[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” custom_padding=”0px||0px|” next_background_color=”#000000″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”||5px|” allow_player_pause=”off” parallax=”off” parallax_method=”on” make_equal=”off” parallax_1=”off” parallax_method_1=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” use_border_color=”off” border_color=”#ffffff” border_style=”solid” custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”30px||0px|” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” background_color=”#1e73be” prev_background_color=”#000000″ next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” custom_padding=”30px||0px|” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”0px||0px|” custom_padding_last_edited=”on|desktop” prev_background_color=”#1e73be” next_background_color=”#000000″][et_pb_row][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.2″ title=”Index”]

Contents

15.2 Definition of joint ventures.

15.2.1 Extract from FRS 102: Section 15.2 – 15.3.

15.2.2.1 What forms of entities can be considered a joint venture.

15.2.2.2 What happens where one of the venturers manage the joint venture?

15.2.2.4 What types of joint ventures are there?

15.2.2.5 What is defined as the strategic, financial and operating decisions?

15.2.2.5.1 What is defined a control for the purpose of joint control?

15.2.2.6 What is meant by a contractual arrangement?

15.2.2.7 Is there a requirement for the same percentage holding to be held?

15.2.2.7.1 Determining if joint control exists.

15.3 Jointly controlled operations.

15.3.1 Extract from FRS102: Section 15.4 – 15.5.

15.3.2.1 Jointly controlled operations – Defined.

15.3.2.1.1 Example of a jointly controlled operation.

15.3.2.2 Accounting for a jointly controlled operation.

15.3.2.2.1 Loans to jointly controlled operations.

15.3.2.2.2 Accounting for a jointly controlled operation – worked example.

15.4 Jointly controlled assets.

15.4.1 Extract from FRS 102 15.6 – 15.7.

15.4.2.1 Jointly controlled assets – defined.

15.5 Jointly controlled entities.

15.5.1 Extract from FRS 102 15.8 – 15.9B.

15.5.2.1 Jointly controlled entities – defined.

15.5.2.2 Accounting for Jointly controlled entities.

15.5.2.2.1 Accounting policy choice.

15.6.1 Extract from FRS 102 15.10 – 15.11.

15.6.2.1.1 Definition of cost.

15.6.2.3 Deferred tax under the cost model.

15.6.2.4 Illustration of the cost model.

15.6.2.5 Recognition of Income.

15.7.1 Extract from FRS 102: Section 15.13, 15.16, 15.17 and extract from Section 14.8.

15.7.2.2 Application of equity accounting.

15.7.2.2.2 Worked example illustrating equity accounting requirements.

15.7.2.4 Transactions with joint venturers’.

15.7.2.4.1 Sales and purchases.

15.7.2.4.1.2 Elimination of profit where investor sells goods to joint venture.

15.7.2.4.1.3 Sale of assets to and from joint ventures.

15.7.2.5 Date of joint venture financial statements (Section 14.8(f) of FRS 102).

15.7.2.6 Uniform Accounting policies (Section 14.8 (g) of FRS 102).

15.7.2.7 Losses in excess of investment (Section 14.8(h) of FRS 102).

15.7.2.8 Deferred tax on unremitted earning in the consolidated financial statements.

15.7.2.8.2 Timing difference to reverse through sale.

15.7.2.8.3 Timing difference to reverse through receipt of dividends.

15.7.2.8.4 Example of deferred tax on unremitted earnings.

15.8 Discontinuing the equity method.

15.8.1 Extract from FRS102: Section 14.8(i) and section 15.18.

15.8.2.2.1 Full derecognition of joint venture due to sale.

15.8.2.2.2 Partial derecognition of joint venture due to sale but joint control still retained.

15.8.2.2.3 Transfer of joint venture as a result of loss of joint control due to sale.

15.8.2.2.4 Loss of joint control not due to sale.

15.10 Step increase in an existing joint venture.

15.11 Step increase from investment/financial asset to joint venture.

15.12 Fair value model for a jointly controlled entity.

15.12.1 Extracts from FRS102-Section 15.14-15.15A.

15.12.2.1 Fair value through other comprehensive income (OCI).

15.12.2.1.1 Measurement and recognition.

15.12.2.1.2 Treatment of transaction costs.

15.12.2.1.3 Frequency of valuations.

15.12.2.1.4 What happens when fair value cannot be measured reliably.

15.12.2.1.6 Example of application of Fair Value through Other Comprehensive Income model.

15.12.2.1.7 Recognition of income.

15.12.2.2 Fair value through the profit and loss.

15.12.2.2.1 Measurement and recognition.

15.12.2.2.2 Frequency of valuations.

15.12.2.2.3 What happens when fair value cannot be measured reliably?

15.12.2.2.4 Example of application of Fair Value through profit and loss model.

15.13 Disclosures in individual and consolidated financial statements.

15.13.1 Extracts from FRS102-Section 15.19 – 15.21A.

15.13.2.2 Consolidated financial statements.

15.13.2.2.1 Accounting policies – consolidated financial statements.

15.13.2.2.2 Notes to the financial Statements.

15.13.2.2.3 Consolidated profit and loss account showing share of joint venture interest.

15.13.2.3 Parent entity financial statements.

15.13.2.3.1 Accounting policies.

15.13.2.3.2 Notes to the financial statements.

15.13.2.3.3 Profit and loss account for entity that is not a parent.

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” text_orientation=”justified” use_border_color=”off” border_color_all=”off” module_alignment=”left” _builder_version=”3.1.1″]

15.3 Jointly controlled operations

15.3.1 Extract from FRS102: Section 15.4 – 15.5

15.4 The operation of some joint ventures involves the use of the assets and other resources of the ventures’ rather than the establishment of a corporation, partnership or other entity, or a financial structure that is separate from the ventures’ themselves. Each venturer uses its own property, plant and equipment and carries its own inventories. It also incurs its own expenses and liabilities and raises its own finance, which represent its own obligations. The joint venture activities may be carried out by the venturer’s employees alongside the venturer’s similar activities. The joint venture agreement usually provides a means by which the revenue from the sale of the joint product and any expenses incurred in common are shared among the ventures’.

15.5 In respect of its interests in jointly controlled operations, a venturer shall recognise in its financial statements:

(a) the assets that it controls and the liabilities that it incurs; and

(b) the expenses that it incurs and its share of the income that it earns from the sale of goods or services by the joint venture.

15.3.2 OmniPro comment

15.3.2.1 Jointly controlled operations – Defined

As per Section 15.4 of FRS 102, jointly controlled operations are effectively operations where equipment etc. is shared but ownership does not pass nor is ownership shared. It is in fact not a legal entity. Each party incurs its own costs and incurs its own liabilities.

15.3.2.1.1 Example of a jointly controlled operation

An example would be where two or more venturers combine their operations, resources or expertise to jointly manufacture market and distribute a product. Each venturer undertakes a different part of the manufacturing process and bears its own costs. Revenue from the sales of the product is shared on the basis of the contractual agreement. There is no separate entity doing this work.

15.3.2.2 Accounting for a jointly controlled operation

As the assets, liabilities, income and expenses will already be reflected in the individual financial statements of each venturer, no consolidation adjustments are required as they are already included. A separate set of books is not required to be kept however it is likely that they will be kept so the performance of the entity can be determined. Therefore as per Section 15.5 of FRS 102 each venturer accounts for the assets it controls, the liabilities they incur and the expenses incurred and share of income that it earns from the sale of goods/services.

15.3.2.2.1 Loans to jointly controlled operations

Example 2: Loans to jointly controlled operation

Company X and Y entered into a jointly controlled operation where the contractual agreement makes it clear that it is owned 50/50 by each party. However in order to get the operation started, Company X had to provide a loan of CU100,000 and Company Y a loan of CU200,000 to the joint operation.

Therefore the total borrowings in the joint operation are CU300,000 and under the agreement costs and revenues are shared 50/50 which includes the liabilities of the joint operation. Therefore Company Y has to recognise an asset for the amount receivable from Company X and Company X has to recognise its liability.

The way in which the amount payable to Company Y in Company X’s financial statements should be accounted for is as follows:

| CU | CU | |

| Dr Amounts due from Joint Venture | 50,000 | |

| Cr Amounts due to Company Y | 50,000* |

*(CU300,000*50%) = CU150,000. Therefore, amount to be shown as a receivable is the amount of the loan given of CU200,000 less CU150,000 being the element that Company Y legally had to make (CU50,000).

15.3.2.2.2 Accounting for a jointly controlled operation – worked example

Example 3: Accounting for a jointly controlled operation

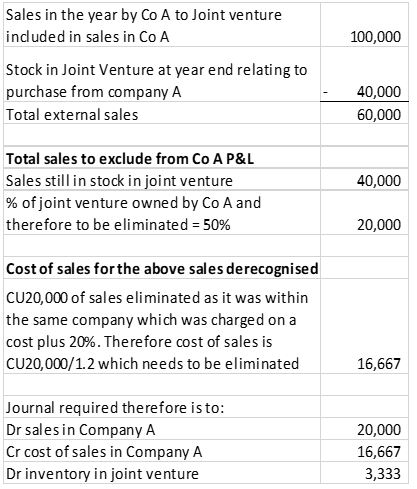

Company A manufacturers a product. It has entered into an agreement with a packaging and marketing Company, Company B to create a jointly controlled operation. A contractual agreement makes it clear that all decisions require unanimous consent. As per the agreement the profits and liabilities are shared 50/50. As part of the agreement Company A will charge the operation on a cost plus 20% basis. Both parties are required to contribute CU20,000 each.

During the year Company A sold CU100,000 of goods to the joint operation which cost Company A CU83,333.

The joint operation made sales of CU70,000 and it cost the joint operation CU60,000. To account for these joint operation sales in Company A’s financial statements, the below is required:

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle admin_label=”Examples” _builder_version=”3.2″ title=”Practical Examples”]

Example

Example 1: Determining if joint control exists.

Example 2: Loans to jointly controlled operation.

Example 3: Accounting for a jointly controlled operation.

Example 4: Jointly controlled assets.

Example 5A: Dividend paid out of pre-acquisition reserves.

Example 6: Equity method accounting.

Example 7: Elimination of profit where investor sells goods to joint venture.

Example 8: Sale of asset from venturer to joint venture at profit.

Example 9: Sale of asset from venturer to joint venture at loss.

Example 10: Sale of asset from joint venture to venturer at loss (Section 15.17 of FRS 102).

Example 11: loss in excess of investment.

Example 12: Deferred tax on unremitted earnings.

Example 13: Full derecognition of joint venture due to sale.

Example 14: Partial derecognition of a joint venture due to sale but joint control still retained.

Example 15: Transfer of joint venture as a result of loss of joint control due to sale.

Example 16: Loss of joint control not due to sale.

Example 18: Step increase in an existing joint venture.

Example 19: Step increase from investment /financial asset to associate.

Example 20: Adoption of fair value through other comprehensive income.

Example 21: Adoption of fair value through profit and loss.

Example 22: Extract from the accounting policy notes to the consolidated financial statements.

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]