financial asset or liability. They are usually:

- the arrangement fees,

- commitment fees, or

- facility fees.

These costs are added to the amount originally received where it is an asset or deducted from a liability and included in the calculation of amortised cost using the effective interest rate method (see 11.6.2.4.2). The transactions costs are usually released over the life of the instrument unless there is a market repricing element in the contract in which case the transaction price is released up to the date of market repricing. The only exception is where the financial asset or liability is calculated at fair value in which case they are expensed as incurred (i.e. an investment in non-puttable ordinary or preference shares or where a debt instrument meets the definition of 11.14 (b) where measuring the debt instrument at amortised cost creates a measurement inconsistency.

Transaction costs do not include:

- debt premium or discounts;

- finance costs; or

- internal administration costs.

11.6.2.4 Effective interest rate calculation and amortised cost

11.6.2.4.1 Effective interest rate

The effective interest rate is the rate that brings the interest carrying amount including transaction costs back to the payable/repayable balance of the end of the instrument’s life. It is a method of cal-culating the amortised cost of a financial asset or liability and of allocating the interest income or expense over the life of the instrument See further details at 11.6.2.4.2 See diagram on next page for the way in which a basic financial instrument should be accounted for on initial and subsequent measurement.

11.6.2.4.2 Amortised cost

The amortised cost is the amount at which the financial asset/liablity is measured at initial recognition minus principal repayments, plus or minus the cumulative amortisation using the effective interest rate basis of any difference between the initial amount and the maturity amount minus any reduction (directly or through the use of an allowance account), and minus any reductions (directly or through the use of an allowance account) for impairment or uncollectability.

See Example 13 at 11.6.2.4.5 for illustration of this method. In addition see examples 14 to 16 at 11.6.2.4.8 where the effective interest rate rules and amortised cost basis is illustrated for loans to and from group companies/directors.

See Example 16c and 16d detailed in 11.6.2.4.9 which illustrates the effective interest rate and amortised cost model for sales and purchases made under unusual credit terms (debtors/creditors). See 11.6.2.4.14 for illustration of this method for bonds. See illustration of loans to employees at 11.6.2.4.10

11.6.2.4.3 Put or call options when calculating effective interest rate

When calculating the effective interest rate, consideration needs to be given to any put or call options, and at each reporting date a determination as to whether it is likely any party will take action on the put and call options so that the life over the financial instrument can be determined. If initially the calcula-tions were completed based on the option not been triggered which then it subsequently does, then the financial asset/liability would have to be adjusted to reflect the actual and revised estimated cash flows. The adjustment is recognised prospectively as income or expenses at the date of the revision.

11.6.2.4.4 Diagram 1 Rules for Accounting for basic financial instruments

11.6.2.4.5 – Financing Arrangement

Where a financing arrangement exists i.e. sales/purchases made at non-standard terms or where loans are provided at non market rates and not repayable on demand then the financing element needs to be separated and posted as a finance income or expense using the effective interest rate method as stated in Section 11.13 of FRS 102.

The standard is silent on how the difference between the transaction price paid or received and the present value of future payments of the future cash flows should be accounted for however example 15 to example 18 below would be indicative of how these can be accounted for.

Where a debt instrument is repayable on demand whether a market rate of interest is charged or not, then the amortised cost is effectively equal to the value of the money received or paid and any transaction costs are expensed as incurred as this represents the present value as it is repayable on demand.

NOTE: where there are no transaction costs and no financing arrangement exists then the amortised cost is the same as the actual amount received or paid, the effective interest rate is the rate stated in the agreement. If Any

11.6.2.4.5.1 Financing arrangement for small entities for loans from directors (who are natural persons) to the entity.

In May 2017 the FRC made an amendment to Section 1 of FRS 102. This inserted a new Section 1.15A into Section 1 of FRS 102. This states where a small entity meets the definition of a small company as stated in Section 280A and 280B of Companies Act 2014 and when there is a loan payable by the entity to a director or close family members which is not repayable on demand and not at market rates (i.e. a financing transaction exists), then under Section.1.15A of FRS 102, the entity has the option to carry this at the amount of the loan received less repayments, plus interest if any of each reporting date (i.e. the entity does not have to follow the rules in Section 11.13 and 11.14 (a) of FRS 102 (the entity does not have to present value the loan or hold at amortised cost). Note the above is a choice, the entity can continue to apply the full rules in Section 11 if it wishes.

If the entity previously applied the rules stated in Section 11.13 and 11.14 (a) of FRS 102 (i.e. present valued the loans at market rates) and decides in the current year to apply the exemption in Section 1.15A of FRS 102 the entity will need to restate the prior year comparatives to reflect the new accounting policy (i.e. retrospective application is required). The disclosure and method to be adopted as a result of the change in accounting policy should be disclosed in accordance with Section 10.12 of FRS 102.

Note where a small entity has loans to directors or loans between companies which come within the definition of a financing transaction or loans from other parties who are not directors (and are not close family members) then the rules in Section 11.13 and 11.14(a) of FRS 102 continue to apply as Section 1.15A of FRS 102 only applies in the case of loans from directors or close family members to a company.

11.6.2.4.6 Steps in determining the effective interest rate

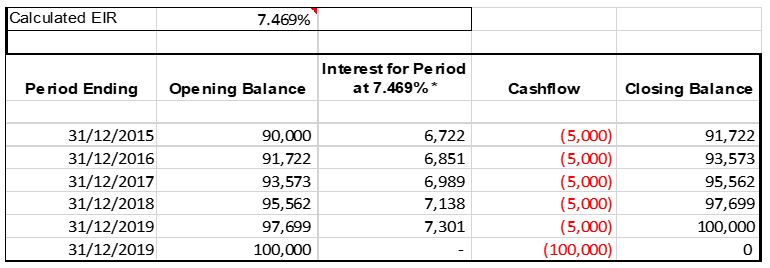

Example 13: loan at market rates with transaction costs (application of Section 11.12 to 11.20 of FRS 102)

Company A obtains a loan from the bank for CU100,000 on 1 January 2015. Arrangement fees of CU10,000 was charged by the bank. The loan carries a market rate of interest of 5% per annum which is charged annually. It is repayable after 5 years. Entity A would calculate the amortised cost and effective interest rate in the following way:

Step 1: Assess whether the instrument meets the definition of a basic instrument and the category it falls into

As this loan meets the definition of a debt instrument where there is no unusual interest rates, then this meets the definition of a basic debt instrument.

Step 2: Determine the method in which the debt instrument should be measured (does section 11.14 (b) apply

As using the amortised cost basis does not create a measurement inconsistency and as this is not a group managed debt instrument where the performance of the group is evaluated on a fair value basis, then it is correct to use the amortised cost basis

Step 3: Assess if there is a financing transaction within the arrangement i.e. is the transaction at non market rates; is unusual extended credit terms provided?

Here the loan is at market rates, therefore there is no financing transaction.

Step 4: Determine amount to be recognised on initial recognition.

The amount to be recognised is the total value of the loan received of CU100,000 less the transaction costs of CU10,000 i.e. CU90,000

Step 5: Determine the effective interest rate and determine the carrying amount on subsequent measurement

The effective interest rate is the rate of interest that exactly discounts the estimated future cash flows through the expected life. In this case the rate is 7.469%. This 7.469% can be determined through trial and error or through the use of a mathematical formula in Microsoft Excel.

Step 6: Decide the journals to be posted at each period end

The journals to be posted in 2015 excluding the payment of the interest are as detailed below such that the amortised cost at 31/12/15 is CU91,722. This will be continued year on year:

| CU | CU | |

| Dr Loan Liability | 10,000 | |

| Cr Bank | 10,000 |

Being journal to recognise the arrangement fee charged

| CU | CU | |

| Dr Interest Expense | CU6,722 | |

| Cr Loan Liability | CU6,722 |

Being journal to recognise effective interest charge for 2015. The effective interest charge will be posted in each of the 5 years as detailed above. The CU5,000 will be set against the liability as it is paid.

11.6.2.4.7 Changes in cash flow estimates (amortised cost model)

Section 11.20 of FRS 102 states the entity shall adjust the carrying amount of the financial asset or financial liability to reflect actual and revised estimated cash flows. The entity shall recalculate the carrying amount by computing the present value of estimated future cash flows at the financial instrument’s original effective interest rate. The entity shall recognise the adjustment as income or expense in profit or loss at the date of the revision. See example 13a below. This will be a common calculation as it is likely that an unforecasted cash flow is made which will then need a reassessment of the amortised cost carrying amount.

NOTE: if anything other than cashflows change then an entity will need to consider if a substantial modification has occurred. See guidance at 11.9.2.2

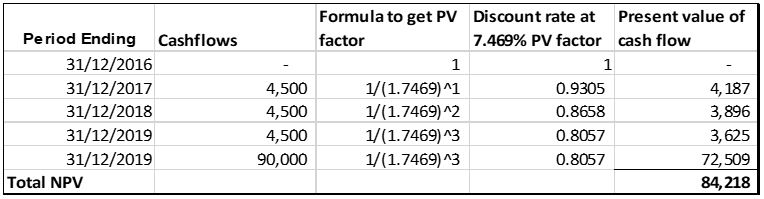

Example 13a: Change in estimate

If we take example 13 and assume that a repayment of CU10,000 was made at the end of year 2 (i.e. 31/12/16). Therefore the new principal to be repaid at 31/12/19 is CU90,000 and the new interest charge is CU4,500 (i.e. CU90,000*5%) for 2017 to 2019.

Calculate the net present value of estimated future cash flows as per below.

The actual carrying amount at 31/12/16 as per the amortised cost table above in example 13 was CU93,573. If we then take account of the additional payment of CU10,000 made on 31/12/16, the carrying amount in the financial statements is CU83,573. The difference of CU645 (CU83,573-CU84,218) is debited to the interest cost in the profit and loss account at 31/12/16.

The remaining difference of CU5,782 (CU90,000-CU84,218) is then charged to the profit and loss account over the remaining life as follows (assuming there is not a substantial modification as discussed further below):

11.6.2.4.8 Non market loans- inter-company loan / director’s loans

Section 11 requires all such loans to be stated at the amortised cost (with the exception of loans from a director who is a natural person to a small entity as defined in the Companies Act in which case these rules are not specifically required to be followed). See Section 11.6.2.4.5.1 for an analysis of the exemption for small entities and when this exemption applies. In reality for a lot of intercom-pany loans which are between related parties, there may be a favourable interest rate or no interest charged on the loan. In this particular case section 11 deems this to be akin to a financing arrange-ment (Section 11.13 of FRS 102) in the receiving company and therefore requires:

- an inputted rate to be charged on these loans; and

- for the loan to be recognised at the present value of the future cash flows discounted at a market rate of interest for similar debt instrument.

11.6.2.4.8.1 Determining the market rate of interest

The inputted rate is the interest rate that would be charged by a bank if the entity had to obtain exter-nal loan financing. Even where interest is charged on the loan but it is not at market rates, the differ-ence between the market rate and the rate charged is used to determine the amortised cost.

Although the standard does not specify where the difference between the amount initially recognised and the amount received is to be posted in the P&L or equity or as an investment as appropriate. See section 11.6.2.4.8.2.

11.6.2.4.8.2: Analysis of debt and credits on initial recognition of loans – financing arrangements.

Depending on the circumstances the below accounting treatment may be used when assessing where the difference in initial recognition should be recognised:

- Where the loan is received from a parent company, in the receiving company; the difference is posted as a capital contribution to equity and the other side of the transaction is posted to the loan liability. The posting to equity reflects the fact that the parent company has provided a gift i.e. an interest free loan or a non-market interest rate loan to its subsidiary. See Example 14 below.

In the parent company financial statements, the difference is posted as an investment i.e. credit to bank, debit to investment and debit to debtors on initial recognition. A review would have to be performed to ensure the amount stated including this adjustment does not result in the carrying amount of the investment being in excess of its recoverable amount.

- Where the loan is received from a non-group company or a group company that is not its parent or a shareholder/director, then in the books of the giver the difference is posted as a debit to interest expense in the books of the equity where it is deemed to be a distribution (applicable for a loan to a sister company). In the books of the receiver, for loans between group companies where no company in the arrangement is the parent a credit would go to interest income for non-group companies and as a capital contribution for transactions between sister companies where applicable.

See further possibilities for accounting for certain loans below:

- In the subsidiary accounts and loan received from parent company = recognised as a capital contribution in equity and the corresponding entry posted to the loan liability. See Example 14 below.

- In the subsidiary accounts and loan from sister company = recognised as a capital contribution in equity OR as a credit to the P&L; and the corresponding entry posted to the loan liability. See Example 16a below.

- In the subsidiary accounts and loan provided to parent company = recognised as a distribution in equity OR a debit to interest costs in the P&L and the corresponding entry posted to the loan asset. See Example 16b below.

- In the subsidiary accounts and loan provided to a sister company = recognised as a distribution in equity OR a debit to interest costs in the P&L and the corresponding entry posted to the loan asset. See Example 16A below..

- In the Parent accounts and loan received from subsidiary company = recognised as a credit to the P&L as a deemed distribution from the subsidiary (in the line income from group undertakings) and the corresponding entry posted to the loan liability. See Example 16B below.

- In the Parent accounts and loan given to subsidiary company = recognised as an investment in the subsidiary and the corresponding entry posted to the loan asset. See Example 14 below.

- In the company accounts and loan provided to shareholder = recognised as a distribution in equity OR a debit to interest costs in the P&L and the corresponding entry posted to the loan asset. For an illustration of same refer to the journals in Example 16a below.

- In the company accounts and loan received from shareholder = recognised as a capital contribution in equity and the corresponding entry posted to the loan liability.

- In the company accounts and loan provided to director/employee who is not a shareholder = recognised as a debit to interest cost in the P&L and the corresponding entry posted to the loan asset. See Example 15 below.

- In the company accounts and loan received from director/employee third party who is not a shareholder = recognised as a credit in interest income in the P&L and the corresponding entry posted to the loan liability (subject to a small company availing of the exemption detailed in 11.6.2.4.5.1 for loans from directors to companies/entities). See Example 15 of this section for an example.

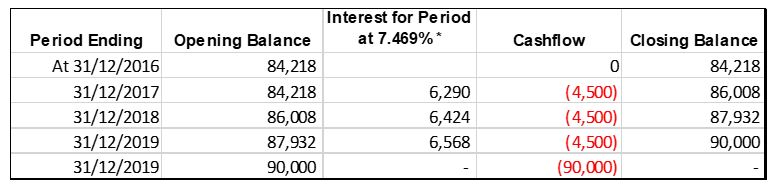

Example 14: Intercompany loan from a parent company

Company A is a subsidiary of Parent B. Parent B provides a loan to Company A for 5 years for CU200,000 on 01/01/2015. No interest is charged on the amount loaned. The market rate of interest that would be charged on this loan by a third party i.e. a bank would be 5%. In the analysis below we have assumed the answers to steps one and two are as per example 13 above. (Step 1 Asses whether the instrument meets the definition of a basic instrument and the category it falls into. Step 2 Determine the method in which the debt instrument should be measured (does section 11.14 (b) apply). Under Section 11, the following accounting transactions will be required in the books of the parent and the subsidiary:

Step 3: Assess if there is a financing transaction within the arrangement i.e. is the transaction at non market rates; is unusual extended credit terms provided?

Step 4: Determine amount to be recognised on initial recognition and subsequent measurement

Given that a financing arrangement exists, there is a need to determine the present value of the future payments using the inputted market rate. Therefore the amount to be recognised initially is:

CU200,000 / (1.05)^5 = CU156,705

Therefore the journals to post in Company A’s TB are:

| CU | CU | |

| Dr Bank | 200,000 | |

| Cr Interco Loan | 200,000 |

Being journal to recognise receipt of the loan

| CU | CU | |

|

Dr Interco Loan (CU200,000- CU156,705) |

43,295 | |

| Cr Equity/Capital Contribution | 43,295 |

Being journal to reflect deemed gift from the parent for the fact that the loan was given interest free.

In the parent company financial statements the journals on initial recognition would be:

| CU | CU | |

| Dr Interco Loan | 200,000 | |

| Cr Bank | 200,000 |

Being journal to recognise provision of the loan

| CU | CU | |

| Dr Investment | 43,295 | |

|

Cr Interco Loan (CU200,000-CU156,705) |

43,295 |

Being journal to recognise the deemed investment in Company as a result of providing a favourable loan

Step 5: Determine the effective interest rate

The effective interest rate is the rate of interest that exactly discounts the estimated future cash flows through the expected life. In this case the rate is 5% which is the same as the market interest rate as there was no transaction costs.

Step 6: Decide the journals to be posted at each period end.

In Company A financial statements the journals to be posted at 31/12/2015 are as detailed below such that the amortised cost at 31/12/15 is 164,540. This will be continued year on year:

| CU | CU | |

| Dr Interest Expense | 7,835 | |

| Cr Loan Liability | 7,835 |

Being journal to recognise effective interest charge for 2015. The effective interest charge will be posted in each of the 5 years as detailed above assuming no changes in the cash flow occur.

In the parent company financial statements the journals to be posted at 31/12/2015 are as detailed below such that the amortised cost at 31/12/15 is CU164,540. This will be continued year on year:

| CU | CU | |

| Dr Loan Liability | 7,835 | |

| Cr Interest Income | 7,835 |

Being journal to recognise effective interest charge for 2015. The effective interest charge will be posted in each of the 5 years as detailed above.

NOTE: if the terms of the loan agreement stated that the loan was repayable on demand, the carrying amount on initial recognition would be CU200,000 as this is the deemed present value of future payments, therefore no deemed interest would need to be recognised.

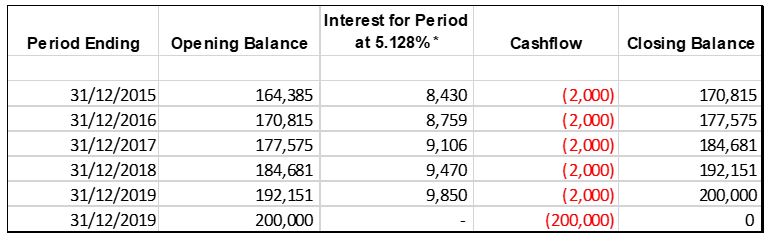

Example 15: Loan provided to the company by a director

A shareholder/director provides a loan to Company A for 5 years for CU200,000 on 01/01/2015. Interest of 1% is charged on the amount loaned annually (i.e. CU2,000 per annum). The market rate of interest that would be charged on this loan by a third party i.e. a bank would be 5%. In the analysis below we have assumed the answers to steps one and two are as per above. (Step 1 Asses whether the instrument meets the definition of a basic instrument and the category it falls into. Step 2 Determine the method in which the debt instrument should be measured (does section 11.14 (b) apply). Assume that there are no timing differences for deferred tax purposes. Under Section 11, the following accounting transactions will be required in the books of Company A:

Step 3: Assess if there is a financing transaction within the arrangement i.e. is the transaction at non market rates; is unusual extended credit terms provided?

Here the loan is at non-market rates as there is no interest charged, therefore there is a financing transaction. The interest rate charged on the loan is 4% (5%-1%) below market rates.

Step 4: Determine amount to be recognised on initial recognition

Given that a financing arrangement exists, there is a need to determine the present value of the future of the future payments using the inputted market rate. Therefore amount to be recognised initially is:

CU200,000 / (1.04)^5 = CU164,385

Therefore, the journals to post in Company A’s TB are:

| CU | CU | ||||

| Dr Bank | 200,000 | ||||

| Cr Directors Loan | 200,000 | ||||

Being journal to recognise receipt of the loan

| CU | CU | |

|

Dr Directors Loan (CU200,000-CU164,385) |

35,615 | |

| Cr Interest Income | 35,615 |

Being journal to reflect the benefit received from the loan being received interest free.

NOTE: if the director was instead a shareholder/director, then there could be an argument to say that the credit should go to equity as opposed to the P&L as the shareholder has in effect given the company the benefit of an interest free loan which is akin to a capital contribution.

Step 5: Determine the effective interest rate

The effective interest rate is the rate of interest that exactly discounts the estimated future cash flows through the expected life. In this case the rate is 5.128%. This rate is determined through trial or error or through the use of a mathematical model in Excel.

Step 6: Decide the journals to be posted at each period end.

The journals to be posted at 31/12/2015 are as detailed below such that the amortised cost at 31/12/15 is CU170,815. This will be continued year on year:

| CU | CU | |

| Dr Interest Expense | 8,430 | |

| Cr Loan Liability | 8,430 |

Being journal to recognise effective interest charge for 2015. The effective interest charge will be posted in each of the 5 years as detailed above.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 1: Investment in shares.

Example 2: Investment in shares – 15%.

Example 3: variable and fixed interest payments.

Example 5: Fixed and variable interest payments.

Example 6: Fixed rate loan for a set period and then a reversion to the banks variable rate.

Example 8: Loan/bond which is convertible into the borrower’s equity.

Example 9: Loan issued which is linked to a general inflation index.

Example 10: Variation in return.

Example 11: Prepayment options.

Example 12: Loan extension option.

Example 12a: Unguaranteed Capital

Example 12b: Collective investment funds.

Example 13: loan at market rates with transaction costs.

Example 13a: Change in estimate.

Example 14: Intercompany loan from a parent company.

Example 15: Loan provided to the company by a director

Example 16a: Intercompany loan from a related party or a fellow subsidiary.

Example 16b: Loan from subsidiary to the parent company.

Example 16c: Sale with unusual credit terms.

Example 16d: Purchase with unusual credit terms.

Example 17a: Loans repayable on demand..

Example 17b: Loan repayable on demand but with notice of 1 year and 1 day.

Example 18: Bonds – discount/premium.

Example 20: Impairment of debt instruments.

Example 20a: Bonds with an impairment

Example 21: Asset recognised due to settlement

Example 22: Sale of debtors with recourse.

Example 23: Sale of debtors without recourse.

Example 24: Transfer of assets at fair value subject to a call option.

Example 25: Substantial modification of a loan.

Example 26: Sample disclosure requirements

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text _builder_version=”3.0.98″ background_layout=”light”]

Example 16a: Intercompany loan from a related party or a fellow subsidiary

Company A is a sister company/fellow subsidiary of Company B. Company B provides a loan to Company A for 5 years for CU200,000 on 01/01/2015. 1% rate of interest is charged on the amount loaned. The market rate of interest that would be charged on this loan by a third party i.e. a bank would be 5%.

Assume there are no timing differences for deferred tax purposes. The journals in this particular instance for each entity are (note there are two choices here, so an entity should look at the substance of the transaction when determining which journals to post):

The present value of future cash flows = CU200,000 / (1.04)^5 = CU164,385

Journals on initial recognition in Company A

| CU | CU | |

| Dr Bank | 200,000 | |

| Cr Related Party Loan Liability | 200,000 | |

| Dr Related Party Loan Liability (CU200,000 -CU164,385) | 35,615 | |

| Cr Capital Contribution | 35,615 |

Being journal to recognise the receipt of the loan and the adjustments to show the loan at its present value of future payments (posted to equity as a capital contribution as the parent company has forced the other subsidiary to give that company a favourable loan).

OR

| CU | CU | |

| Dr Bank | 200,000 | |

| Cr Related Party Loan Liability | 200,000 | |

| Dr Related Party Loan Liability (CU200,000-CU164,385) | 35,615 | |

| Cr Interest Income | 35,615 |

Being journal to recognise the receipt of the loan and the adjustments to show the loan at its present value of future payments (this journal would only apply where the fellow subsidiary gave the loan voluntarily without the demand by the parent)

The journals for subsequent years will be the same as included in example 15 above.

Journals on initial recognition in the fellow subsidiary/related party company:

Journals on initial recognition in the fellow subsidiary/related party company (note there are two choices here, so an entity should look at the substance of the transaction when determining which journals to post):

| CU | CU | |

| Dr Related Party Loan Asset | 200,000 | |

| Cr Bank | 200,000 | |

| Cr Related Party Loan Asset | 35,615 | |

| Dr Distribution in Equity | 35,615 |

Being journal to recognise the provision of the loan and the adjustments to show the loan at its present value of future payments (posted to equity as a debit as it is effectively a distribution to the Parent Company as it has forced this company to provide a favourable loan to its subsidiary)

OR

| CU | CU | |

| Dr Related Party Loan Asset | 200,000 | |

| Cr Bank | 200,000 | |

| Cr Related Party Loan Asset | 35,615 | |

| Dr Interest Expense | 35,615 |

Being journal to recognise the provision of the loan and the adjustments to show the loan at its present value of future receipts, (this journal would only apply where the fellow subsidiary gave the loan voluntarily without being demanded by its parent entity).

On subsequent measurement the journals would be to credit interest income and debit related party loan asset so as to show the correct amortised cost amount as calculated above.

In an instance where Company A provided a loan to the directors who is a shareholder or shareholders, the accounting treatment in Company A’s books would be the same as the journals for the related party entity that gave the loan above. If the director is not a shareholder, then the option to debit to other reserves with the distribution would not apply and therefore it would have to hit interest costs or employee costs.

Example 16b: Loan from subsidiary to the parent company

If the above loan in example 16a was from a subsidiary to a parent company the journals required in the parent company would be

CU CU

Dr Bank 200,000

Cr Related party loan (CU200000 = CU43295 ) 156,702

Cr Income from interest in group undertakings in P&L 43295

In the subsidiary financial statements where the loan was provided to the parent company, the journals required are:

CU CU

Dr Related party loan asset 156702

Dr Distribution in equity 43295

Cr Bank 200000

11.6.2.4.9 Sales and purchases made under unusual credit terms – Debtors/creditors

As per section 11.13 and 11.14 (a) of FRS 102 where sales or purchases are made under unusual credit terms the effective interest rate and amortised cost model must be used. See examples below.

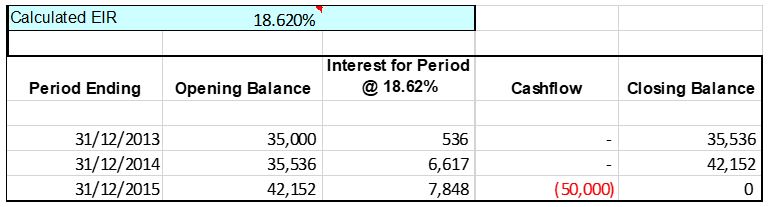

Example 16c: Sale with unusual credit terms

Company A sold goods worth CU50,000 with unusual credit terms on 01/12/13. The credit provided is for a period of up to 31/12/15. The normal cash price for these goods would be CU35,000. The difference of CU15,000 is determined to be a financing transaction. The effective interest rate is calculated at 18.62% as per below. The effective interest rate is determined so as to write the deemed interest into the P&L over the life of the transaction. The effective interest rate is determined through trial and error or through the use of Excel. If the cash price was not known then you have to present value the amount at a market rate of interest.

The adjustments required to accounted for this are as follows:

| CU | CU | |

| Dr Trade Debtors | 50,000 | |

| Cr Sales | 50,000 |

Being journal to recognise the sale

| CU | CU | |

|

Dr Sales (CU50,000-CU35,000) |

15,000 | |

| Credit Trade Debtors | 15,000 |

Being journal to reflect the deemed financing element of the purchase so as to show the correct amortised cost

| CU | CU | |

| Dr trade debtors | 536 | |

| Cr Finance Income in P&L (so that the carrying amount is now CU35,536) | 536 |

Being journal reflect the deemed interest income in the profit and loss for the year for one month. The same type of journal is posted for the other two years.

Example 16d: Purchase with unusual credit terms

If we take example 16c, and show the accounting for the purchaser in this case. For the purchasing company the journals to post are:

| CU | CU | |

| Dr Inventory | 50,000 | |

| Cr Trade Creditors | 50,000 |

Being journal to reflect purchase of stock

| CU | CU | |

| Dr Trade Creditors | 15,000 | |

| Cr Inventory | 15,000 |

Being journal to reflect the deemed financing element of the sale so as to show the correct amortised cost

| CU | CU | |

|

Dr Finance Expense in P&L (so that the carrying amount is now CU35,536) |

536 | |

| Cr Trade Creditors | 536 |

Being journal reflect the deemed interest income in the profit and loss for the year for one month. The same type of journal is posted for the other two years.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text _builder_version=”3.0.98″ background_layout=”light”]

11.6.2.4.10 Employee Loans

Example 17: Employee loan

If this loan was to an employee who is not a shareholder, then the option in example 16A at 11.6.2.4.8.2 to debit other reserves with the distribution would not apply and therefore it would have to be recognised in employee costs and not to interest costs.

11.6.2.4.11 Loans repayable on demand

Where the terms of the loan are such that it is repayable on demand, even where no interest rate is charged, the present value of the loan is the amount received at 11.6.2.4.8.2 which therefore equates to its amortised cost. Therefore, the calculations performed in the examples above would not be re-quired as the value of the loan received is the carrying amount it should be shown at in the financial statements. If the example at 11.6.2.4.8.2 were all repayable on demand then all of the aforemen-tioned steps at 11.6.2.4.8.2 would not be applicable.

Example 17a: Loans repayable on demand

Company A received a loan of CU100,000 from Company B. Transaction fees of CU1,000 were incurred. No interest is charged on this loan. The loan is repayable on demand. In this case as this loan is repayable on demand, the CU1,000 transaction fees are expensed as incurred and the fair value of the loan is CU100,000 which is the amount to be recognised in the financial statements.

11.6.2.4.12 Loan repayable on demand but with notice of 1 year and 1 day

In this situation where the loan is at non-market rates and not repayable on demand then a financing arrangement exists and as required by Section 11.13 of FRS102 it must be present valued at the market rate of interest at initial recognition.While Section 11.14 of FRS 102 states that present valuing is not required if it is repayable/refundable within 12 months of period end, it is clear in Section 11.13 of FRS 102 where a financing arrangement exists then it must be present valued regardless of the length of the financing.

However, given that the loan is on demand the interest is not unwound until it has been demanded.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text _builder_version=”3.0.98″ background_layout=”light”]

Example 17b: Loan repayable on demand but with notice of 1 year and 1 day

Company A is a subsidiary of Parent B. Parent B provides a loan to Company A for CU200,000 on 01/01/2015. No interest is charged on the amount loaned. The terms of the loan are such that Parent B can demand repayment of the loan at any time but Parent B must give notice to Company A of 1 year and 1 day. The market rate of interest that would be charged on this loan by a third party i.e. a bank would be 5%. Assume for the purposes of this example that at the start of year 4 Parent B demands repayment of the loan and therefore starts the 1 year and 1 day notice period.

As the loan is at non-market rates (i.e. interest free) and not repayable on demand then under Section 11.13 of FRS 102 this loan must be present valued over the financing period which is one year and one day.

Under Section 11, the following accounting transactions will be required in the books of the parent and the subsidiary:

1 Determine amount to be recognised on initial recognition

Given that a financing arrangement exists, there is a need to determine the present value of the future payments using the inputted market rate. Therefore the amount to be recognised initially is:

CU200,000 / (1.05)^1.0027 = CU190,451

| CU | CU | |

| Dr Bank | 200,000 | |

| Cr Interco Loan | 200,000 |

Being journal to recognise receipt of the loan

| CU | CU | |

|

Dr Interco Loan (CU200,000- CU190,451) |

9,549 | |

| Cr Equity/Capital Contribution | 9,549 |

Being journal to reflect deemed gift from the parent for the fact that the loan was given interest free.

In the parent company financial statements the journals on initial recognition would be

| CU | CU | |

| Dr Interco Loan | 200,000 | |

| Cr Bank | 200,000 |

Being journal to recognise provision of the loan

| CU | CU | |

| Dr Investment | 9,549 | |

|

Cr Interco Loan (CU200,000-CU190,451) |

9,549 |

Being journal to recognise the deemed investment in Company as a result of providing a favourable loan

2 Determine the effective interest rate

The effective interest rate is the rate of interest that exactly discounts the estimated future cash flows through the expected life. In this case the rate is 5% which is the same as the market interest rate as there was no transaction costs. Note this only gets released when the loan has been demanded.

3 Journals required on subsequent recognition for year to the end of year 3.

There are no journals required in years 1 to 3 in either the subsidiary or parent entity accounts as the loan has not been demanded so therefore the interest does not have to be unwound during this period. The loan can be shown as being repayable in greater than one year on the financial statements of both companies.

4 Journals required on subsequent recognition – start of year 4.

As Parent B has now demanded repayment of the loan, the interest must be unwound from that date which is the 1 January 2018 (start of year 4). See below the effective interest rate calculation and amounts to be unwound:

The journals required in Company A’s accounts during year 4 are:

| CU | CU | |

| Dr Interest Expense | 9,496 | |

| Cr Loan Liability | 9,496 |

Being journal to recognise effective interest during year 4. At the end of year 4 this 200,000 will be shown as repayable within one year in the balance sheet.

In the parent company financial statements the journals to be posted

| CU | CU | |

| Dr Loan Liability | 9,496 | |

| Cr Interest Income | 9,496 |

Being journal to recognise effective interest charge for year 4.

The remaining CU53 will be posted in year 5 which the journals similar to the above.

11.6.2.4.13 Subordination

Entities should review third party agreements (e.g. enterprise Ireland agreements, bank loan agree-ments etc.) to assess whether as part of these agreements, the entity has agreed to subordinate in-tercompany or directors’ loans. If this is the case then effectively the parties have agreed to alter the agreed terms and therefore such loans cannot be treated as being repayable on demand so instead present valuing of these loans will be required.

11.6.2.4.14 Deferred Tax

No deferred tax arises of the present value adjustments as these are not taxable or tax deductible under revenue rules. Therefore as there is no tax impact, there is no timing difference. Likewise for fees amortised on an effective interest rate basis this is allowed for tax/taxable as released into the P&L so therefore there are no timing differences.

11.6.2.4.15 Variable interest rate over the life of the loan

Where a variable interest rate is charged on a loan and no transaction costs are incurred, then the amount that this will be carried at is the actual amount received/paid as the interest rate will be charged to the P&L as incurred which is based on a market interest rate at that time.

Where on the other hand, a variable interest rate loan is issued by a group company which is below market rates, the variable interest rate to be used in the amortised cost calculation is the expected variable interest rate over the life of the loan (unless there is a repricing element within it in which case it would be up until the date of the repricing).

11.6.2.6.16 Issues surrounding directors or intra-group loans

In the majority of cases it is likely that there may be no formal signed agreements in place in relation to these loans. If this is the case, each loan should be looked at separately to assess if there are any implied contractual terms. An assessment has to be made as to whether under the terms that repayment was not likely to have been required in the near future.

Consideration would also need to be given as to whether the loans were shown as repayable within one year under old GAAP or whether they were included in the financial statements as being payable/repayable after more than one year. If it is felt that the substance is that it is akin to a capital contribution which may never have to be paid, it is no longer in Section 11 scope and instead comes within the remit of Section 22 of FRS 102. If the agreement is such that this will never be repayable in the future and there is documentation to support that it is a capital contribution, then it would be treated as equity.

Where the substance of the loan based on the facts and circumstances indicate that it is repayable on demand and therefore the amount received/paid is what the financial asset/liability will be carried at, auditors will need to assess where a letter of support is required, if this letter of support from the parent company contradicts the repayable on demand concept in relation to that loan. If the wording in the letter of support contradicts the repayable on demand concept then the entity will have to carry out the detailed exercise to ascertain the amortised cost, the market rate of interest when the loan was received/advanced etc.

Therefore care needs to be taken when the parent company provides a letter of support. The parent company should ensure that the letter of support does not evidence the contractual terms of intra group financing or that use the incorrect wording. In reality the letter of support should state that the parent will only provide support if the subsidiary is unable to meet its debts as they fall due.

Where there are no terms attached to the loan and a letter of support is put in place then the letter of support effectively determines the terms (if the loan is due to the parent). If there are formal terms then a letter of support does not override the terms of the loan as this loan agreement is a separate agreement and is not altered by an intention given by a party to the loan (i.e. the parent company stated that they do not intend to call in the loan within 12 months of sign off of the Financial Statements, however this does not alter the legal agreement).

11.6.2.4.16.1 Factors that indicate a related party loan is not at market rates

Factors which indicate a loan has been provided/advanced at non market rates are:

- It is interest free or the interest rate is excessively high or low

- The interest charged is not in line with what has been charged by third parties in the past or presently and the loan advanced is riskier than what the third party advanced but yet the interest rate is lower.

- Transfer pricing adjustments being made to reflect market rates.

11.6.2.4.17 Bonds

Where a bonds meets the definition of a basic instrument as stated in Section 11.9 of FRS 102, and transaction costs or premiums or discounts on purchase are released to the profit and loss on an effective interest rate basis in line with Section 11.13 of FRS 102.

Example 18: Bonds – discount/premium

Company A acquired a capital guaranteed government bond for CU950,000 on 30 April 2016 and matures on 16 March 2021. The bond was for CU1 million and had a coupon rate of 5% with commission costs of CU2,000.

This should be accounted for under Section 11 of FRS 102. The discount should be amortised into the P&L over the life of the bond on the effective interest rate basis and held at amortised cost. The effective interest rate is calculated by mathematical formula. It is a rate of .0693% per month as per below.

The journals required to account for this in the year ended 31 December 2016 are:

Journal 1:

| CU | CU | |

| Dr investment-government bond | 952,000 | |

| Cr Bank | 952,000 | |

Being journal to reflect the government bond at cost inclusive of transaction fees on initial recognition.

Journal 1:

| CU | CU | |

| Dr investment-government bond | 5,291 | |

| Cr Other Income in P&L | 5,291 |

Being journal to unwind the discount on the bond up to 31 December 2016 so as to come to CU 957,291

Note when the coupon on the government bond is paid in the year, you will continue to recognise the full 5% in income i.e.

Journal 2:

| CU | CU | |

|

Dr bank (CU1,000,000 * 5%) |

50,000 | |

| Cr Interest receivable and other income | 50,000 |

At each period end the Company must review the bond for indicators of impairment which are given in Section 11. Where these are present they should be written down to the market value of bond/recoverable amount.

If the above bond was purchased at a premium a similar treatment would be required (except there would be a debit to release the premium).

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][/et_pb_column][/et_pb_row][/et_pb_section]