[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

22.1.1 Extract from FRS 102 – Section 22.1-22.2.

22.2 Classification of an instrument as liability or equity.

22.2.1 Extract from FRS 102 – Section 22.3.

22.2.2.1 Definition of financial liability.

22.2.2.2 Definition of equity.

22.2.3 Accounting treatment of instruments classified as debt

22.2.5 Treatment of dividend on instruments classified as equity.

22.2.6 Examples illustrating whether an instrument meets the definition of debt or equity.

22.2.6.1 Redeemable preference shares at option of the holder with mandatory coupon.

22.2.6.2 Non-redeemable preference shares with mandatory coupon at market rate.

22.2.6.4 Shares/loan notes redeemable at the option of the holder

22.2.6.5 Non-redeemable preference shares with discretionary dividend.

22.2.6.6 Redeemable preference shares at option of issuer with discretionary dividend.

22.2.6.7 Redeemable preference shares at option of issuer with mandatory.

22.2.6.9.1 Treatment of difference between present value ad actual amount subscribed for

22.2.6.13 Fixed for fixed arrangement

22.2.6.14 Equity issued in return for a forward contract to issue foreign currency.

22.3.2.2 Contingency element is not genuine.

22.3.2.3 contingency occurring on liquidation.

22.3.2.5 Examples of uncertain future/changed events outside the control of the issuer

22.3.2.6 Example of instruments to be classified as a debt or equity.

22.4 Original issue of shares or other equity instruments.

22.4.1 Extract from FRS 102 – Section 22.7-22.10.

22.4.2 OmniPro comment – Accounting treatment

22.4.2.4 Examples of share issues – accounting treatment

22.5 Exercise of options, rights and warrants.

22.5.1 Extract from FRS 102 – Section 22.11.

22.6 Capitalisation or bonus issues of shares and share splits.

22.6.1 Extract from FRS 102 – Section 22.12.

22.7.1 Extract from FRS 102 – Section 22.13-22.15.

22.7.2.1 Determining the split of debt and equity.

22.7.2.2 Treatment of transaction cost

22.7.2.3 Subsequent revisions.

22.7.2.4 Accounting for the liability.

22.7.2.5 Examples of compound financial instruments.

22.7.2.6 Compound Financial instrument example.

22.7.2.7 Accounting for the convertible option once exercised or option to exercise is not taken.

22.7.2.8 Allocation of transaction costs.

22.8.1 Extract from FRS 102 – Section 22.17-22.18.

22.8.2.1 Distribution of shares classified in equity.

22.8.2.2 Distributions on shares classified as debt (i.e. On shares classified on debt)

22.8.2.3 Disclosure of fair value of non-cash distributions.

22.9 Non-controlling interest and transactions in shares of a consolidated subsidiary.

22.9.1 Extract from FRS 102 – Section 22.19.

22.9.2.2 Accounting for acquiring a further controlling interest

22.9.2.3 Accounting for disposals of controlling interests but controlling interest retained.

22.10.1.1 Statement of changes in equity.

22.10.1.2 Accounting Policies.

22.10.1.3 Note to the financial statements.

22.10.1.4 Notes in relation to dividends

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.0.101″]

22.7 Convertible debt or similar compound financial instruments

22.7.1 Extract from FRS 102 – Section 22.13-22.15

22.13 On issuing convertible debt or similar compound financial instruments that contain both a liability and an equity component, an entity shall allocate the proceeds between the liability component and the equity component. To make the allocation, the entity shall first determine the amount of the liability component as the fair value of a similar liability that does not have a conversion feature or similar associated equity component. The entity shall allocate the residual amount as the equity component. Transaction costs shall be allocated between the debt component and the equity component on the basis of their relative fair values.

22.14 The entity shall not revise the allocation in a subsequent period.

22.15 In periods after the instruments were issued, the entity shall account for the liability component as a financial instrument in accordance with Section 11 Basic Financial Instruments or Section 12 Other Financial Instruments Issues as appropriate. The appendix to this section illustrates the issuer’s accounting for convertible debt where the liability component is a basic financial instrument.

22.7.2 OmniPro comment

22.7.2.1 Determining the split of debt and equity

A compound instrument is an instrument that contains both an equity and debt component.

In accordance with section 22.13 of FRS 102 the liability element is determined first by applying the market rate of interest to the proceeds in order to get the present value (assuming the option was not incorporated into the instrument) The difference between the present value and the proceeds is determined to be the equity element.

22.7.2.2 Treatment of transaction cost

Any transaction costs are allocated between debt and equity based on relative fair values. See example of same at 22.7.2.8.

22.7.2.3 Subsequent revisions

An equity is not permitted to revise the slit of debt and equity in subsequent periods as stated in section 22.14 of FRS 102.

22.7.2.4 Accounting for the liability component

Section 22.15 of FRS 102 requires the debt component to be accounted for in line with section 11 of FRS 102 (for basic financial instruments – see 11.5.2 and 11.6.1.1 for further details) or section 12 of FRS 102 for complex financial instruments.

22.7.2.5 Examples of compound financial instruments.

Examples of compound instruments are:

- Preference shares/bonds convertible with a mandatory coupon redeemable at the option at the holder, into a fixed number of ordinary shares at any time up to maturity (see example 17 and 18 at 22.7.2.6 and 22.7.2.7).

- Non redeemable preference shares issued at non-market rate with mandatory coupon. See example 3 at 22.2.6.3.

- Mandatory redeemable preference shares/bonds at fixed amount at a fixed or future date with dividend payable at the discretion of the issuer. See example 9 at 22.2.6.9.

- Redeemable preference shares/bonds at holder’s option at some future date with dividend payable at the discretion of the issuer. See example 10 at 22.2.6.10.

22.7.2.6 Compound Financial instrument example

See the example provided in Appendix to Section 22 in the FRS below which illustrates Section’s 22.14-22.15 of FRS 102. This refers to bonds but the word ‘bond’ can be replaced with preference shares:

Example 17: Accounting treatment for a compound financial instrument (instrument containing both a debt and equity component – bond with a fixed coupon and convertible at the option of the holder into a variable number of shares (Extracted from the appendix of Section 22 of FRS 102)

On 1 January 20X5 an entity issues 500 convertible bonds. The bonds are issued at par with a face value of CU100 per bond and are for a five-year term, with no transaction costs. The total proceeds from the issue are CU50,000. Interest is payable annually in arrears at an annual interest rate of 4 per cent. Each bond is convertible, at the holder’s discretion, into 25 ordinary shares at any time up to maturity. At the time the bonds are issued, the market interest rate for similar debt that does not have the conversion option is 6 per cent.

Here the liability component is the interest liability on the bond and the principal to be repaid. The equity component being the holder’s option to convert the bonds into a fixed number of equity shares.

When the instrument is issued, the liability component must be valued first, and the difference between the total proceeds on issue (which is the fair value of the instrument in its entirety) and the fair value of the liability component is assigned to the equity component. The fair value of the liability component is calculated by determining its present value using the discount rate of 6 per cent. The calculations and journal entries are illustrated below:

| CU | |

| Proceeds from the bond issue (A) | 50.000 |

| Present value of principal at the end of five years (see calculations in note 1 below) | 37,363 |

| Present value of interest payable annually in arrears for five years (see calculations in note 1 below) | 8,425 |

| Present value liability, which is the fair value of liability component (B) (see calculations in note 1 below) | 45,788 |

| Residual, which is the fair value of the equity component (A) – (B) | 4,212 |

The issuer of the bonds makes the following journal entry at issue on 1 January 20X5:

| CU | CU | |

| Dr Cash | 50,000 | |

| Cr Financial Liability – Convertible Bond | 45,788 | |

| Cr Equity | 4,212 |

The CU4,212 represents a discount on issue of the bonds, so the entry could also be shown ‘gross’:

| CU | CU | |

| Dr Cash | 50,000 | |

| Dr Financial Liability – Convertible Bond Discount | 4,212 | |

| Cr Financial Liability – Convertible Bond | 50,000 | |

| Cr Equity | 4,212 |

After issue, the issuer will amortise the bond discount according to the following table

| (a) Interest payment

CU |

(b) Total Interest expense = 6% x(e)

CU |

Amortisation of bond discount =

(b) – (a) CU |

(d) Bond discount =

(d) – (c) CU |

(e) Net liability = 50,000 – (d)

CU |

|

| 1/1/20X5 | 4,212 | 45,788 | |||

| 31/12/20X5 | 2,000 | 2,747 | 747 | 3,465 | 46,535 |

| 31/12/20X6 | 2,000 | 2,792 | 792 | 2,673 | 47,327 |

| 31/12/20X7 | 2,000 | 2,840 | 840 | 1,833 | 48,167 |

| 31/12/20X8 | 2,000 | 2,890 | 890 | 943 | 49,057 |

| 31/12/20X9 | 2,000 | 2,943 | 943 | 0 | 50,000 |

| Totals | 10,000 | 14,212 | 4,212 |

At the end of 20X5, the issuer would make the following journal entry:

| CU | CU | |

| Dr Interest Expense | 2,747 | |

| Cr Bond Discount | 747 | |

| Cr Cash | 2000 |

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 1: Redeemable preference shares at option of the holder with mandatory coupon.

Example 2: Non-redeemable preference shares with mandatory coupon at market rate.

Example 4: Shares redeemable at the option of the holder

Example 5: Non-redeemable preference shares with discretionary dividend.

Example 6: Redeemable preference shares at option of issuer with discretionary dividend.

Example 7: Redeemable preference shares at option of issuer with mandatory dividend.

Example 13: Fixed for fixed arrangement

Example 13A: Application of Section 22.3(b)(ii) of FRS 102.

Example 13B: Future contingency amount

Example 13C: Future contingency.

Example 14: Accounting treatment on original issue of shares.

Example 15: Accounting treatment on original issue of shares – left as unpaid.

Example 16: Capitalisation/bonus issue.

Example 17: Accounting treatment for a compound financial instrument

Example 18: compound instrument where conversion is chosen.

Example 19: compound instrument where conversion is chosen.

Example 20: Accounting for transaction costs in acquiring a compound financial instrument

Example 21: Acquiring a further controlling interest

Example 22: Acquiring a further controlling interest

Example 23: Disposing of controlling interest but controlling interest retained.

Example 24: Extract of Statement of Changes in Equity from financial statements.

Example 25: Extract from accounting policies note.

Example 26: Extract from notes to the financial statements – liability

Example 27: Extract from notes to the financial statements – share capital

Example 28: Extract from notes to the financial statements – dividends on equity shares.

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text _builder_version=”3.0.101″ background_layout=”light”]

Note 1: Calculations

Present value of principal of CU50,000 at 6 per cent

CU50,000/(1.06)^5 = CU37,363

The CU2,000 annual interest payments are an annuity: a cash flow stream with a limited number (n) of periodic payments (C), receivable at dates 1 to n. To calculate the present value of this annuity, future payments are discounted by the periodic rate of interest (i) using the following formula:

PV = C/i * [1 – 1/(1+i)n]Therefore, the present value of the CU2,000 interest payments is (CU2,000/.06) * [1 – [(1/1.06)5] = CU8,425

This is equivalent to the sum of the present values of the five individual CU2,000 payments, as follows:

| CU | |

| Present value of interest payment at 31 December 20X5 = 2,000/1.06 | 1,887 |

| Present value of interest payment at 31 December 20X6 = 2,000/1.062 | 1,780 |

| Present value of interest payment at 31 December 20X7 = 2000/1.063 | 1,679 |

| Present value of interest payment at 31 December 20X8 = 2000/1.064 | 1,584 |

| Present value of interest payment at 31 December 20X9 = 2000/1.065 | 1,495 |

| Total | 8,425 |

Yet another way to calculate this is to use a table of present value of an ordinary annuity in arrears, five periods, interest rate of 6 per cent per period. (Such tables are easily found on the Internet.) The present value factor is 4.2124. Multiplying this by the annuity payment of CU2,000 determines the present value of CU8,425.

22.7.2.7 Accounting for the convertible option once exercised or option to exercise is not taken.

Section 22 provides no guidance on how to account for the convertible option once it is exercised. In accordance with Section 10, one can look to IAS 32 for guidance in this regard. See the accounting treatment for same in example 18 below. If the option is not exercised, there is no changes to be made. See example 19 below.

Example 18: compound instrument where conversion is chosen

If we take example 17, and now assume at the end of 5 years, the convertible bond/preference shares are converted into 12,500 shares (i.e. CU50,000/CU100 per bond * 25 shares per bond). Assume the fair value of the shares issued at that date was CU4.50. The journal entries required to account for this is to:

| CU | CU | |

| Dr Liability | 50,000 | |

| Cr Equity | 50,000 |

NOTE: the original component stays in equity but can be transferred within equity. No gain or loss is ever recognised on conversion as no money changes hands.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text _builder_version=”3.0.101″ background_layout=”light”]

Example 19: compound instrument where conversion is chosen

If we take example 17 above and assume the conversion option was not taken. The journal required is:

| CU | CU | |

| Dr Liability | 50,000 | |

| Cr Bank | 50,000 |

The original equity component remains as equity. It may be transferred within equity for classification purposes.

22.7.2.8 Allocation of transaction costs.

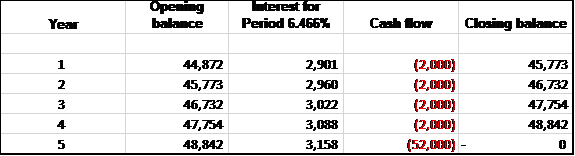

Example 20: Accounting for transaction costs in acquiring a compound financial instrument

If we take example 17 above and assume transaction costs of CU1,000 were incurred. In accordance with Section 22 these transaction costs should be apportioned between the debt and equity element of the instrument in proportion to the split determined. For example this CU1,000 would be split as follows in example 17:

Element of cost to be allocated to debt CU1,000* CU45,788 = CU916

CU50,000

Element of cost to be allocated to equity CU1,000* CU4,212 = CU84

CU50,000

The CU916 is netted against the CU45,788 on initial recognition of the financial liability (CU44,872). The effective rate of interest is then obtained which accumulates the net CU44,872 to CU50,000 by the end of year 5. Through trial and error, the effective rate of interest is 6.466%

The same type of journals that were posted in example 17 would be posted here for the updated figures above.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][/et_pb_column][/et_pb_row][/et_pb_section]