[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off”][et_pb_column type=”4_4″][et_pb_post_title admin_label=”Post Title” global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#ffffff” global_module=”1228″][et_pb_row admin_label=”Row” global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text admin_label=”Text” global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-1/” type=”big” color=”red”] Return to Section 1 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Example 1: Intermediary holding company

UK Parent A is a UK company with a functional currency as CU. It has a 100% subsidiary called Intermediate Co which in turn owns 100% of a trading subsidiary Company B whose functional currency is FC.

The Intermediate Co merely holds the investment in Company B and obtains FC borrowings from the bank to make this investment. The borrowings are guaranteed by Parent UK Co.

In this instance what is the functional currency of Intermediate Co?

Applying the guidance in Section 30.3 to 30.5 as follows:

Primary indicators:

- currency in which costs or income is derived – As Intermediate Co does not generate revenue and only incurs minimal expenses, this indicator is not that relevant.

Secondary indicators:

- Operating activities – this is not relevant as the company does not generate any cash flows it merely holds the investment

- Financing activities – Intermediate Co has obtained FC borrowings to make the acquisition, however this is only a secondary indictor and section 30.5 has to be reviewed for foreign operations.

Factors specific to foreign operations:

- Degree of autonomy – Section 30.5(a) states that where the activities of the foreign operation is an extension of the reporting entity and has very little autonomy, then the foreign entity is likely to have the functional currency of its parent. – In this example, as Intermediate Co has merely been put in funds through UK Parent A (by parent A providing finance by way of guarantee to the bank) and it has akin made an investment into a subsidiary on UK Parent Co’s behalf, this would indicate that the functional currency of the parent is that of the UK Parent Co i.e. FC.

- Frequency of transaction with parent – All transactions are with the parent thereby indicating it should take the functional currency of the parent.

- Cash flow impact on reporting entity – not that relevant

- Financing – Parent Co has provided the funds therefore this suggest it is an extension of the Parent Co.

Based on the facts and circumstances outlined Intermediate Co’s functional currency should be CU and not FC.

Example 2: Intermediate holding Company

If we take example 1 and this time assume that no bank borrowings was obtained and instead UK Parent Co provided the loan finance or equity finance. In this case the same determination would be obtained i.e. the functional currency of Intermediate Co is CU.

Example 3: Intermediate holding Company

If we take example 1 and in this case the money to fund the investment in Company B is obtained from a sister company. In this case the functional currency of the Intermediate Co would likely be the functional currency of the sister company.

Example 4: Functional currency

Company A is a trading company resident in France. Company A predominately sells its goods in FC with 30% of sales being made in CU. The company’s principal costs are wages and stock purchases. These are all paid in FC.

Based on the primary indicators, the functional currency of Company A is CU. The secondary indicators do not need to be reviewed as it is clear from the primary indicators.

Example 5: Functional currency

Company A is a trading company resident in France. Company A predominately sells its goods in FC with 30% of sales being made in CU. The company’s principal costs are wages and stock purchases. These are mainly denominated and settled in CU.

The company is financed through FC borrowings.

In this case the primary indicators do not give conclusive evidence so therefore one must move to the secondary indicators. The secondary indicators are financing activities and from review of same we can see that this is carried out in FC.

On this basis it would appear the functional currency is FC.

Example 6: Retranslation of monetary asset – purchase

Company A whose functional currency is CU purchased good’s from a foreign supplier on credit for FC10,000 on 1 October when the exchange rate was CU1=FC0.80p. Company A’s year end is 31 December. The invoice was not paid by the year end date and exchange rate was CU1=FC0.85p. The invoice was paid on 30 January of the following year when the exchange rate was CU1=FC0.90p. The accounting treatment of this transaction is:

At date of transaction

|

|

CU |

CU |

|

Dr Inventory (FC10,000/.80p) |

12,500 |

|

|

Cr Accounts Payable |

|

12,500 |

Being journal to recognise the purchase at the transaction date

At year end date

|

|

CU |

CU |

|

Dr Accounts Payable |

735* |

|

|

Cr Unrealised Foreign Exchange Gain in P&L |

|

735 |

Being journal to recognise the foreign exchange gain for the movement in rate to year end

*the amount to be recognised as a foreign exchange gain is determined to be the difference between the amount recognised at the date of transaction of CU12,500 less the year end carrying amount using the year end spot rate of CU11,765 (i.e. FC10,000/.85)= CU735

At payment date

|

|

CU |

CU |

|

Dr Accounts Payable (being carrying amount at 31 December) |

11,765 |

|

|

Cr Bank (FC10,000/0.90) |

|

11,111 |

|

Cr Foreign Exchange Gain in P&L |

|

654

|

Being journal to reflect realised profit on settlement

Example 7: Retranslation of monetary asset – sale

Company A whose functional currency (but also sells goods in FC) is CU sold good’s to a foreign customer on credit for FC10,000 on 1 October when the exchange rate was CU1=FC0.80p. Company A’s year end is 31 December. The invoice was not paid by the year end date and exchange rate was CU1=FC0.85p. The invoice was paid on 30 January of the following year when the exchange rate was CU1=FC0.90p. We are ignoring the stock movement in the example. The accounting treatment of this transaction is:

At date of transaction

|

|

CU |

CU |

|

Dr Trade Debtors (FC10,000/.80p) |

12,500 |

|

|

Cr Revenue |

|

12,500 |

Being journal to recognise the sale at the transaction date

At year end date

|

|

CU |

CU |

|

Dr Unrealised Foreign Exchange Loss in P&L |

735 |

|

|

Cr Trade Debtors |

|

735* |

Being journal to recognise the unrealised foreign exchange loss for the movement in rate to year end

*the amount to be recognised as a foreign exchange loss is determined to be the difference between the amount recognised at the date of transaction of CU12,500 less the year end carrying amount using the year end spot rate of CU11,765 (i.e. FC10,000/.85)= CU735

At payment date

|

|

CU |

CU |

|

Dr Bank (FC10,000/0.90p) |

11,111 |

|

|

Dr Foreign Exchange Loss in P&L |

654 |

|

|

Cr Trade Debtors (being carrying amount at 31 December) |

|

11,765 |

Being journal to reflect realised loss on settlement

Example 8: Retranslation of non-monetary asset

Company A whose functional currency is CU purchased a fixed asset from a foreign supplier on credit for FC10,000 on 1 October when the exchange rate was CU1=FC0.80p. Company A’s year end is 31 December. The invoice was not paid by the year end date and exchange rate was CU1=FC0.85p. The invoice was paid on 30 January of the following year when the exchange rate was CU1=FC0.90p. The accounting treatment of this transaction is:

At date of transaction

|

|

CU |

CU |

|

Dr PPE (FC10,000/.80p) |

12,500 |

|

|

Cr Accounts Payable |

|

12,500 |

Being journal to recognise the purchase at the transaction date

At year end date

No foreign exchange adjustment is made as the asset is carried at the rate determined at the date of the transaction. It is not revalued to the year end rate. The creditor balance is retranslated at year end spot rate with the other side of the transition hitting the profit and loss.

At payment date

|

|

CU |

CU |

|

Dr Accounts Payable (being carrying amount at 31 December) |

CU11,765 |

|

|

Cr Bank (FC10,000/0.90p) |

|

CU11,111 |

|

Cr Foreign Exchange Gain in P&L |

|

654 |

Being journal to reflect foreign exchange gain on payment

Example 9: Retranslation of non-monetary asset – impairment of asset

Take example 8 above and assume an impairment review has been carried out on this asset at the end of year 1. The recoverable amount of the asset is determined to be FC7,000 retranslated to CU at the date of the impairment was CU9,333 (FX rate CU1=FC.75). The carrying amount at the same date in the balance sheet is CU8,000. As the recoverable amount is still in excess of the carrying amount no impairment is required.

Example 10: Net investment in a foreign operation

Parent A loaned CU100,000 to Sub A on 1 February (Sub A has a functional currency in FC) which is neither planned nor likely to occur in the foreseeable future, so the entity is regarded as a net investment in a foreign operation. The foreign exchange rate at the date of receipt by Sub A was FC1=CU1.20. The spot rate at 31 December is FC1=CU1.15 and the year end for both companies is 31 December. Assume the average rate in the year was FC1=CU1.17. The journals to be posted for FX are:

Sub A

|

|

FC |

FC |

|

Dr Bank |

83,333 |

|

|

Cr Amounts Due to Parent A (CU100,000/1.2) |

|

83,333 |

Being journal to reflect receipt of loan at transaction date

At year end

|

|

FC |

FC |

|

Dr FX Loss P&L |

3,623 |

|

|

Cr Amounts Due to Parent A ((CU100,000/1.15)=FC86,956-FC83,333) |

|

3,623 |

Being journal to reflect unrealised FX loss due to retranslation to year end rate

Parent A

No FX effect as it was issued in CU.

Consolidated accounts

|

|

CU |

CU |

|

Dr Unrealised FX in OCI |

4,239 |

|

|

Cr FX in Profit and Loss (FC3,623*1.17) |

|

4,239 |

Being journal to reclassify the FX loss from P&L to OCI assuming average rate for the year was used in the consolidation. This would then be recognised in a separate component in equity.

Example 11: Change in functional currency due to a change in circumstances

Company A carries out a software trade in Australia where its functional currency was CU. At the start of the year Company A was acquired by a US multinational software Group. Following acquisition, the US group using its synergies restructured the group whereby all of the cost of sales with regard to the software developments was recharged by the US parent in FC. This resulted in 85% of all costs being incurred in FC. The acquisition also resulted in the Company acquiring a significant portion of contracts with companies around the world all of these contracts were agreed in FC and received from customers in FC. 70% of all sales are now in FC. The company acquired FC loans from other group companies to allow it to expand.

From the above facts, it can be seen that the functional currency has changed to FC as the primary indicators now indicate that it is FC. If we assume for simplicity here that the functional currency changed on 1 January 2014 and the year end is 31 December 2014. Assume the year end FX rate at 1 January 2014 was CU1=FC1.20. The opening balance sheet would be retranslated as follows:

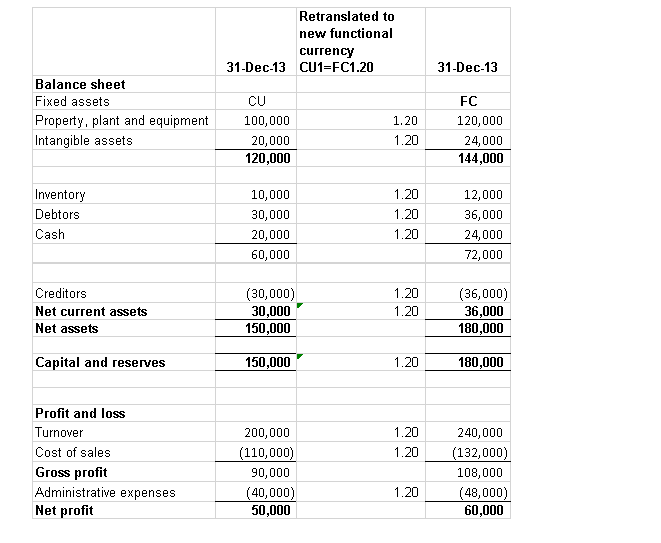

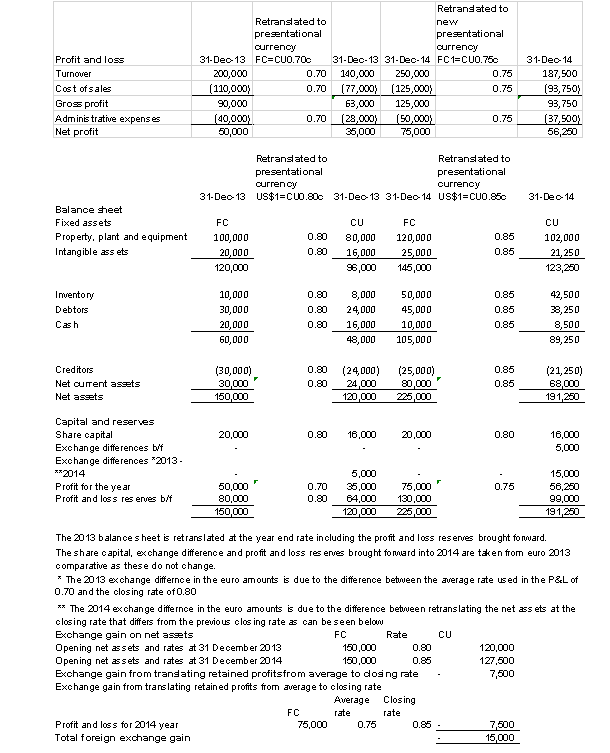

Example 12: Presentational currency

Company A has a functional currency of CU. It purchased a US company, Company B for FC200,000 on 1 January 2014. The fair value of the net assets at that date was FC150,000 with goodwill of FC50,000 being recognised. The spot rate at 31 December 2013 and 31 December 2014 was FC1=CU0.80c and USFC=CU0.85c. The average rate for the 31 December 2014 and 31 December 2013 year end is FC1=CU0.75c and FC1=CU0.70c respectively.

See below the work required to retranslate Company B’s financial statements from the functional currency of FC to the presentational currency of CU.

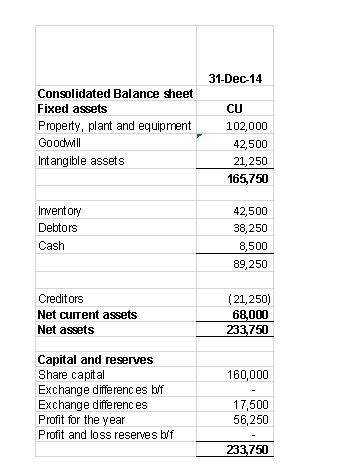

Example 13: Consolidation a foreign operations results

If we take example 12 above where we retranslated the subsidiaries FC functional accounts to a presentation currency of CU and now incorporate this into the consolidated financial statements of Company A. In accordance with Section 30.23 any goodwill arising on acquisition of Company B is treated as the assets and liabilities of the foreign operation. Therefore applying this to the example 12 where goodwill of FC50,000 was recognised. In the consolidated financial statements of Company A, this goodwill would have been recognised on 1 January 2014 at the rate on the date i.e. CU40,000 (FC50,000*0.8). The total consideration paid in CU was CU160,000 (FC200,000*0.8)

If we assume the parent company’s balance sheet is simple and only holds an investment in Company B with no costs or income. Then the parent entity balance sheet would look as follows:

| Financial assets | CU160,000 |

| Ordinary shares | CU160,000 |

In the consolidated financial statements goodwill would have to be restated as follows (excluding amortisation)

| Goodwill of FC50,000 retranslated at opening rate of CU1=USFC0.80 = | CU40,000 |

| Goodwill of FC50,000 retranslated at closing rate of CU1=USFC0.85 = | CU42,500 |

| Exchange gain to be added to goodwill & included in OCI | CU2,500 |

| Plus exchange difference posted on retranslation of Company B’s financials statements from USD to CU (see example 12 above) | CU15,000 |

| Total exchange gain difference posted to OCI in consolidated | CU17,500 |

Balance Sheet

Example 14: Contracted rate adjustment

The date of transition is 1 January 2014. Company A had forward contracts in place at 1 January 2014. The company makes sales in FC and CU. The functional currency of the company is CU. Under old GAAP as the entity was a non-FRS 26 adopter, the average forward contract rate of CU1=FC0.80 was used to retranslate the 31 December 2013 year end debtor and cash balances and the rate of CU1=FC0.78p at 31 December 2014. The actual year end spot rate at 1 January 2014 was CU1=FC0.75 and 31 December 2014 was CU1=FC0.82. Assume a deferred tax rate of 10%. Details of the value of the cash and debtor balances in FC are:

|

|

31/12/13 |

31/12/14 |

|

Debtors in Foreign Currency |

FC100,000 |

FC50,000 |

|

Cash in Foreign Currency |

FC70,000 |

FC80,000 |

|

Year-end Spot Rate |

CU1=FC0.75p |

CU1=FC0.82p |

|

Average Forward Rate Used |

CU1=FC0.80p |

CU1=FC0.79235 |

|

Debtors as Stated in Balance Sheet |

CU125,000 |

CU63,103 |

|

Cash as Stated in Balance Sheet |

CU87,500 |

CU102,564 |

|

Average Contracted Rate |

CU1=FC0.80p |

CU1=FC0.78p |

The following adjustments would be required:

On 1 January 2014

The carrying amount at 1 January using the year end spot rate as required by FRS 102 should have been:

Debtors – FC100,000/0.75p i.e. year end rate= CU133,333

Cash – FC70,000/0.75p i.e. year end rate= CU93,333

|

|

Debtors |

Cash |

|

Carrying Amount per the Balance Sheet |

CU125,000 |

CU87,500 |

|

Carry Amount at Spot Rate |

CU133,333 |

CU93,333 |

|

Difference – FX Gain |

CU8,333 |

CU5,833 |

Journals required

|

|

CU |

CU |

|

Dr Debtors |

8,333 |

|

|

Dr Cash |

5,833 |

|

|

Cr Profit and Loss Reserves for Foreign Exchange Gain |

|

14,166 |

Being journal to reflect adjustment required to show foreign currency balances at year end spot rate

|

|

CU |

CU |

|

Dr Profit and Loss Reserves for Deferred Tax (CU14,166*10%) |

1,417 |

|

|

Cr Deferred Tax in Balance Sheet |

|

1,417 |

Being journal to reflect deferred tax on the adjustment to reflect tax to be paid on this in the future

Journals required at 31 December 2014 assuming the above journals are posted to balance sheet and P&L reserves

The carrying amount at 31 December 2014 using the year end spot rate should have been:

Debtors – FC50,000/0.82p i.e. year end rate= CU60,975

Cash – FC80,000/0.82p i.e. year end rate= CU97,561

|

|

Debtors |

Cash |

|

Carrying amount per the balance sheet |

CU63,103 |

CU102,564 |

|

Carry amount at spot rate |

CU60,975 |

CU97,561 |

|

Difference – FX loss |

CU2,128 |

CU5,003 |

|

Journals required

|

CU |

CU |

|

Dr Foreign Exchange Loss in P&L |

7,131 |

|

|

Cr Debtors |

|

2,128 |

|

Cr Cash |

|

5,003 |

Being journal to reflect adjustment required to show foreign currency balances at year end spot rate

|

|

CU |

CU |

|

Dr Deferred Tax in Balance Sheet |

713 |

|

|

Cr Deferred Tax in P&L (CU7,131*10%) |

|

713 |

Being journal to reflect deferred tax on the adjustment to reflect the fact that tax was paid on this in the prior year and therefore a tax deduction will be obtained over the next 5 years under the tax transitional arrangements.

The journals posted for the 1 January 2014 will also have to be reversed into the profit and loss account as we have assumed these were posted in 31 December 2014 so as to show the correct opening reserves:

|

|

CU |

CU |

|

Dr Foreign Exchange Gain in P&L |

14,166 |

|

|

Cr Debtors |

|

8,333 |

|

Cr Cash |

|

5,833 |

Being journal to reflect reversal of prior year FX adjustment

|

|

CU |

CU |

|

Dr Deferred Tax in Balance Sheet |

1,417 |

|

|

Cr Deferred Tax in P&L (CU14,166*10%) |

|

1,417 |

Being journal to reflect reversal of prior year deferred tax on the adjustment above

Journals required in the year ended 31 December 2015 year end assuming the above journals are posted to reserves etc

|

|

CU |

CU |

|

Dr Debtors |

2,128 |

|

|

Dr Cash |

5,003 |

|

|

Cr FX gain in P&L |

|

7,131 |

Being journal to reverse the 2014 journals on the forward contract was closed out in the year.

|

|

CU |

CU |

|

Dr Deferred Tax in P&L |

143 |

|

|

(713/5 years) |

|

|

|

Cr Deferred Tax Asset |

|

143 |

Being journals to reflect the 1/5th release of the deferred tax asset recognised in 2014 to reflect the fact that a tax deduction will be claimed for CU1,426 (CU7,131/5 years) in the 2015 tax computation based on the assumption in this example that it will be reclaimed over a 5 year period. The remaining deferred tax will be released over the following four years as the tax deduction is claimed.

Example 15: Long term loan adjustment

The date of transition is 1 January 2014. Company A has a 100% investment in Company B. Company A loaned stgFC100,000 to Company B when the rate was CU1=0.80p. The terms of the loan was such that it was long term and it was not likely this loan would ever be repayable in the foreseeable future. Under old GAAP Company A treated this as a non-monetary asset as it was akin to an investment as a result this debtor balance was carried at its historical rate of CU125,000 (CU100,000/0.80). Under Section 30 although this balance would still meet the definition of an investment as it is akin to an investment (net investment in foreign entity) this balance is a non-monetary asset and therefore should be retranslated at the year end spot rate. The spot rate at 1 January 2014 and 31 December 2014 was CU1=FC0.75 and CU1=FC0.82 respectively. Assume the FX adjustment is taxable/tax deductible. Assume deferred tax of 10%. The journals to be posted on transition are:

1 January 2014

The carrying amount of the loan using the spot rate of CU1=FC0.75 under FRS 102 is = CU133,333 (FC100,000/0.75). Therefore the adjustment required is:

|

|

CU |

CU |

|

Dr Amounts Due from Company B (investment) (CU133,333-CU125,000) |

8,333 |

|

|

Cr Profit and Loss Reserves for Foreign Exchange Gain |

|

8,333 |

Being journal to reflect FC loan at the year end spot rate

|

|

CU |

CU |

|

Dr Profit and Loss Reserves for Deferred Tax (CU8,333*10%) |

833 |

|

|

Cr Deferred Tax Liability |

|

833 |

Being journal to reflect deferred tax as tax will be payable on this balance in the future

Journals required at 31 December 2014 assuming the above journals are posted in balance sheet and P&L side to reserves

The carrying amount of the loan using the spot rate of CU1=FC0.82 under FRS 102 is = CU121,951 (FC100,000/0.82). Therefore the adjustment required is:

|

|

CU |

CU |

|

Dr Foreign Exchange Loss in P&L |

3,049 |

|

|

Cr Amounts Due from Company B (investment) (CU121,951-CU125,000) |

|

3,049 |

Being journal to reflect FC loan at the year end spot rate

|

|

CU |

CU |

|

Dr Deferred Tax Asset |

305 |

|

|

Cr Deferred Tax in P&L (CU3,049*10%) |

|

305 |

Being journal to reflect deferred tax as tax will be payable on this balance in the future through adjustment to the tax computation for transition adjustments.

The journals posted for the 1 January 2014 will also have to be reversed into the profit and loss account as we have assumed these were posted in 31 December 2014 so as to show the correct opening reserves:

|

|

CU |

CU |

|

Dr Foreign Exchange Loss in P&L |

8,333 |

|

|

Cr Debtors |

|

8,333 |

Being journal to reflect reversal of prior year FX adjustment

|

|

CU |

CU |

|

Dr Deferred Tax Asset |

833 |

|

|

Cr Deferred Tax in P&L (CU8,333*10%) |

|

833 |

Being journal to reflect reversal of prior year deferred tax.

Journals required at 31 December 2015

The same type of journals will be required as was done in 2014 for 2015 excluding the deferred tax impact as this will be included in the 2015 tax computation. The deferred tax journal required is:

|

|

CU |

CU |

|

Dr Deferred Tax in P&L |

61 |

|

|

Cr Deferred Tax Asset |

|

61 |

|

(CU305/5 years) |

|

|

Being journal to reflect the 1/5th release of deferred tax to reflect the fact that a tax deduction will be claimed for CU610 (CU3,049/5 years) in the 2015 tax computation assuming it is a taxable adjustment in line with the tax transition revenue guidelines. The remaining deferred tax will be released over the following 4 years as the tax deduction is claimed in the tax computation. If the regulation in the disregard provisions were applied the full amount of the deferred tax of CU305 would be reversed in the 2015 year and deferred tax recognised at each year end from then on to reflect the movement.

Example 16: Foreign borrowings taken out to fund foreign investment

The date of transition is 1 January 2014. Company A (who has a CU functional currency) purchased a 100% UK subsidiary, Company B for FC100,000 retranslated to CU125,000 at 2 January 2014. Company A took out a FC loan of FC100,000 to fund the purchase of Company B. The spot rate of CU to FC at 31 December 2014 was CU1=FC0.75. Assume deferred tax of 10% and the carrying amount of the FC loan at the end of 2014 was FC90,000. Under old GAAP the company was allowed to retranslate the investment of FC100,000 at the year end rate as it met the conditions as it had taken out foreign borrowings specifically to fund this investment. Therefore under old GAAP the FX movement on the investment was set against the FX gain/loss on the FC loan. As a result of this treatment the carrying amount of the investment in old GAAP books at 31/12/14 was CU133,333 (FC100,000/0.75). Assume this adjustment was taxed/tax deductible in the prior year for the purpose of this example.

Section 30 does not allow the treatment adopted under old GAAP as it does not meet the requirements for a fair value hedge under Section 12. As a result the investment cannot be retranslated at the year end rate, instead it must remain at historical cost. The journals required on transition are:

At 31 December 2014

Under old GAAP the journal posted was to Dr investment CU8,333 (CU133,333-CU125,000 being the historic cost) and Cr foreign exchange gain in P&L or OCI for CU8,333. Under FRS 102 this treatment is not allowed so this journal would have to be reversed such that the investment remains to be shown at CU125,000 being the original historic cost. The journal required is:

|

|

CU |

CU |

|

Dr Foreign Exchange Gain/OCI |

8,333 |

|

|

Cr Investment in Company B |

|

8,333 |

Being journal to reverse previous posting under old GAAP.

|

|

CU |

CU |

|

Dr Deferred Tax Asset |

833 |

|

|

Cr Deferred Tax in P&L (CU8,333*10%) |

|

833 |

Being journal to reflect deferred tax for tax paid in 2014 now being repayable assuming it was taxable initially.

This deferred tax will be released over a 5 year period from 2015 in line with the tax transition guidance. The journal required in 2015 is

|

|

CU |

CU |

|

Dr Deferred Tax in P&L |

167 |

|

|

Cr Deferred Tax Asset (CU833/5 years) |

|

167 |

Being journal to reflect the release of deferred tax to reflect the fact that a tax deduction will be claimed for CU1,667 (CU8,333/5 years) in the 2015 tax computation assuming it is a tax deductible amount.

If in the above example this adjustment was not taxed/deducted in the prior year tax computations there would be no deferred tax or current tax implication.

Note a journal would be required to be posted to retained earnings on transition if an entity has treated an investment in the above way under old GAAP. For simplicity in the example above we have assumed an investment was acquired post the transition date.

Example 17: Goodwill on foreign operations to be retranslated at the closing rate

The transition date to FRS 102 is 1 January 2014. Parent A (who has a CU functional currency) purchased a 100% interest in a US Company, Company B at 1 January 2013 for FC200,000. At that time the fair value of the net assets was FC150,000 which equaled the net assets at the time and goodwill of FC50,000 was recognised on acquisition. Goodwill of CU40,000 (FC50,000/0.80) was recognised at the date of acquisition and was not subsequently retranslated in the consolidated financial statements under old GAAP. The goodwill is amortised over 10 years and the NBV of goodwill under old GAAP at 1 January 2014, 31 December 2014 and 31 December 2015 was CU36,000, CU32,000 and CU28,000 respectively. The year end FX rate at 1 January 2014, 31 December 2014 and 31 December 2015 is FC1=CU0.85, FC1=CU0.87 and FC1=CU0.90.

Under Section 30.23 any goodwill or fair value adjustments recognised in the consolidated financial statements should be retranslated at each year end date. The journal adjustments required on transition are:

On 1 January 2014

Carrying amount of goodwill in FC at 1 January = FC50,000/10yrs*9yrs= FC45,000 retranslated at the year end rate of FC1=CU0.85 = CU38,250

Therefore adjustment required is the difference between the carrying amount under old GAAP of CU36,000 less the carrying amount retranslated at the year end rate of CU38,250. The journals required to be posted in the consolidated accounts is therefore:

|

|

CU |

CU |

|

Dr Goodwill (CU38,250-CU36,000) |

2,250 |

|

|

Cr Profit and Loss Reserves |

|

2,250 |

Being journal to reflect foreign goodwill retranslated at year end rate

Journals required for year ended 31 December 2014 assuming the above journals are posted to reserves etc

Carrying amount of goodwill in FC at 31 December 2014 = FC50,000/10yrs*8yrs= FC40,000 retranslated at the year end rate of FC1=CU0.87 = CU34,800

Therefore adjustment required is the difference between the carrying amount under old GAAP of CU32,000 less the carrying amount retranslated at the year end rate of CU34,800. The journals required to be posted in the consolidated accounts is therefore:

|

|

CU |

CU |

|

Dr Goodwill (CU34,800-CU32,000) |

2,800 |

|

|

Cr Other Comprehensive Income |

|

2,800 |

Being journal to reflect foreign goodwill retranslated at year end rate

A journal is also required to reverse the adjustment posted into the opening balance sheet as this is no longer required such that the true movement in the FX rate is shown in other comprehensive income.

|

|

CU |

CU |

|

Dr other comprehensive income |

2,250 |

|

|

Cr goodwill |

|

2,250 |

Being journal to reflect reversal of prior year goodwill journal

Journals required for year ended 31 December 2015 assuming the above journals are posted to reserves etc

The journals required for 2015 will be similar to the 2014 journals.

Example 18 – Extract from notes to the accounting policies

The company has chosen to present the financial statement in a currency that differs from its functional currency so that it can be easily consolidated into the parent company’s financial statements. The functional currency of the company is XXXX

Extract from the financial statements – operating profit note

OPERATING PROFIT

Operating profit is stated after charging/(crediting):

|

|

2015 |

|

2014 |

|

|

CU |

|

CU |

|

Depreciation |

149,999 |

|

170,037 |

|

Directors’ remuneration: |

212,000 |

|

225,600 |

|

Impairment of goodwill (included within administrative expenses) |

– |

|

– |

|

Foreign exchange gain/loss |

– |

|

– |

|

Impairment of investment in subsidiary/associate/joint venture |

– |

|

– |

|

Reversal of impairment of property, plant and equipment (included within administrative expenses) See note 1 |

– |

|

– |

|

Reversal of impairment of goodwill/intangibles (included within administrative expenses) |

– |

|

– |

|

Reversal of impairment of inventory (included within cost of sales) |

– |

|

– |

|

Impairment of inventory (included within cost of sales) |

– |

|

– |

|

Inventory recognised as an expense |

– |

|

– |

|

Auditors’ remuneration |

|

|

|

|

Audit |

13,000 |

|

13,000 |

|

Non audit services |

3,000 |

|

3,000 |

|

Tax Advisory |

3,225 |

|

3,225 |

Extract from other comprehensive income showing foreign exchange differences on retranslation

Consolidated Statement of Comprehensive Income

|

Profit for the financial year |

1,000,000 |

500,000 |

|

Cash flow hedges |

|

|

|

– effective portion of changes in fair value to cash flow hedges |

9 XXX |

XXX |

|

– fair value of cash flow hedges transferred to income statement |

10 XXX |

XXX |

|

Actuarial loss in respect of the defined pension scheme |

11 (XXX) |

(XXX) |

|

Exchange differences on retranslation of subsidiary undertakings |

XXX |

(XXX) |

|

Gain/(loss) on revaluation of intangible assets |

12 XXX |

(XXX) |

|

Gain/(loss) on revaluation of property, plant and equipment |

13 XXX |

(XXX) |

|

Gain/(loss) on revaluation of subsidiaries, associates, etc. |

14 XXX |

(XXX) |

|

Deferred tax on components of other comprehensive income |

15 XXX |

XXX |

|

|

|

|

|

Total other comprehensive income for the year net of tax |

200,000 |

(100,000) |

|

|

|

|

|

Total comprehensive income for the year |

1,200,000 |

400,000 |

|

Total comprehensive income for the financial year attributable to: |

|

|

|

Owners of the parent company |

XXX |

XXX |

|

|

1,200,000 |

400,000 |

Example 19: Example of a change of functional currency due a change in circumstance i.e. adjusted prospectively

|

Change in functional currency |

|

|

|

The company changed functional currency from FC (“FC”) to United States Dollar (“USFC”) on 31 December 2014. This change arose as a result of the acquisition of the company by a larger group. As a result a change was made to the cost and funding structure such that the primary economic environment in which the company operates resulted in a change in functional currency to USFC. |

||

|

– All resulting exchange differences were recognised as a separate component of equity, described as the exchange rate reserve. |

||

|

|

Restated |

|

|

|

2014 |

2014 |

|

|

USFC |

FC |

|

|

|

|

|

Turnover |

237,601 |

146,134 |

|

|

|

|

|

Cost of sales |

(220,264) |

(135,471) |

|

|

|

|

|

|

|

|

|

Gross profit |

17,337 |

10,663 |

|

|

|

|

|

Administrative expenses |

(16,066) |

(9,882) |

|

Other operating income |

– |

– |

|

|

|

|

|

Operating profit |

1,270 |

781 |

|

|

|

|

|

Interest receivable |

– |

– |

|

Interest payable and similar charges |

(355) |

(218) |

|

|

|

|

|

|

|

|

|

Profit on ordinary activities before taxation |

916 |

563 |

|

|

|

|

|

Tax on profit |

(416) |

(256) |

|

|

|

|

|

|

|

|

|

Profit / (loss) for the financial period after taxation |

499 |

307 |

|

Balance sheet |

Restated |

|

|

2014 |

2014 |

|

|

USFC |

FC |

|

|

Fixed assets |

||

|

Tangible assets |

5,637 |

3,483 |

|

Investments |

8,810 |

5,443 |

|

|

|

|

|

14,447 |

8,927 |

|

|

Current assets |

||

|

Debtors |

387,831 |

239,641 |

|

Cash at bank and in hand |

32,999 |

20,390 |

|

|

|

|

|

420,831 |

260,031 |

|

|

Creditors: amounts falling due within one year |

(255,617) |

(157,946) |

|

|

|

|

|

Net current assets |

165,214 |

102,086 |

|

Creditors: amounts falling due after more than one year |

(5,273) |

(3,258) |

|

Provision for liabilities |

(1,900) |

(1,174) |

|

|

|

|

|

Net assets |

172,488 |

106,581 |

|

Capital and reserves |

||

|

Called-up share capital |

6 |

3 |

|

Other reserve |

64,548 |

39,884 |

|

Profit and loss account |

107,935 |

66,693 |

|

|

|

|

|

Equity shareholder’s funds |

172,488 |

106,581 |

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]