[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-19/” type=”big” color=”red”] Return to Section 19 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Purchase method – steps

Extracts from FRS102 – Section 19.6-19.7

19.6 All business combinations shall be accounted for by applying the purchase method, except for:

(a) group reconstructions which may be accounted for by using the merger accounting method (see paragraphs 19.27 to 19.33); and

(b) public benefit entity combinations that are in substance a gift or that are a merger which shall be accounted for in accordance with Section 34 Specialised Activities.

19.7 Applying the purchase method involves the following steps:

(a) identifying an acquirer;

(b) measuring the cost of the business combination; and

(c) allocating, at the acquisition date, the cost of the business combination to the assets acquired and liabilities and provisions for contingent liabilities assumed.

OmniPro comment

Group reconstructions do not have to come within the remit of the purchase method instead these are accounted for under the merger method which is discussed further below within Section 19 of this website.

Purchase method – Identifying the acquirer

Extracts from FRS102 – Section 19.8 – 19.10 and 19.17

19.8 An acquirer shall be identified for all business combinations accounted for by applying the purchase method. The acquirer is the combining entity that obtains control of the other combining entities or businesses.

19.9 Control is the power to govern the financial and operating policies of an entity or business so as to obtain benefits from its activities. Control of one entity by another is described in Section 9 Consolidated and Separate Financial Statements.

19.10 Although it may sometimes be difficult to identify an acquirer, there are usually indications that one exists. For example:

(a) If the fair value of one of the combining entities is significantly greater than that of the other combining entity, the entity with the greater fair value is likely to be the acquirer.

(b) If the business combination is effected through an exchange of voting ordinary equity instruments for cash or other assets, the entity giving up cash or other assets is likely to be the acquirer.

(c) If the business combination results in the management of one of the combining entities being able to dominate the selection of the management team of the resulting combined entity, the entity whose management is able so to dominate is likely to be the acquirer.

19.17 Application of the purchase method starts from the acquisition date, which is the date on which the acquirer obtains control of the acquiree. Because control is the power to govern the financial and operating policies of an entity or business so as to obtain benefits from its activities, it is not necessary for a transaction to be closed or finalized at law before the acquirer obtains control. All pertinent facts and circumstances surrounding a business combination shall be considered in assessing when the acquirer has obtained control.

OmniPro comment

The acquirer is the combining entity that obtains control of the other combining entities or businesses.

As stated above control is presumed where greater than 50% of the voting power is held by an entity. However control can also exist as detailed in Section 9.5 of FRS 102 when the parent owns 50% or less of the voting power but it has:

- power over more than half of the voting rights by virture of an agreement with other investors; or

- power to govern the financial and operating policies of the entity under a statute or an agreement; or

- power to appoint or remove the majority of members of the board of directors or equivalent; or

- power to cast the majority of votes at meetings of the board of directors.

- having options or convertible instruments which are exercisable at the date of acquisition.

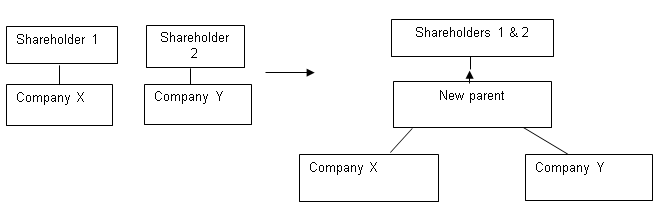

There are occasions where a new entity is formed to issue equity instruments to effect a business combination between two other entities. Although not specifically dealt with in Section 19, IFRS 3 requires that one of the combining entities that existed before the combination be identified as the acquirer. Therefore, the new parent would only account for this under merger accounting and one of the combining entities would account for the transaction as a business combination.

This approach would be appropriate under FRS 102. The basis for this is that the transaction has little or no substance and it was not at an arm’s length basis. See the example below which illustrates this.

[/et_pb_text][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Example 3: Acquiring company

The shareholders of Company X and Y agree to join together under the same group. A new company, Company C is set up with Shareholder 1 and 2 as the owners. A transaction is entered into whereby Company A issues shares to each of its directors in proportion to the fair value of Company X & Y. Assume shares issued to Company X obtained 200 shares and Company Y was issued 100 shares. In this case Company C is not deemed to be the acquirer instead Company X is the acquirer as the fair value of Company X is well in excess of Company Y.

Company X would use the purchase accounting method to account for the acquisition. Company Y would use merger accounting.

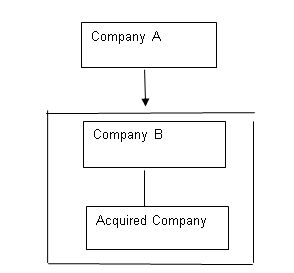

However where an entity sets up a 100% subsidiary and provides funds to this new company to invest in another entity/business combination and the transaction is performed on an arm’s length basis, the acquirer would be the new company. Here there was no issue of shares to the combining entities. In reality as it is an intermediate parent, it may be exempt from preparing consolidated financial statements.

Example 4: Identifying the acquirer

Company A set up a new Company as a 100% subsidiary, Company B with the sole purpose to acquire a business/shares of another entity. Company A provides the funds to Company B to allow it to acquire the business and charges market interest. In this case the acquirer of the business is Company B and not Company A.

[/et_pb_text][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Although not mentioned in Section 19.7 another key thing to identify when applying the purchase accounting method is to identify the acquisition date. The acquisition date is the date from which the acquired entities results are consolidated with the acquirers results and the date on which fair value of assets are determined. The acquisition date is the date when the acquirer obtains control over the acquiree. Section 19.9 defines control as the power to govern the financial and operating policies of an entity or business so as to obtain benefits from its activities.

There is a presumption that control has been obtained where an entity owns greater than 50% of the voting rights of a company. However it is also possible to obtain control where less than this is owned, for example an entity might have the right to appoint and remove parties from the board of directors.

The key date when ascertaining when control is obtained is when the offer to purchase is unconditional and when the directors of the acquiring entity are appointed to the board. For example where a takeover is subject to competition authority approval control is unlikely to pass until the approval is obtained, hence the date of acquisition will be the date approval is obtained. The date on the purchase agreement is not the key date as this may not be the date the control is transferred. The key date is the date the acquirer nominates its directors, it does not necessarily have to correspond to the date the shares are transferred.

Purchase method – Cost of a business combination

Extracts from FRS102 – Section 19.11-19.11A

19.11 The acquirer shall measure the cost of a business combination as the aggregate of:

(a) the fair values, at the acquisition date, of assets given, liabilities incurred or assumed, and equity instruments issued by the acquirer, in exchange for control of the acquiree; plus

(b) any costs directly attributable to the business combination.

19.11A Where control is achieved following a series of transactions, the cost of the business combination is the aggregate of the fair values of the assets given, liabilities assumed and equity instruments issued by the acquirer at the date of each transaction in the series.

OmniPro comment

Where cash is paid for the business, the cost of the business combination is effectively the cash price paid being its fair value.

Where payment is deferred and it is for greater than one year the present value of the amount to be paid is the cost of the business combination.

The calculation of deferred consideration is considered further below.

Consideration paid could also include group loans or borrowings taken over in the acquired entity. Future losses expected to be incurred are not considered to be liabilities incurred.

Costs directly attributable to the acquisition

Cost that would be considered to be directly attributable to the business combination (costs that have to be incurred to effect the business) would include:

- professional fees paid to accountants, legal advisors, valuers and other consultants to effect the combination

- Cost of paying a third party to investigate or assist in identifying a potential target but only if the fee is payable on condition that the combination takes place.

- Cost for auditing the completion accounts and undertaking due diligence work

Example of costs which would not be considered to be directly attributable to the business combination are:

- Incremental costs that are attributable towards the cost of obtaining finance to purchase the combination e.g. costs directly attributable to financial liabilities or cost associated with the issue of equity instruments.

- Costs charged by professional advisors in order to allow the entity to obtain finance or issue shares

- General administrative costs e.g. staff costs of the acquirer’s regardless of their position and regardless of how long they have worked on it

- Overhead costs

Equity issued as consideration for the acquisition

Where equity instruments issued by the acquirer are given as consideration for the business combination, then the equity instruments have to be fair valued.

The fair value exercise should follow the requirement of Section 11 when determining fair value i.e. in reality a listed share price will not be available so a discounted cash flow or option pricing model will have to be used. These discounted cash flows should use market information when determining the valuation and very little internal information. Where the variability of various valuation techniques is not significant, or the probabilities of the various estimates within the range can be reasonably assessed and used in estimating fair value, the valuation of the equity instrument is likely to be reliable.

Cost where control achieved in stages

Where a Company initial acquires an investment which gives a significant interest or just a partial interest and subsequently acquires a further interest such that control is obtained, the cost of the combination will be the total cost i.e. the cost of the transaction which resulted in the control being obtained plus the previous cost.

Example 5: Determining cost where control achieved in stages

In year 1 Company A acquired a 10% interest in Company B for CU10,000. In year 2 Company A acquired a further 50% interest for CU70,000 at which point it obtains control and therefore is a business combination.

The cost of the combination in this instance would be CU80,000 (CU70,000+CU10,000).

[/et_pb_text][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Adjustments to the cost of a business combination contingent on future events

Extracts from FRS102 – Section 19.12-19.13

19.12 When a business combination agreement provides for an adjustment to the cost of the combination contingent on future events, the acquirer shall include the estimated amount of that adjustment in the cost of the combination at the acquisition date if the adjustment is probable and can be measured reliably.

19.13 However, if the potential adjustment is not recognised at the acquisition date but subsequently becomes probable and can be measured reliably, the additional consideration shall be treated as an adjustment to the cost of the combination. Allocating the cost of a business combination to the assets acquired and liabilities and contingent liabilities assumed

OmniPro comment

Contingent consideration and change in estimate

Section 19.12 and 19.13 deals with contingent consideration. This is where the price payable to the acquiree is conditional on future events. A flat price is paid for the target entity and a further amount may be payable if profits exceed a certain level in the future. Where the future payment is linked to the cost of an employee’s future service then these costs do not form part of the cost of a business combination instead they should be charged to the profit and loss.

Where contingent consideration exists, the fair value of the expected future payment where it can be reliably measured should be included within the cost of the business combination but it must be probable the amount will be paid. Where the contingent consideration is payable over a period of more than one year the expected payment should be present valued.

Examples of contingent consideration which would meet the definition of being included in the cost of the acquisition are:

- Additional amounts payable if the acquiree’s profit in the year after acquisition exceeds a certain value

- An additional payment if EBITA is maintained or increased after acquisition.

Where a reliable estimate of the contingent consideration cannot be determined or it is not probable it will be payable but it later becomes probable/can now be reliably measured, or the expected consideration changes the adjustment to show the corrected contingent consideration should be included in the cost of the combination and therefore set against the goodwill figure.

The adjustment to goodwill for the change in contingent consideration does not require retrospective adjustment as in effect this is a change in estimate as opposed to an error. This adjustment also has an effect on the amortisation of goodwill as ultimately the goodwill figure will have either reduced or increased.

In this case an entity should charge the additional amortisation on goodwill in the year of the adjustment where the previous estimate was overstated or otherwise credit the over amortisation back to the profit and loss for an under statement of the initial contingent consideration amount. Disclosure of the change in estimate would need to be included in the disclosure notes to the financial statements in line with Section 10. Alternatively an entity can choose to amortise the updated profit figure over its remaining useful life.

Example 6: Changes in contingent consideration – change in estimate

Company A acquires Company B at the start of year 1. The purchase price was CU1,000,000 and a further CU300,000 will be payable in three years time if the future profits remain at CU350,000 or a further CU370,000 if profits increase to CU450,000 for each of the four years.

At the start of year 1, in calculating the business combination cost, Company A would have to assess if it is probable that the company will maintain the profit level. If we assume that it is probable that the CU300,000 will be maintained and the CU450,000 will not be obtained. Then the present value of the CU300,000 should be recognised within goodwill as a cost of the business combination. Assume goodwill before accounting for the business combination is CU100,000 and the discount rate is 5%. Assume the amortisation of goodwill is 10 years.

The present value of CU300,000 in 3 years time is CU259,151 (CU300,000/(1.05)^3). Three years is used here as the fair value is determined at the date of acquisition. The deemed interest on the unwinding of the discount would be:

|

End of year 1: |

CU12,958 (CU259,151 X 5%) |

|

End of year 2: |

CU13,605 ((CU259,151 + CU12,958) X 5%) |

|

End of year 3: |

CU14,286 ((CU2591,51 + CU12,958 + CU13,605) X 5%) |

Therefore this CU259,151 will be added to goodwill i.e. Dr goodwill, Cr provisions. The posting for the unwinding of the discount at the end of year 1 would be to: Cr provision for contingent consideration CU12,958, Dr interest expense CU12,958.

Assume at the end of year 2 the company believes CU450,000 profits will be achieved in each of these years so the probable consideration to be paid is CU370,000. In this case the entity should use the discount rate at the end of year 2 to determine the present value however here as this is repayable within one year no discounting has been performed. The adjustment posted at the end of year 2 would be:

|

CU |

CU |

|

|

Dr Goodwill |

67,429*** |

|

|

Dr Amortisation of Goodwill on Adjustment in P&L |

16,857** |

|

|

Cr Provision for Contingent Consideration |

84,286* |

*Total carrying amount of provision at end of year 2 = CU259,151+interest for year 1 of CU12,958 + interest for year 2 of CU13,605= CU285,714.

The carrying amount of CU285,714 less the required provision based on the new estimate of CU370,000 = CU84,286

**Amortisation of additional goodwill = CU84,286/10yrs*2yrs as two years have elapsed= CU16,857

***Goodwill adjustment = CU84,286 less the amortisation of CU16,857 that would have been charged if this were recognised initially= CU67,429.

As can be seen no prior period adjustment is required as it is a change in accounting estimate.

In this case the company could also choose to amortise the updated goodwill figure over the remaining life instead of posting a catch up amortisation charge e.g. the new goodwill figure could be CU291,670.

Carrying amount of goodwill at end of year 2:

| (CU259,151/10yrs X 8yrs) | = CU207,321 |

| Additional amount posted | = CU84,286 |

| CU291,607 |

This CU291,607 would then by depreciated over the remaining life of 8 years.

Example 7: Contingent consideration – No provision booked in year 1

If we assume in the above example that a reliable estimate cannot be measured at the date of acquisition and therefore no provision was posted but at the end of year 2 a reliable estimate of CU300,000 can be made. The adjustment required would be to:

|

CU |

CU |

|

|

Dr Goodwill |

217,687* |

|

|

Dr Amortisation of Goodwill on Adjustment in P&L |

54,422** |

|

|

Cr Provision for Contingent Consideration |

272,109*** |

*Goodwill adjustment = CU272,109 less the amortisation of CU27,211 that would have been charged if this were recognised initially= CU244,898.

**Amortisation of additional goodwill = CU272,109/10yrs*2yrs as two years have elapsed= CU54,422

***The present value of CU300,000 in 2 years time is CU272,109 (CU300,000/(1.05)^2). Two years is used here as the fair value is determined at the date of the change in estimate. If the discount rate was different at that time than the discount rate at the date of the initial acquisition the new discount rate would be used.

The entity can instead also choose to amortise the CU272,109 over the remaining 8 years from that date.

As can be seen no prior year adjustment is required as it is a change in accounting estimate.

Contingency payments relating to further services

Section 19 or FRS 102 does not differentiate between contingent consideration that in substance, is additional to the purchase price and contingent consideration that, in substance represents compensation for future services.

IFRS 3 on the other hand does differentiate and states that where a contingency payment is part of the agreement which is a payment for future services then this should be expensed to the profit and loss account and should not be included in the cost. Generally where the payment does not have to be paid if the employee leaves this is akin to a payment for future services. Given Section 2 of FRS 102 states that substance over form should be considered, it is not unreasonable that FRS 102 should apply the same principals as IFRS.

This means that entities should assess each element of the contingent consideration payable to determine if it is a payment made to the vendor in their capacity of a vendor or an employee. The following factors should be considered when making this assessment:

- The level of remuneration paid after the acquisition (is it low to compensate for the fact that the contingent payment is paying some of this fee)

- The formula for determining the consideration as to what is included

- Duration of continuing employment.

Cost of a business combination – contingent liabilities

Extracts from FRS102 – Section 19.14-19.15, 19.18 and 19.20-19.21

19.14 The acquirer shall, at the acquisition date, allocate the cost of a business combinationthose contingent liabilities (that satisfy the recognition criteria in paragraph 19.20) at their fair values at that date, except for the items specified in paragraphs 19.15A to 19.15C. Any difference between the cost of the business combination and the acquirer’s interest in the net amount of the identifiable assets, liabilities and provisions for contingent liabilities so recognised shall be accounted for in accordance with paragraphs 19.22 to 19.24.

19.15 Except for the items specified in paragraphs 19.15A to 19.15C, the acquirer shall recognise separately the acquiree’s identifiable assets, liabilities and contingent liabilities at the acquisition date only if they satisfy the following criteria at that date:

(a) In the case of an asset other than an intangible asset, it is probable that any associated future economic benefits will flow to the acquirer, and its fair value can be measured reliably.

(b) In the case of a liability other than a contingent liability, it is probable that an outflow of resources will be required to settle the obligation, and its fair value can be measured reliably.

(c) In the case of an intangible asset or a contingent liability, its fair value can be measured reliably.

19.20 Paragraph 19.15(c) specifies that the acquirer recognises separately a provision for a contingent liability of the acquiree only if its fair value can be measured reliably. If its fair value cannot be measured reliably:

(a) there is a resulting effect on the amount recognised as goodwill or the amount accounted for in accordance with paragraph 19.24; and

(b) the acquirer shall disclose the information about that contingent liability as required by Section 21.

19.21 After their initial recognition, the acquirer shall measure contingent liabilities that are recognised separately in accordance with paragraph 19.15(c) at the higher of:

(a) the amount that would be recognised in accordance with Section 21; and

(b) the amount initially recognised less amounts previously recognised as revenue in accordance with Section 23 Revenue.

19.18 In accordance with paragraph 19.14, the acquirer recognises separately only the identifiable assets, liabilities and contingent liabilities of the acquiree that existed at the acquisition date and satisfy the recognition criteria in paragraph 19.15 (except for the items specified in paragraphs 19.15A to 19.15C). Therefore:

(a) the acquirer shall recognise liabilities for terminating or reducing the activities of the acquiree as part of allocating the cost of the combination only to the extent that the acquiree has, at the acquisition date, an existing liability for restructuring recognised in accordance with Section 21 Provisions and Contingencies; and

(b) the acquirer, when allocating the cost of the combination, shall not recognise liabilities for future losses or other costs expected to be incurred as a result of the business combination.

OmniPro comment

The identifiable assets acquired and liabilities assumed must meet the definition of assets and liabilities the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

An asset is a resource controlled by an entity as a result of past events and from which economic benefits can be expected to flow to the entity (FRS102 Appendix I).

A liability is a present obligation of the entity arising from past events, the settlement from which is expected to result from an outflow of economic benefits (FRS 102 Appendix I).

Section 19 does not provide any guidance on the definition of fair value. Section 2 states that in the absence of specific guidance Section 11.27 to 11.32 should be used. The hierarchy would state that where available a quoted price should be used but where this is not available a valuation model should be used. In the absence of this judgement should be used.

It is very important that the acquirers intentions are not recognised as part of the fair value of assets and liabilities. The acquirer can only recognise restructuring provisions if they have been recognised by the acquiree i.e. if they have been publically announced. The fact that the entity may intend ceasing factory lines for example should not be incorporated into the fair value instead the depreciation of the asset should be adjusted.

The same would be the case if the company acquired a competitor and after acquisition would close the operation, here the fair value given must reflect the value that would be placed on it by a third party.

Measurement of contingent liabilities

Detailed in 19.15 are detailed conditions with regard to recognition of the assets and liabilities acquired. Accounting for intangibles and contingent liabilities is different than any other standard, in that these can be measured where they can be reliably measured. There is no need for there to be a probable outflow of economic benefits.

Although Section 21-Provisions does not allow recognition of contingent liabilities in general Section 19.15(c) makes it clear that a provision should be recognised for a contingent liability in a business combination. Where in a business combination, contingent liabilities exists, these are required to be fair valued where they can be reliably measured. Where this is included in the fair values and as a result it increases goodwill, disclosure is required under Section 19.20 above detailing the fact that a contingent liability has been recognised.

Examples of contingent liabilities may be a tax exposure which was not required to be provided in the acquirees books or legal cases would be another example.

If under the purchase agreement the acquirer is indemnified, the acquirer cannot net the contingent liability with the asset. The asset must be assessed in its own rights and recognised separately at acquisition. An asset should only be recognised where it is virtually certain that it will be achieved.

The fair value is based on the amount that a third party would charge to assume the contingent liability. Regardless of probability, any acquirer would charge something for to take on a potential liability. Where the liability is more than expected, the increase is posted to the profit and loss.

Future losses expected to be incurred are not considered to be liabilities incurred which is in line with Section 21.

Determining fair value of property, plant and equipment

When determining the fair value of PPE, it would be good practice to review the guidance on revaluations contained in Section 17.15C and 17.15D. This would suggest that non-specialised property should be valued at market prices by a qualified valuer. The valuer should ignore government grants when valuing PPE as these are fair valued separately usually at the amount to be repaid in the event of a condition in the grant being breached.

For specialised PPE, the fair value can be determined from a future cash flow approach or a depreciated replacement cost approach.

Determining fair value of intangible assets

Where no active market exists the fair value would be the amount the acquirer would have paid for the asset in an arm’s length transaction between knowledgeable willing parties based on best information available. Section 18 provides further details on this.

This would be done by looking at the multiples used for similar assets

IAS 38 of IFRS noted that it may not always be easy to place values on the intangibles and stated in that case where the below procedures reflected current transactions and practices in the industry the entity could value it by:

- discounting estimate future net cash flows from the asset; or

- estimating the costs that the entity avoids by owning the intangible asset and not needing to:

- license it from another party in an arm’s length transaction;

- recreate or replace it.

Examples of intangibles which would usually be recognised in a business combination if they can be reliably measured are:

- trademarks, trade names, certification marks

- internet domain names

- newspaper mastheads

- non-competition agreements

- customer lists (separable)

- non-contractual customer relationships

- advertising, construction, service or supply contracts

- user rights

- patented technology

- computer software and mask works

- franchise agreements

Determining fair value of inventory

FRS 102 provides no guidance however IFRS 3 states that:

- finished goods should be valued using selling prices less costs of disposal and a reasonable profit allowance for the selling effort of the acquirer based on profit for similar finished goods.

- WIP should be valued at the selling price of the finished goods less costs to complete, cost of disposal and a reasonable profit allowance for the selling effort of the acquirer based on profit for similar finished goods.

It would be reasonable that the above guidance be used under FRS 102.

Example 8: Valuing work in progress

Company A acquired Company B. As part of the assets acquired it included work in progress for bicycles with a cost in the acquire books at CU100,000. The selling price of these bikes when they are finished goods is CU300,000.

In the fair value exercise, the acquirer would need to determine how much extra it will cost to complete. This can be done by looking at the total costs it would be expected that Company B would incur to produce these bikes in full. Assume the total cost to complete is CU250,000, therefore a profit of CU50,000 would have been made.

In order to determine the fair value, the following calculation would be required to determine the profit allowance of CU20,000:

CU50,000 being the profit that would have been made * (CU150,000 being the costs incurred to date / CU250,000 being the total cost to produce the bikes) =CU30,000

Therefore the fair value of the WIP would be CU120,000 (CU300,000-CU150,000-CU30,000 being the profit element).

Determining fair value of financial instruments

The rules in Section 11-Basic Financial Instruments and Section 12-Other Financial Instruments should be followed when fair valuing these instruments. Depending on the accounting framework adopted by the acquiree this may result in differences especially where fair valuing is not required.

Under Section 11 basic financial instruments excluding investments which are less than 20% (i.e. which do not have significant influence), these instruments should be held at amortised costs. Where these are not carried at amortised cost, a fair value adjustment will be required.

For complex instruments, such as forward contracts these should be fair valued at the date of acquisition.

In the majority of cases, debtors, creditors, is not usually significantly different from the book values unless the acquiree did not account for financing transactions.

The majority of differences between fair value and book value are:

- Difference in the carrying amount of debtors due to an over/under provision in the books of the acquiree. Under Section 19.19, an entity has 12 months from the date of acquisition to determine the fair values of the assets and liabilities. Therefore, during this 12 months facts will emerge which will provide evidence that there is an over/under provision. See example 11 below which illustrates how this adjustment would be accounted for i.e. as prior year adjustment or not and the effect it has on goodwill.

- Loans in the acquirer not charged at market rates. In this case the acquirer will have to determine the amortised cost of these loans and identify the financing element. See Section 11 for how this measurement is carried out.

Determining fair value of investment in associate and joint ventures

These should be valued based on the guidance in Section 11 for fair valuing i.e. based on an active market, or where not available a discounted cash flow model using as much industry inputs as possible.

Determining fair value of deferred revenue

Deferred revenue should only be recognised as part of the liabilities taken over to the extent that it relates to an outstanding performance obligation assumed by the acquirer. The fair value of the obligation at the date of acquisition is recognised. This is likely to be lower than the acquirees book value as the amount of revenue that another party would expect to receive on meeting that obligation would not include any profit element relating to the selling or other efforts completed by the acquiree.

If the acquiree’s deferred revenue does not relate to an outstanding performance obligation but to goods or services that have already been delivered, no liability should be recognised by the acquirer.

Example 9: Deferred revenue

Company A acquired Company B. Part of the net liabilities taken over was deferred revenue of CU40,000 for an outstanding service contract which has to be performed. In fair valuing this obligation Company A determines that another third party would take this outstanding contracts work on and would have charged CU35,000. Company A should include in the acquisition cost calculation the CU35,000 and not the CU40,000.

Determining fair value of non-beneficial/beneficial controls

If at the acquisition date, the acquiree has contracts it has entered into which are at rates above or below market rates then these will need to be fair valued. Note these are not onerous contracts as these items are still used by the entity. If they were onerous contracts they should have already been provided for in the acquiree’s books.

Where these contracts exist, the net liability or asset is recognised and released to the consolidated profit and loss over the life of the contract.

Where the contract is above market rate = difference between contract rate and lease rate (applies to operating leases also) recognised as a liability

Where the contract is below market rate = difference between contract rate and lease rate (applies to operating leases also) recognised as an asset

Example 10: Favorable/unfavorable contract

Company A acquired Company B. It has an operating lease on a property at an unfavorable rate. The market rent for a similar property in the area is CU6,000 per annum however the rate charged to Company B is CU10,000. This lease has 10 years to run. The provision to be recognised at acquisition date at its fair value is CU40,000 ((CU10,000-CU6,000)*10yrs). This CU40,000 increases the goodwill.

Each year CU4,000 will be released to the consolidated profit and loss.

The opposite would occur if an asset was to be recognised.

Measurement of deferred tax, employee benefit and share based payments

Extracts from FRS102 – Section 19.15A-19.15C

19.15A The acquirer shall recognise and measure a deferred tax asset or liability arising from the assets acquired and liabilities assumed in accordance with Section 29 Income Tax.

19.15B The acquirer shall recognise and measure a liability (or asset, if any) related to the acquiree’s employee benefit arrangements in accordance with Section 28 Employee Benefits.

19.15C The acquirer shall recognise and measure a share-based payment in accordance with Section 26 Share-based Payment.

OmniPro comment

Deferred tax

Section 29 requires deferred tax to be recognised on all differences including permanent differences with the exception of goodwill between the fair value of the assets and liabilities at the date of acquisition and the carrying amount in the books of the acquiree.

The rate of deferred tax to use (i.e. the sales tax rate or the trading rate) depends on the expected manner of recovery of the asset or liability. Where the assets/liabilities are likely to be settled/used through use in the trade with little residual value, the trading rate enacted at the year end date should be used. Where it is likely the assets will be sold or there is a high residual value the sale tax rate should be used.

A deferred tax asset is only recognised where it is probable there will be future taxable cash flows to utilise the asset. Sometimes it may be possible to recognise losses forward in the acquire which were not recognised previously as there was doubt about future profits. However care needs to be had as to whether these losses will be allowable in the future.

The deferred tax recognised is set against the goodwill figure as detailed in Section 29.11 above and illustrated below.

Deferred tax has been discussed further in Section 29 of this website.

Example 11: Deferred tax on business combinations

Parent A acquired 100% of the ordinary shares of Company B for CU1,000,000. Assume the deferred tax rate is 10%. Assume deferred tax has been recognised correctly in the book amounts transferred. Details of the book value and fair value at the time of acquisition is detailed below:

|

Book value |

Fair value |

|

|

Property, Plant and Equipment |

CU300,000 |

CU550,000 |

|

Intangible Assets |

CUnil |

CU100,000 |

|

Inventory |

CU150,000 |

CU170,000 |

|

Cash |

CU100,000 |

CU100,000 |

|

Debtors |

CU20,000 |

CU25,000 |

|

Creditors |

(CU100,000) |

(CU100,000) |

|

Contingent Liabilities |

CU- |

(CU10,000) |

|

Deferred Tax |

(CU60,000) |

(CU86,500*) |

|

Total Net Assets |

CU410,000 |

CU748,500 |

|

Consideration |

CU1,000,000 |

|

|

Goodwill |

CU251,500 |

The deferred tax to be recognised on acquisition is:

|

Uplift in Property, Plant and Equipment |

CU150,000 |

|

Uplift in Intangible Assets |

CU100,000 |

|

Uplift in Inventory |

CU20,000 |

|

Uplift in Cash |

CUnil |

|

Uplift in Contingent Liabilities |

(CU10,000) |

|

Uplift in Debtors |

CU5,000 |

|

Uplift in Creditors |

CUnil |

|

Total Timing Difference |

CU265,000 |

Once the above exercise is completed management should assess the rate that the asset/liabilities are expected to be reversed. Here the debtors, inventory, contingent liability property, plant and equipment are going to be reversed during trading as they are trading assets. In relation to the intangible assets, if it is assumed these will be used throughout the trade and have little residual value then the trading rate should be used in measuring the deferred tax. The deferred tax liability to recognise as a result of the uplift in value is:

CU265,000 * 10%= CU26,500. Therefore total deferred tax to be shown in the consolidated financial statements is = CU26,500+CU60,000=CU86,500

The journals required in the consolidated financial statements are:

|

CU |

CU |

|

|

Dr Goodwill |

251,500 |

|

|

Dr Net Assets of Company B |

748,500 |

|

|

Cr Investment in Company B in Parent Entity Balance Sheet |

1,000,000 |

From above it is evident that the additional liability for deferred tax has increased goodwill by the same amount. The deferred tax will be reduced as the differences reverses year on year (i.e. for PPE and intangibles in the period depreciation/amortisation is charged, for debtors when they are paid, for inventory when they are sold etc.). The deferred tax is reversed as depreciation/amortisation is charged and as the debtors/contingent liability is realised.

Note in the example above if there was a large residual value on the PPE, then it may be appropriate to recognise deferred tax at the sales rate for the value allocated to the residual amount and the remainder would be measured using the trading tax rate. This would then give a different answer for goodwill.

Example 11A: Deferred tax on a business contribution where net assets as opposed to shares are acquired.

If we assume the company acquired the trade (net assets) as opposed to the shares in the above example deferred tax would be still required to be recognised. In the entity accounts as the fair value would be included on the balance sheet. The journals will be:

|

CU |

CU |

|

|

Dr Net Asset at Fair Value |

248,500 |

|

|

Dr Goodwill |

251,500 |

|

|

Cr Bank |

1,000,000 |

Employee benefits

Where an amount is payable as part of the acquisition and deemed to be for future services, this cost should be accounted for in accordance with Section 28-Employee benefits. Therefore they should be recognised in the profit and loss over the period to which the contingency relates i.e. the length of time the employee has to remain in service after the acquisition. The amount provided for in the profit and loss in the consolidated financial statements should use a best estimate of the likely volume of employees that will stay on to receive the payment.

Share based payments

It would be unusual to have to account for share based payments as part of the acquisition cost. Usually where share are issued they are based on an agreed price per share. Where shares are issued as part of contingent consideration which are issued based on an agreed total value this would be accounted for as normal contingent consideration as discussed above.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]