[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-19/” type=”big” color=”red”] Return to Section 19 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Group reconstructions

Extracts from FRS 102 section 19.27-19.32

19.27 Group reconstructions may be accounted for by using the merger accounting method provided:

(a) the use of the merger accounting method is not prohibited by company law or other relevant legislation;

(b) the ultimate equity holders remain the same, and the rights of each equity holder, relative to the others, are unchanged; and

(c) no non-controlling interest in the net assets of the group is altered by the transfer.

19.28 The provisions of paragraphs 19.29 to 19.33, which are explained by reference to an acquirer or issuing entity that issues shares as consideration for the transfer to it of shares in the other parties to the combination, should also be read so as to apply to other arrangements that achieve similar results.

Merger accounting method

19.29 With the merger accounting method the carrying values of the assets and liabilities of the parties to the combination are not required to be adjusted to fair value, although appropriate adjustments shall be made to achieve uniformity of accounting policies in the combining entities.

19.30 The results and cash flows of all the combining entities shall be brought into the financial statements of the combined entity from the beginning of the financial year in which the combination occurred, adjusted so as to achieve uniformity of accounting policies. The comparative information shall be restated by including the total comprehensive income for all the combining entities for the previous reporting period and their statement of financial position for the previous reporting date, adjusted as necessary to achieve uniformity of accounting policies.

19.31 The difference, if any, between the nominal value of the shares issued plus the fair value of any other consideration given, and the nominal value of the shares received in exchange shall be shown as a movement on other reserves in the consolidated financial statements. Any existing balances on the share premium account or capital redemption reserve of the new subsidiary shall be brought in by being shown as a movement on other reserves. These movements shall be shown in the statement of changes in equity.

19.32 Merger expenses are not to be included as part of this adjustment, but shall be charged to the statement of comprehensive income as part of profit or loss of the combined entity at the effective date of the group reconstruction.

OmniPro comment

Where the conditions for merger accounting is met it results in considerable less work for the acquiring entity. No fair value valuations are required to be performed and no goodwill needs to be calculated. The net assets as per the acquired entity is the amount that is recognised in the consolidated financial statements. Section 19.27 above describes the conditions for the relief to be claimed.

Merger accounting differs from the purchase method of accounting as follows:

- Under merger accounting, the results, balance sheet and cashflows of the acquiree are shown in the current and comparative financial year of the parent consolidated accounts regardless of what period in the year this was acquired.

Under purchase method accounting, the results are only shown from the date of acquisition and the comparative figures on first acquisition does not include the acquirees results

- Merger accounting does not require the net assets of the acquiree to be fair valued whereas purchase accounting does, and any fair value adjustments must be accounted for in the parent.

- Merger accounting does not require goodwill to be calculated whereas purchase accounting does.

Note where inter group sales are made the normal rules with regard to intergroup balances/sales/profits are applied to eliminate these.

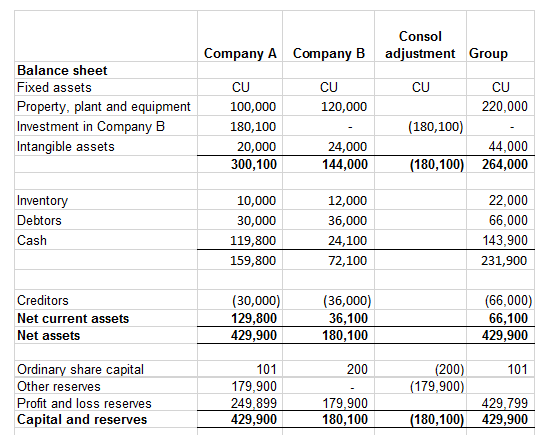

Example 20: Group reorganisations

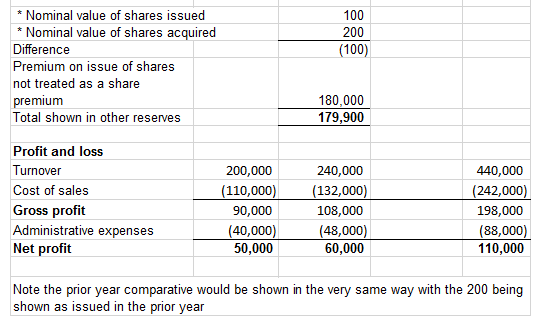

Company A who is a member of a group with Parent A, acquires Company B from Parent A on 1 March in return for the issuance of 100 CU1 ordinary shares for CU1,801 each i.e.CU180,100. This CU180,100 is equivalent to the net assets of Company B. Company A applies merger accounting and the year end is 31 December. The profit for the 9 month period to 31 December in Company B was CU20,000 and the profit made for the full year is CU60,000

In the consolidated financial statements of Company A the following would be shown assuming the below results. Note the profit made for the full year is included, the date of acquisition is irrelevant. If in the below analysis, the nominal value of shares issued in Company B was less than the actual amount issued to Company B, the other reserve would be reduced to a negative by the difference and therefore on occasion there can be a debit balance in the other reserve.

The above example assumes shares were acquired, merger accounting can also apply when an entity acquires the trade and net assets as opposed to shares (i.e. the acquisition of a business in return for their issuance of shares in itself.) Applying this to the above example the journals would be:

|

|

CU |

CU |

|

Dr Net Assets |

180,100 |

|

|

Cr Ordinary Share Capital |

|

100 |

|

Cr Merger Reserve |

|

180,000 |

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]