[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”]

[breadcrumb]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.106″ title=”Index ” open=”off”]

Contents

Section 1: Scope of financial reporting standard 102

1.1.1 Extract from FRS102: Section 1.1-1.2A.

1.2 Basis of preparation of financial statements.

1.2.1 Extract from FRS102: Section 1.3-1.7.

1.2.2.1 The choices available to entities when deciding what paperwork to use.

1.2.2.2 Where entities must apply a particular standard.

1.3 Reduced disclosures for subsidiaries (and ultimate parents)

1.3.1 Extract from FRS102: Section 1.8-1.13.

1.3.2.1 Qualifying entity defined.

1.3.2.1.1 What entities are not qualifying entities in practical terms?

1.3.2.2 What are the disclosure exemptions for qualifying entities?

1.3.2.3 What needs to be put in place in order for the disclosure exemption to be claimed?

1.4 Date from which effective and transitional arrangements.

1.4.1 Extract from FRS102: Section 1.14-1.15.

1.4.2.2 July 2015 amendments – where applicable.

1.4.2.3 Amendments to FRS 102 – Triennial review – adaption requirements.

1.4.2.4 Small entity get out for some non-market loans.

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.17.6″]

The below extracts and guidance is applicable for periods beginning before 1 January 2019 and are based on the September 2015 version of FRS 102. For periods beginning on or after 1 January 2019, the March 2018 version of FRS 102 applies which incorporates the changes made by the Triennial review of FRS 102. Note the March 2018 version of FRS 102 can be voluntarily applies for periods beginning before 1 January 2019. For the extracts from the March 2018 version of FRS 102 and the related guidance please click on the following link. For details of a summary of the main changes as a result of the triennial review please see the following link.

1.3 Reduced disclosures for subsidiaries (and ultimate parents)

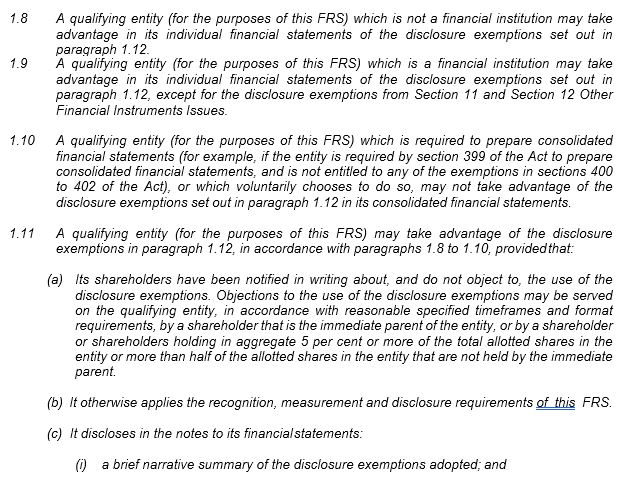

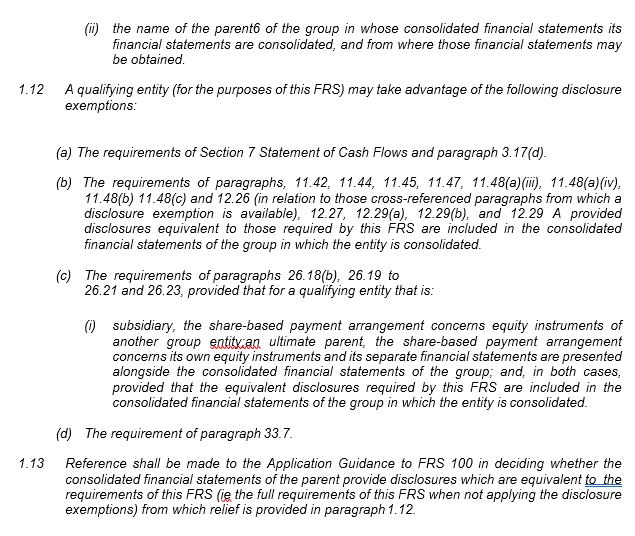

1.3.1 Extract from FRS102: Section 1.8-1.13

1.3.2 OmniPro comment

1.3.2 OmniPro comment

1.3.2.1 Qualifying entity defined

A qualifying entity is defined in FRS 102 as ‘A member of a group where the parent of that group prepares publically available consolidated financial statements which are intended to give a true and fair view (of the assets, liabilities, financial position and profit or loss) and that member is included in the consolidation’.

1.3.2.1.1 What entities are not qualifying entities in practical terms?

In effect the following entities cannot apply the reduced disclosure framework:

- Entities who are not members of a group i.e. individual entities;

- Entities who are members of a group but group consolidated financial statements are not prepared (e.g. due to the group meeting the small company exemptions);

- Parent entities that prepare consolidated financial statements;

- Where the entity is not included in the consolidation of its parent due to it being immaterial to the group etc;

- Where equivalent disclosures are not included in the consolidated financial statements;

- Where disclosures have been included but they have not formed part of the audited figures where the entity is being audited; and

- Entities that are financial

1.3.2.2 What are the disclosure exemptions for qualifying entities?

Where the entity is a qualifying entity the following disclosure exemptions are available:

- No requirement to provide cash flow statements;

- No requirement to provide details of number of shares outstanding at the beginning and end of the year;

- No requirement for key management personnel compensation to be disclosed. However the usual directors remuneration disclosures under company law are required;

- Share based payment disclosures (where shares are given in the parent)*;

- Related party disclosure with 100% owned group companies (available to all groups in any event regardless of whether it meets the qualifying disclosure definition);

- Certain financial instrument disclosures (detailed references in Section 1.12A(c)) of FRS 102*. Company law still requires disclosure of:

- Significant assumptions about the valuation models and techniques for financial instruments held at fair value;

- The fair value of instruments in each category and changes in fair value included in the profit and loss or included in the fair value reserve;

- The nature and extent of derivative instruments at fair value, including significant terms that might affect future cash flows;

- A reconciliation of the fair value

*denotes the fact that disclosure exemptions only available where equivalent disclosures are included in the consolidated financial statements.

1.3.2.3 What needs to be put in place in order for the disclosure exemption to be claimed?

As stated in Section 1.11 of FRS 102 before the disclosure exemptions can be claimed the following is required:

- shareholder approval is required;

- recognition, measurement requirements under FRS 102 are applied;

- a disclosure is made in the financial statements detailing the exemptions

Example 1: Disclosure example for a qualifying entity applying reduced disclosure exemptions

‘FRS 102 sets out a reduced disclosure framework for a ‘qualifying entity’ as defined in FRS 102 which addresses the financial reporting requirements and disclosure exemptions in the financial statements of qualifying entities that otherwise apply the recognition, measurement and disclosure requirements of FRS 102. The company is a qualifying entity for the purposes of FRS 102. Note X gives details of the company’s parent and from where its consolidated financial statements prepared in accordance with (insert GAAP) GAAP may be obtained. The company has notified its shareholders in writing about, and they do not object to, the use of disclosure exemptions availed of by the company in these financial statements.’

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 1: Disclosure example for a qualifying entity applying reduced disclosure exemptions.

Example 2: Disclosure detailing application of July 2015 amendments.

Example 3: Disclosure detailing application of July 2015 amendments.

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]