[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [breadcrumb] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”https://ie.frs102.com/members/premium-toolkit/section-21/” type=”big” color=”red”] Return to Section 21 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

Contingent liabilities

Extract from FRS 102 – Section 21.12

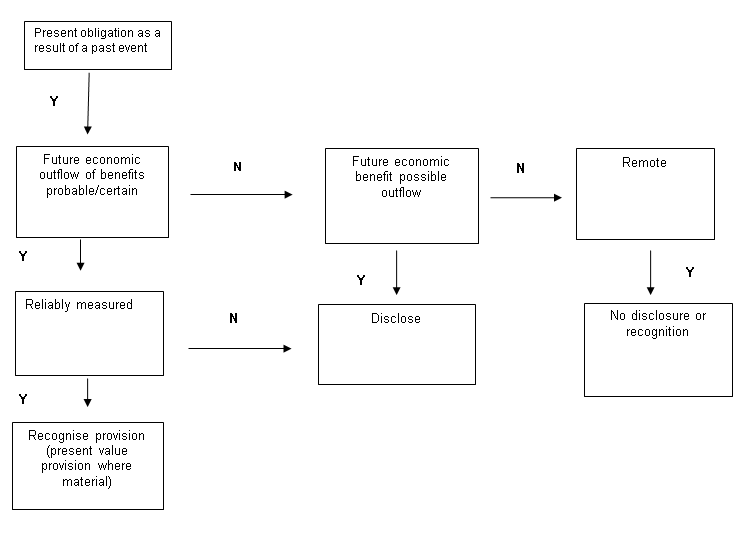

21.12 A contingent liability is either a possible but uncertain obligation or a present obligation that is not recognised because it fails to meet one or both of the conditions (b) and (c) in paragraph 21.4. An entity shall not recognise a contingent liability as a liability, except for provisions for contingent liabilities of an acquiree in a business combination (see paragraphs 19.20 and 19.21). Disclosure of a contingent liability is required by paragraph 21.15 unless the possibility of an outflow of resources is remote. When an entity is jointly and severally liable for an obligation, the part of the obligation that is expected to be met by other parties is treated as a contingent liability.

OmniPro comment

A contingent liability is defined in Appendix 1 of FRS 102 as:

- ‘a present obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; OR

- a present obligation that arises from past events but is not recognised because:

- it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; OR

- the amount of the obligation cannot be reassured with sufficient reliability.’

Where a contingent liability exists where it is possible that there will be an outflow of economic benefits then a disclosure is required in the financial statements. Where the likelihood is considered remote no disclosure is required.

As discussed earlier, it may be unusual to conclude where an estimate cannot be determined given the possibility of using probabilities etc. In trying to assess the liability the entity should consult with experts e.g. solicitors to determine whether those parties can determine the expected out flow.

In reality, a contingent liability will arise:

- where it is possible but not probable (probable being more likely than not) for a future outflow of economic circumstances unless the possibility is remote in which case no disclosure is required.

- A present obligation may have occurred but it can only be determined on occurrence or non-occurrence of a future event

- the future outflow cannot be reliably measured

Where initially an entity has determined a contingent liability existed, the entity should continuously review the facts and circumstances and where it then emerges that a provision is required at that time, this is merely a change in estimate and a provision posted from that date. Section 32 makes it clear that circumstance since year end but before the signing of financial statement should be reviewed to provide further evidence on provisions.

The only exception to non-recognition of contingent liabilities is the case where contingent liabilities are acquired in a business combination.

Section 21 – Liability Decision Tree

Example 17: Contingent liability – remote

An employee has taken a case against Company A for unfair dismissal. At year end management have consulted with its legal advisor who believe the possibility of the employee succeeding with the case is remote.

Here there is a present obligation (i.e. the obligation to possibly compensate the employee) as a result of a past event (i.e. the dismissal of the employee) but the likelihood of outflow of economic benefits is remote i.e. not probable. In this particular case, no disclosure is required.

Example 18: Contingent liability – possible

An employee has taken a case against Company A for unfair dismissal. At year end management have consulted with its legal advisor who believe there is a possibility that the employee will succeed however it is not remote. In this particular case this should be disclosed in the notes to the financial statements.

Example 19: Contingent liability – occurrence or non-occurrence of future events/non ability to estimate liabilities

Company A is an insurance underwriter that earns profit commission from insurance companies based on the number of claims made on policies that it has arranged for the insurance company. The commissions recognised can change in future years depending on the future loss ratios in relation to unsettled claims. Given the fact that the ratios can change year on year, the directors believe that it is not possible to estimate any future liabilities. On this basis although it is probable that there will be future economic outflows/inflows, and although there is a present obligation as a result of a past event (i.e. the recognising of commissions year on year), these cannot be measured reliably hence it is appropriate to disclosure these as a contingent liability.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]