[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-21/” type=”big” color=”red”] Return to Section 21 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Contingent Assets

Extract from FRS 102 – Section 21.13

21.13 An entity shall not recognise a contingent asset as an asset. Disclosure of a contingent asset is required by paragraph 21.16 when an inflow of economic benefits is probable. However, when the flow of future economic benefits to the entity is virtually certain, then the related asset is not a contingent asset, and its recognition is appropriate.

OmniPro comment

Appendix 1 of FRS 102 defines a contingent asset as:

‘a possible asset that arises from a past event and whose existence will be confirmed with occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity’.

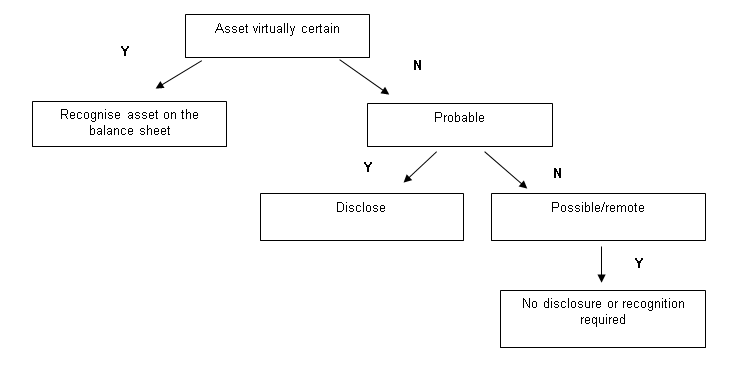

- An asset is only recognised when the inflow of economic benefits are virtually certain.

- Where inflows from a contingent asset is probable (i.e. more likely than not to be received >50%), the contingent asset is not recognised but disclosed.

- Where it is possible or remote the contingent asset is not disclosed or recognised.

See illustration of when a contingent asset should be recognised or instead disclosure required/or not through the use of the illustrative diagram.

Example 20: Contingent assets

Company A has taken a case against company B. At the year end, Company A has won the case and been awarded CU200,000 in damages. However, prior to year end. Company B, appealed to the high court.

Here as there is a risk that Company B might be successful in the appeal, as the asset is not virtually certain, it cannot be recognised, instead it should be disclosed on the basis that it is probable. However the facts and circumstances for each event will need to be looked at to assess if this actually is probable or just possible.

Example 21: Financial guarantees

Company A has provided a guarantee to the bank on behalf of company B whereby they have guaranteed the repayment of a loan if Company B defaults. At the end of year 1, company B is in a very strong financial position. However at the end of year 2, company B is in financial difficulty with very poor cash flows due to the loss of its main customer and as a result there is risk with regard to its going concern.

Based on the facts at the end of year 1, a contingent liability would exist or possibly a contingent liability which requires no disclosure as the probability is remote because:

- Although there is a present obligation as a result of a past event (i.e. the giving of the guarantee to the bank)

- The outflow of economic benefits it not probable as Company B is in a very strong position

Based on the facts at the end of year 2, a provision should be recognised for the estimated cost of honoring the guarantee on the basis that the likelihood of the transfer of economic benefits is probable.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]