[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-30/” type=”big” color=”red”] Return to Section 30 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Change in functional currency

Extract from FRS102: Section 30.14 -30.16

30.14 When there is a change in an entity’s functional currency, the entity shall apply the translation procedures applicable to the new functional currency prospectively from the date of the change.

30.15 As noted in paragraphs 30.2 to 30.5, the functional currency of an entity reflects the underlying transactions, events and conditions that are relevant to the entity. Accordingly, once the functional currency is determined, it can be changed only if there is a change to those underlying transactions, events and conditions. For example, a change in the currency that mainly influences the sales prices of goods and services may lead to a change in an entity’s functional currency.

30.16 The effect of a change in functional currency is accounted for prospectively. In other words, an entity translates all items into the new functional currency using the exchange rate at the date of the change. The resulting translated amounts for non-monetary items are treated as their historical cost.

OmniPro comment

Section 30.14 above states that a change in functional currency is adjusted prospectively. However where the functional currency was wrong due to an error then it would have to be adjusted retrospectively under Section 10. An example of such a retrospective adjustment has not been shown in this manual, however disclosures have been included. If this were the case, then a detailed exercise would need to be performed to identify the historical costs of the non-monetary assets and equity so that the asset can be retranslated at that date of the transaction. This would be a very time consuming exercise for an entity.

For a change in functional currency due to a change in circumstances both the profit and loss and balance sheet in the prior year comparatives are restated at the foreign exchange rate at the date of the change in functional currency.

See example below for application of the guidance in Section 30.14 to 30.16. Note where the change occurs at the start of a financial year, the prior year profit and loss would be translated at the average exchange rate so as to allow comparability. An example of a disclosure is included in the disclosure section below.

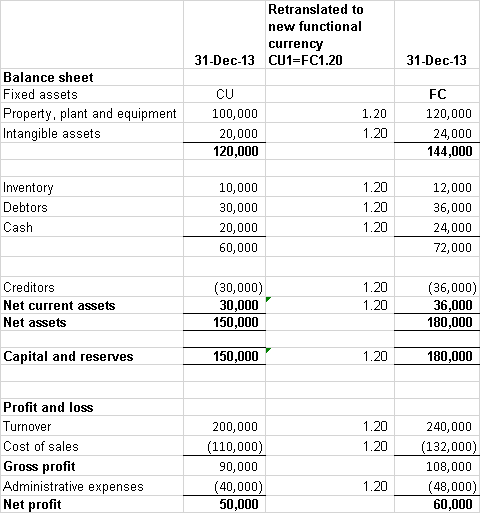

Example 11: Change in functional currency due to a change in circumstances

Company A carries out a software trade in Australia where its functional currency was CU. At the start of the year Company A was acquired by a US multinational software Group. Following acquisition, the US group using its synergies restructured the group whereby all of the cost of sales with regard to the software developments was recharged by the US parent in FC. This resulted in 85% of all costs being incurred in FC. The acquisition also resulted in the Company acquiring a significant portion of contracts with companies around the world all of these contracts were agreed in FC and received from customers in FC. 70% of all sales are now in FC. The company acquired FC loans from other group companies to allow it to expand.

From the above facts, it can be seen that the functional currency has changed to FC as the primary indicators now indicate that it is FC. If we assume for simplicity here that the functional currency changed on 1 January 2014 and the year end is 31 December 2014. Assume the year end FX rate at 1 January 2014 was CU1=FC1.20. The opening balance sheet would be retranslated as follows:

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]