[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-15/” type=”big” color=”red”] Return to Section 15 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Section 15: Investments in Joint Ventures

Scope

Section 15 defines a joint venture and depending on the framework of the joint venture sets out how this should be accounted for and disclosed in the consolidated and individual financial statements.

Definition of joint ventures

Extract from FRS 102: Section 15.2 – 15.3

15.2 Joint control is the contractually agreed sharing of control over an economic activity, and exists only when the strategic financial and operating decisions relating to the activity require the unanimous consent of the parties sharing control (the ventures’).

15.3 A joint venture is a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control. Joint ventures can take the form of jointly controlled operations, jointly controlled assets, or jointly controlled entities.

OmniPro comment

It is clear that a joint venture does not have to be a company, it can be an unincorporated business. No one party can have control above the other and in order for one to exist there must be at least 2 parties. Unanimous consent is required in the arrangement. Unanimous consent means that any party to the arrangement can prevent any of the other parties, or group of other parties, from making decisions of a strategic, financial or operating nature without its consent.

When the contractual arrangement identifies one venturer as the manager of the joint venture, it should be clear that the operator does not control the operation; it is merely running the business in line with the ventures’ wishes as a whole. It cannot take action without the approval of the other venturers on key strategic, financial or operating decisions. Examples of types of strategic decisions that would require unanimous consent are:

- Major financing;

- Approving a business plan;

- Approving a budget;

- Remuneration policy;

- Share issues; and

- Significant asset disposals and acquisitions.

There are three types of joint ventures namely;

- Jointly controlled operations;

- Jointly controlled assets; and

- Jointly controlled entities.

Each of these are explained further below.

Although FRS 102 does not define what the strategic, financial and operating decisions would cover, these are generally understood to include areas such as budgeting, capital expenditure, treasury management, dividend policy, production, marketing, sales and human resources.

Appendix I in FRS 102 defines control as the ‘power to govern the financial and operating policies of an entity so as to obtain benefits from its activities’.

Section 15 does not define what is meant by a contractual arrangement. However in order for it to be contractual in nature, it must be in writing and agreed by all parties. The rules may be incorporated in the articles of association or by way of a shareholders agreement. IAS 31 of IFRS states that this contract arrangement should set out the following:

- The activity, duration and reporting obligations of the joint venture;

- The rules for appointment of the board of directors or equivalent governing body of the joint venture and the voting rights of the venturers;

- The capital contributions to be made by the venturers; and

- Rules with regard to the sharing by the venturers of the output, income, expenses, or results of the joint venture.

In order to be a joint venture there is no requirement that the shareholders own the same percentage shares/rights in the entity. If the contractual agreement makes it clear the unanimous agreement is required this is the key determination.

Example 1: Determining if joint control exists

X, Y and Z enter into an agreement to start a joint entity. Entity A, X, Y and Z own 30%, 50% and 20% respectively. All parties enter into a contractual agreement whereby it is agreed that a unanimous decision is required from X and Y on all major strategic financial and operating decisions.

In this instance X and Y are joint venturers and will account for this as a joint venture however Z should account for this as an associate assuming it has significant influence if not it should be accounted for under Section 11.

Jointly controlled operations

Extract from FRS102: Section 15.4 – 15.5

15.4 The operation of some joint ventures involves the use of the assets and other resources of the ventures’ rather than the establishment of a corporation, partnership or other entity, or a financial structure that is separate from the ventures’ themselves. Each venturer uses its own property, plant and equipment and carries its own inventories. It also incurs its own expenses and liabilities and raises its own finance, which represent its own obligations. The joint venture activities may be carried out by the venturer’s employees alongside the venturer’s similar activities. The joint venture agreement usually provides a means by which the revenue from the sale of the joint product and any expenses incurred in common are shared among the ventures’.

15.5 In respect of its interests in jointly controlled operations, a venturer shall recognise in its financial statements:

(a) the assets that it controls and the liabilities that it incurs; and

(b) the expenses that it incurs and its share of the income that it earns from the sale of goods or services by the joint venture.

OmniPro comment

Jointly controlled operations

Jointly controlled operations are effectively operations where equipment etc. is shared but ownership does not pass nor is ownership shared. It is in fact not a legal entity. Each party incurs its own costs and incurs its own liabilities.

An example would be where two or more venturers combine their operations, resources or expertise to jointly manufacture market and distribute a product. Each venturer undertakes a different part of the manufacturing process and bears its own costs. Revenue from the sales of the product is shared on the basis of the contractual agreement. There is no separate entity doing this work.

Accounting for a jointly controlled operation

As the assets, liabilities, income and expenses will already be reflected in the individual financial statements, no consolidation adjustments are required as they are already included. A separate set of books is not required to be kept however it is likely that they will be kept so the performance of the entity can be determined.

Example 2: Loans to jointly controlled operation

Company X and Y entered into a jointly controlled operation where the contractual agreement makes it clear that it is owned 50/50 by each party. However in order to get the operation started, Company X had to provide a loan of CU100,000 and Company Y a loan of CU200,000 to the joint operation.

Therefore the total borrowings in the joint operation are CU300,000 and under the agreement costs and revenues are shared 50/50 which includes the liabilities of the joint operation. Therefore Company Y has to recognise an asset for the amount receivable from Company X and Company X has to recognise its liability.

The way in which the amount payable to Company Y in Company X’s financial statements should be accounted for is as follows:

|

|

CU |

CU |

|

Dr Amounts due from Joint Venture |

50,000 |

|

|

Cr Amounts due to Company Y |

|

50,000* |

*(CU300,000*50%) = CU150,000. Therefore, amount to be shown as a receivable is the amount of the loan given of CU200,000 less CU150,000 being the element that Company Y legally had to make (CU50,000).

Example 3: Accounting for a jointly controlled operation

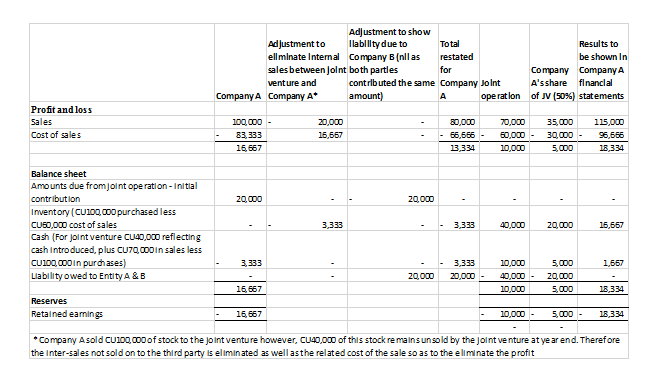

Company A manufacturers a product. It has entered into an agreement with a packaging and marketing Company, Company B to create a jointly controlled operation. A contractual agreement makes it clear that all decisions require unanimous consent. As per the agreement the profits and liabilities are shared 50/50. As part of the agreement Company A will charge the operation on a cost plus 20% basis. Both parties are required to contribute CU20,000 each.

During the year Company A sold CU100,000 of goods to the joint operation which cost Company A CU83,333.

The joint operation made sales of CU70,000 and it cost the joint operation CU60,000. To account for these joint operation sales in Company A’s financial statements, the below is required:

|

Sales in the year by Co A to Joint Venture included in sales in Co A |

100,000 |

|

Stock in Joint Venture at year end relating to purchase from Co A |

-40,000 |

|

Total external Sales |

60,000 |

|

|

|

|

Total sales to exclude from Co A P&L |

|

|

Sales still in stock in joint venture |

40,000 |

|

% of joint venture owned by Co A and therefore to be eliminated = 50% |

20,000 |

|

|

|

|

Cost of sales for the above sales derecognised |

|

|

CU20,000 of sales eliminated as it was within the same company which was charged on a cost plus 20%. Therefore cost of sales is CU20,000/1.2 which needs to be eliminated |

16,667 |

|

|

|

|

Journal required therefore is to: |

|

|

Dr sales in Co A |

20,000 |

|

Cr cost of sales in Co A |

16,667 |

|

Dr inventory in joint venture |

3,333 |

Jointly controlled assets

Extract from FRS 102 15.6 – 15.7

15.6 Some joint ventures involve the joint control, and often the joint ownership, by the ventures’ of one or more assets contributed to, or acquired for the purpose of, the joint venture and dedicated to the purposes of the joint venture.

15.7 In respect of its interest in a jointly controlled asset, a venturer shall recognise in its financial statements:

(a) its share of the jointly controlled assets, classified according to the nature of the assets;

(b) any liabilities that it has incurred;

(c) its share of any liabilities incurred jointly with the other ventures’ in relation to the joint venture;

(d) any income from the sale or use of its share of the output of the joint venture, together with its share of any expenses incurred by the joint venture; and

(e) any expenses that it has incurred in respect of its interest in the joint venture.

OmniPro comment

Jointly controlled assets are effectively operations where ventures’ contribute equally towards the cost of one or more assets and they are owned jointly. No legal entity is created.

Funds provided to the jointly controlled assets are treated the same way as included in the example above for jointly controlled operations.

Accounting for jointly controlled assets

As the assets, liabilities, income and expenses will already be reflected in the individual financial statements, no consolidation adjustments are required as they are already included in the entity financial statements. A separate set of books is not required to be kept however it is likely that they will be kept so the performance of the entity can be determined.

Example 4: Jointly controlled assets

Company A, B & C entered into a joint venture whereby they decided to purchase a specially designed warehouse for holding frozen food. As part of the joint venture agreement, all parties had equal say in the operation of the facility and therefore meet the definition of a joint venture. Company A, B & C contributed CU10,000, CU40,000 and CU50,000 respectively which is reflective of the ownership in the asset. The cost of the asset was CU100,000.

The costs are shared in proportion to the ownership. During year 1 the joint venture incurred CU10,000 in costs to maintain the facility excluding depreciation. The property is being depreciated over 5 years. Company A made sales from this unit of CU100,000. This would be accounted in the books of Company A as follows

|

|

CU |

CU |

|

Dr PPE |

10,000 |

|

|

Cr Cash |

|

10,000 |

Being journal to recognise the portion of the asset on Company A’s balance sheet

|

|

CU |

CU |

|

Dr Property Expenses |

1,000 |

|

|

Cr Bank (CU10,000*10%) |

|

1,000 |

Being journal to reflect Company A’s portion of expenses

|

|

CU |

CU |

|

Dr Depreciation |

2,000 |

|

|

Cr Accumulated Depreciation on PPE (CU100,000/5yrs*10%) |

|

2,000 |

Being journal to reflect depreciation charge on Company A’s portion of the assets

|

|

CU |

CU |

|

Dr Debtors |

100,000 |

|

|

Cr Sales |

|

100,000 |

Being journal to reflect sales by Company A.

Jointly controlled entities

Extract from FRS 102 15.8 – 15.9B

15.8 A jointly controlled entity is a joint venture that involves the establishment of a corporation, partnership or other entity in which each venturer has an interest. The entity operates in the same way as other entities, except that a contractual arrangement between the ventures’ establishes joint control over the economic activity of the entity.

Measurement—accounting policy election

15.9 A venturer that is not a parent but has one or more interests in jointly controlled entities shall, in its individual financial statements, account for all of its interests in jointly controlled entities using either:

(a) the cost model in accordance with paragraphs 15.10 to 15.11;

(b) the fair value model in accordance with paragraphs 15.14 to 15.15A; or

(c) at fair value with changes in fair value recognised in profit or loss (paragraphs 11.27 to 11.32 provide guidance on fair value).

15.9A A venturer that is a parent shall, in its consolidated financial statements, account for all of its investments in jointly controlled entities using the equity method in accordance with paragraph 15.13, except as required by paragraph 15.9B.

15.9B A venture that is a parent, shall measure its investments in jointly controlled entities held as part of an investment portfolio at fair value with changes in fair value recognised in profit or loss in the consolidated financial statements.

OmniPro comment

Jointly controlled entities are joint ventures that involve the establishment of a corporation, partnership or other entity in which the venture has an interest and there is a contractual arrangement between the ventures’ establishing joint control over the economic activity.

The options for a holder of an investment in a jointly controlled entity who is not a parent can choose to:

- carry the investment at cost less impairment; or

- fair value through the profit and loss; or

- fair value through other comprehensive income.

An entity should apply the accounting policy chosen consistently for all investments which meet the definition of a jointly controlled entity.

For a parent company preparing consolidated financial statements the joint venture must be accounted for:

- under the equity method

UNLESS

The investment is held as part of an investment portfolio in which case the interest should be measured:

- at fair value through the profit and loss.

An investment held as part of an investment portfolio as defined in Appendix I of FRS 102 is ‘if its value to the investor is through fair value as part of a directly or indirectly held basket of investments rather than as a media through which the investor carries out business’.

The options for a parent in its entity set of financial statements who hold joint ventures are set out in Section 9.26. It can choose to:

- carry the investment at cost less impairment; or

- fair value the investment through the profit and loss; or

- fair value the investment through other comprehensive income.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]